Real Estate in Bangalore: Prices, Affordability, Top Performing Market...

Key Takeaways Bangalore’s tech sector drives strong demand for properties under...

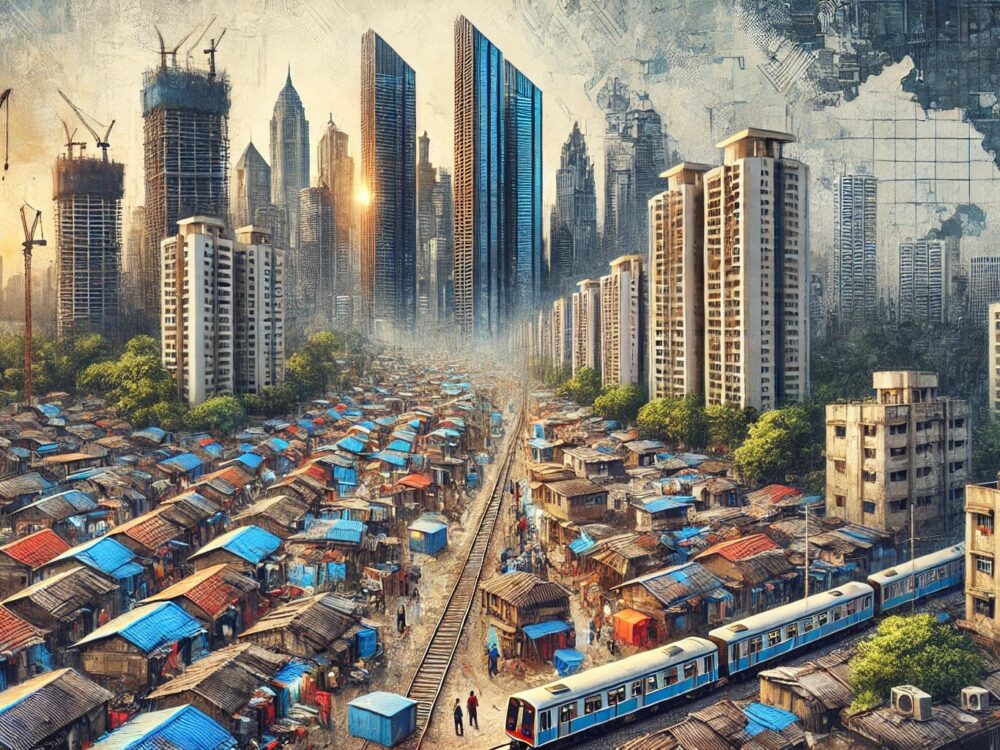

Housing affordability, which means being able to buy or rent a home without straining finances, is crucial for urban growth. However, this is a major challenge in Greater Mumbai. With an average price (as of Q2 2024 ), of ₹32,150 per square foot, Greater Mumbai’s housing costs are far higher compared to cities like Pune (₹15,187) and Bengaluru (₹14,265), making owning a home unaffordable for many.

The concept of housing affordability was initially introduced to serve the financially weaker sections of society, ensuring access to safe and dignified housing for those at the lower end of the economic spectrum. The Government of India, in its 2008 Deepak Parekh Committee Report, defined housing affordability as follows:

In Mumbai, the term “affordable housing” is defined differently by various institutions, each with specific criteria:

Despite these benchmarks, the reality for India’s affluent middle class, particularly in metropolitan cities, is different. While the Pradhan Mantri Awas Yojana (PMAY) aims to address urban housing shortages among Economically Weaker Sections (EWS), Low-Income Groups (LIG), and Middle-Income Groups (MIG), including slum population, by ensuring a pucca house for all eligible urban households, the middle class often finds itself unsupported in navigating the housing market

In Greater Mumbai, the average price-to-income ratio for a 2BHK home is 8.9 times the annual income for affluent middle-class professionals aged 35 and below, significantly exceeding what is considered affordable.

The Indian government has implemented several schemes and projects to enhance housing affordability for Mumbai, particularly targeting the economically weaker sections. However, the affluent middle class often finds these measures insufficient to meet their needs.

Launched in 2015, PMAY aims to provide affordable housing to urban and rural poor by 2022. The scheme offers interest subsidies on home loans for eligible beneficiaries. While it has benefited many in the lower-income brackets, the middle class often falls outside the eligibility criteria, limiting its impact on this segment.

MHADA conducts lotteries to allocate affordable housing units in Maharashtra. These units are priced below market rates, making them attractive. However, the supply is limited, and the demand far exceeds availability, resulting in low chances of allocation for middle-class applicants.

Initiatives like the Mumbai Metro expansion aim to improve connectivity and reduce commuting times. While these projects enhance the quality of life, they often lead to increased property prices in connected areas, inadvertently making housing less affordable for the affluent middle class.

As a sub-scheme under PMAY-Urban, ARHCs aim to provide affordable rental housing for urban migrants and financially weaker societies. However, the focus remains on lower-income groups, with limited provisions for affluent middle-class families seeking affordable rental options.

Part of PMAY, CLSS provides interest subsidies on home loans for the Economically Weaker Section (EWS), Low-Income Group (LIG), and Middle-Income Group (MIG). While it extends to the middle class, the subsidy caps and property price limits often do not align with the high property prices in metropolitan cities like Mumbai, reducing its effectiveness for this segment.

While these initiatives have made strides in addressing housing affordability, they often fall short for the affluent middle class due to:

Middle-class families face significant financial strain as suburban property rates hover between ₹25,000 and ₹27,000 per square foot. A modest 2BHK unit priced at ₹1.75 crore vastly exceeds the affordability benchmark of five times annual income, leaving households to either overstretch finances or settle for smaller homes.

Existing schemes like Pradhan Mantri Awas Yojana (PMAY) and MHADA primarily target lower-income groups, leaving middle-class families unsupported. With flats priced under ₹1 crore in limited supply, accessibility remains a challenge for this segment.

Metro expansions and coastal road projects have spurred real estate inflation in adjacent areas. While Western Suburbs have given a return of about 10% over the last 4 quarters (Q3, 2023 to Q2, 2024) it has become difficult for new investors to buy at such high prices. Further straining affordability for middle-class buyers.

Rising interest rates and stringent lending norms exacerbate financial difficulties for buyers. A typical EMI for a ₹1.5 crore loan at 9% interest—amounting to ₹1.35 lakh per month—leaves little room for other essential expenses.

With the average RERA carpet area of a 2BHK unit in Greater Mumbai shrinking from 900 sq feet in 2014-15 to 700–750 sq ft in recent years., families face compromised living conditions while dealing with rising costs.

Developers prioritising high-margin luxury projects have created a significant shortfall in affordable housing. This trend marginalises middle-class buyers, pushing them further to the city’s periphery.

Affordable housing in Mumbai is not just a policy challenge but a critical need for the city’s middle-class families, who face rising costs, limited options, and shrinking living spaces. Addressing the challenge of unaffordable housing in Mumbai requires a nuanced approach that combines targeted policy reforms, innovative development strategies, and collaborative action among stakeholders.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Key Takeaways Bangalore’s tech sector drives strong demand for properties under...

Evaluate Knowledge Realty Trust REIT before investing

If you have bought a property from an NRI, or even just thought about it, you probabl...