Popular searches

Product scoring may vary based on gender, age, policy tenure and sum assured.

The lowest age in the selected range is considered for price evaluation (e.g., 25 - 29)

Connect with Our Financial Advisor

To create a comprehensive financial plan that is in line with the state of the economy in 2025, schedule a consultation with our Qualified Financial Advisor.

2024 was a year dominated by election-related uncertainties, both in India and abroad, with nearly half the world's population participating in elections across major economies. These political transitions, combined with geopolitical tensions and monetary policy shifts, created significant market volatility.

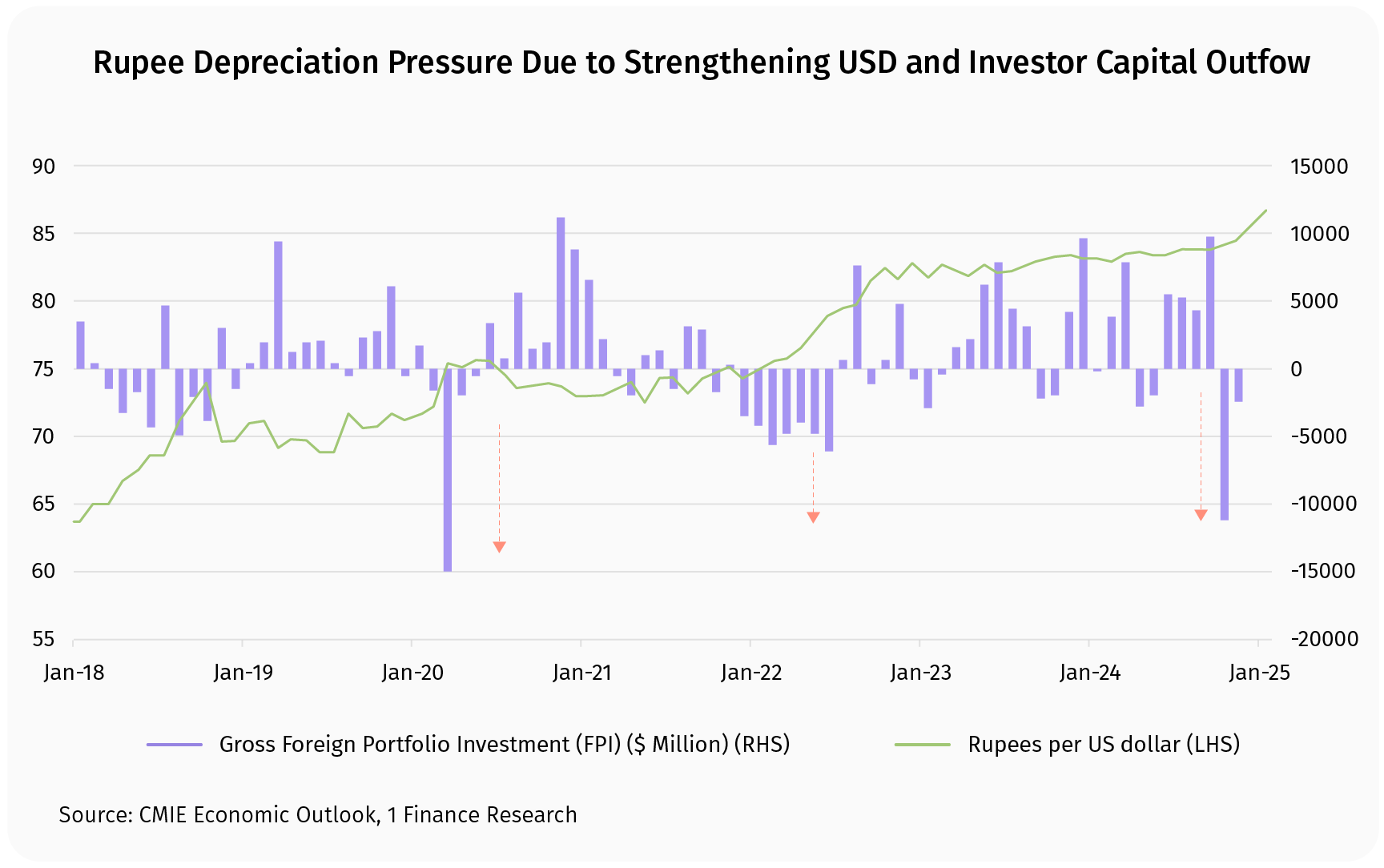

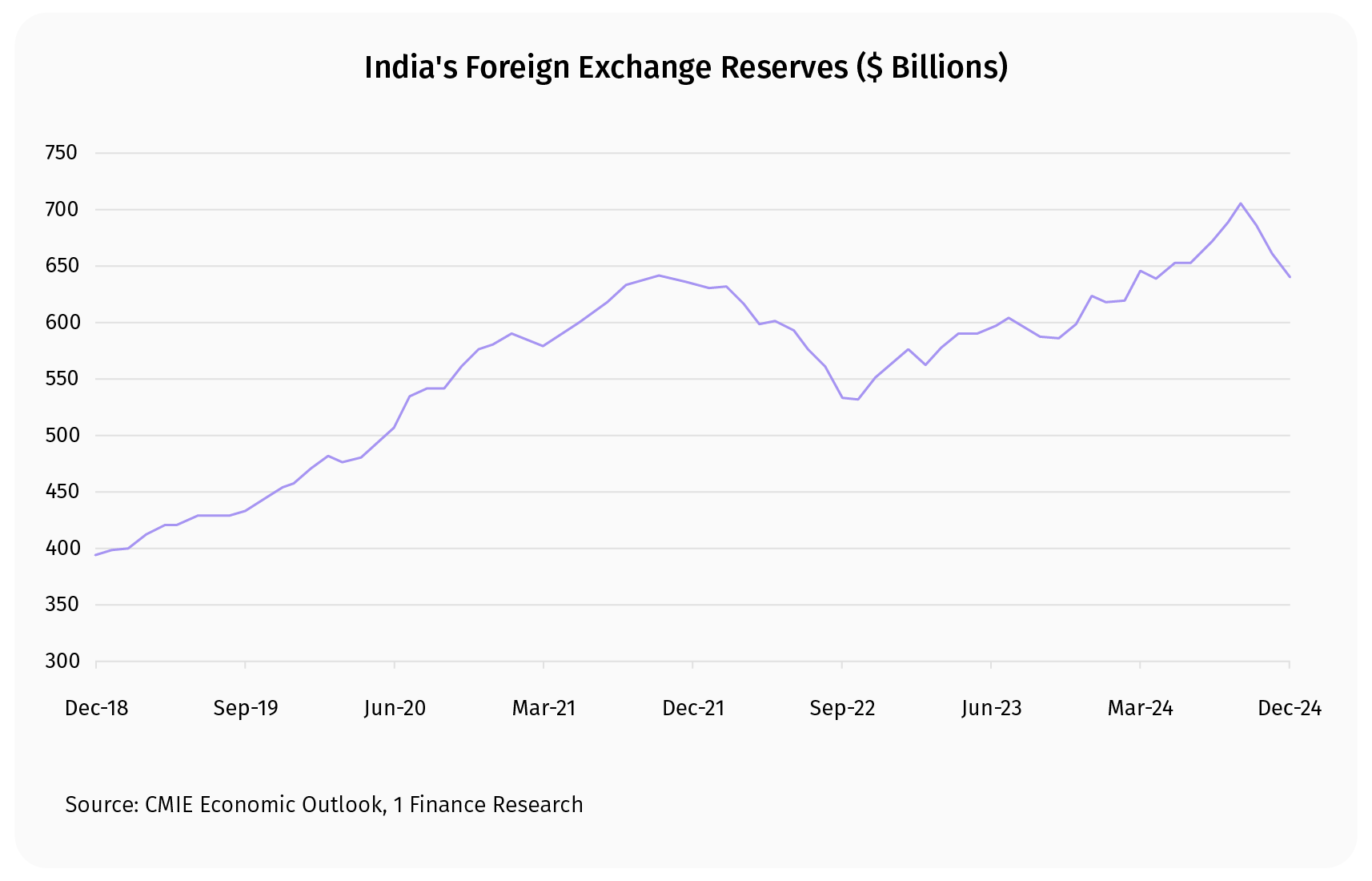

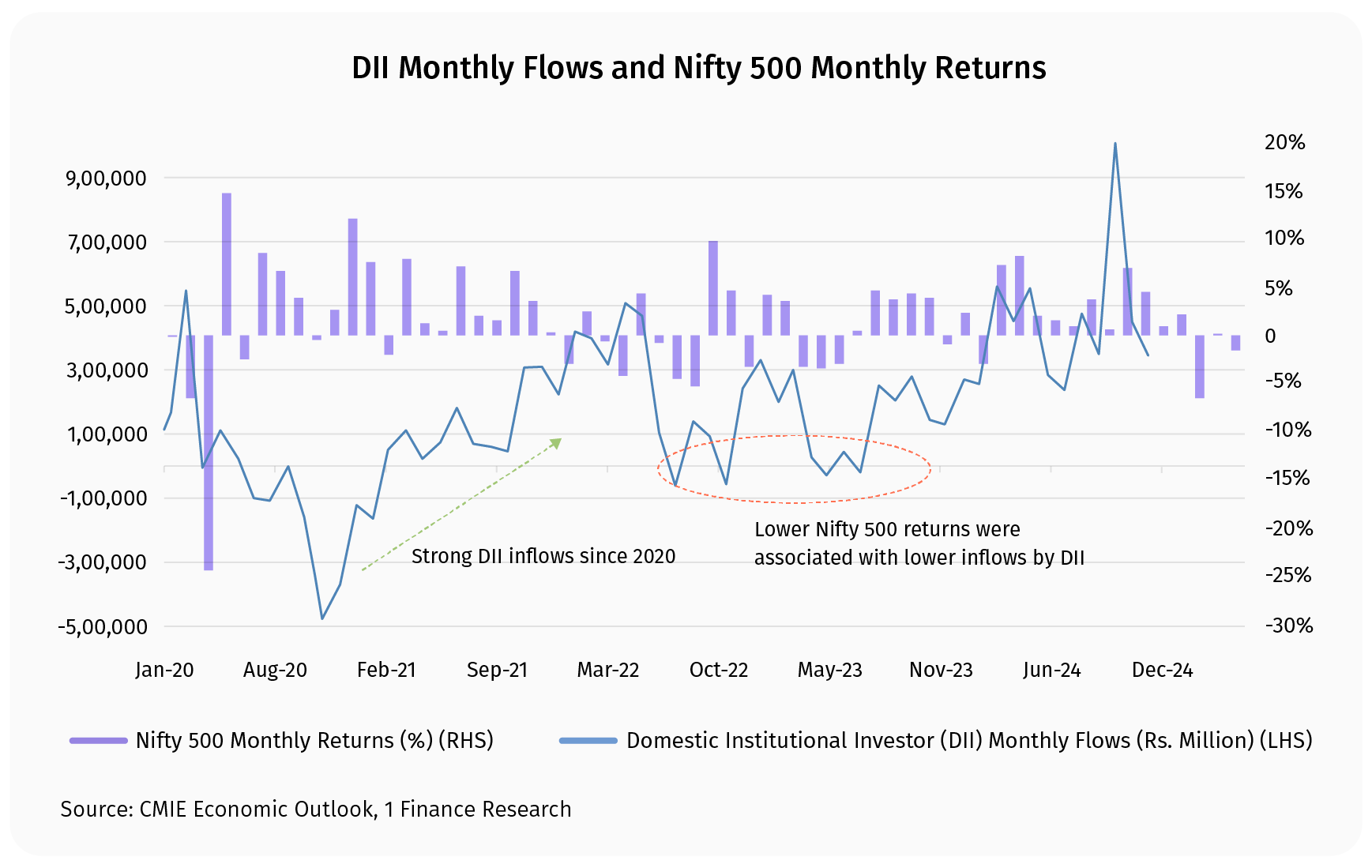

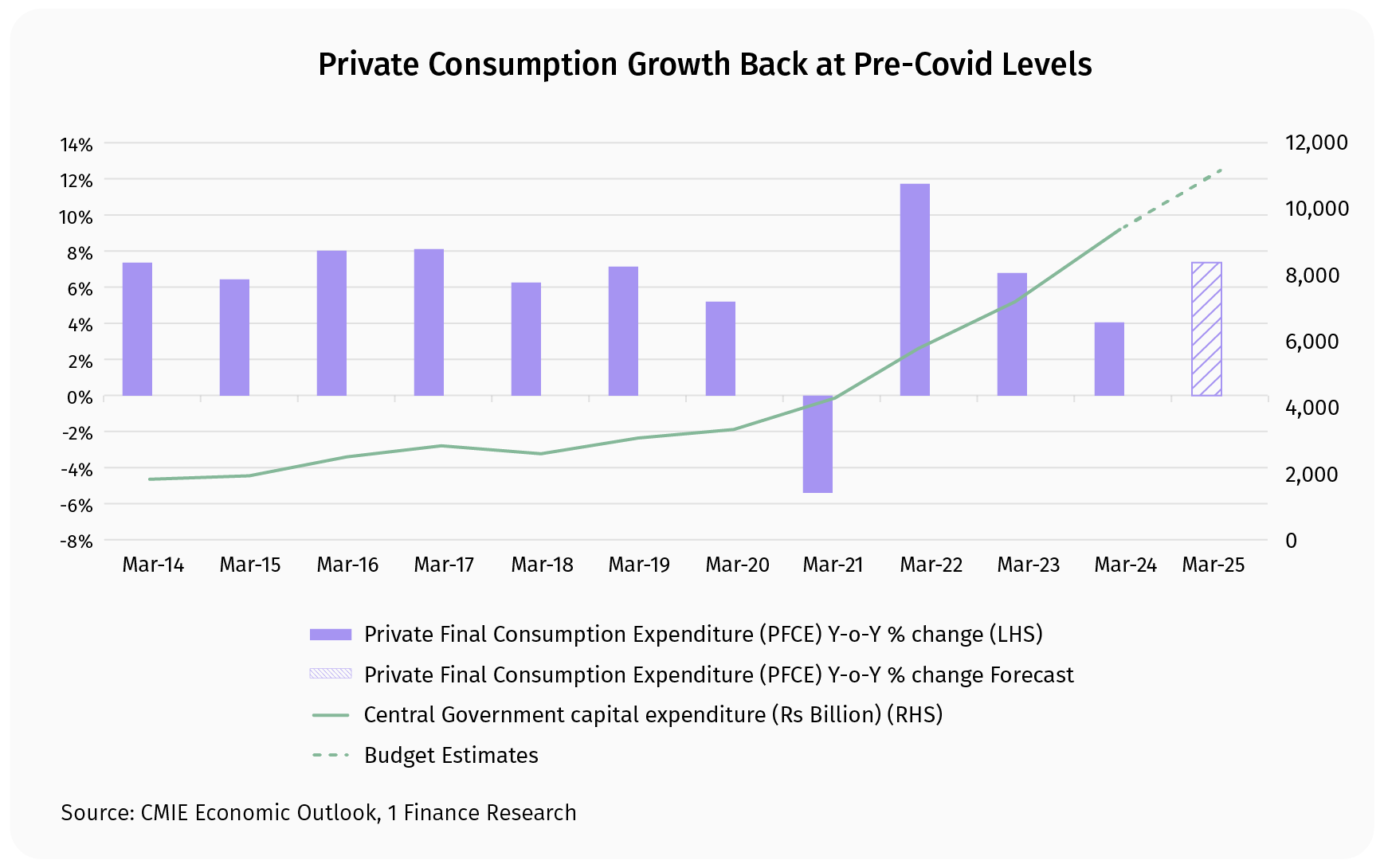

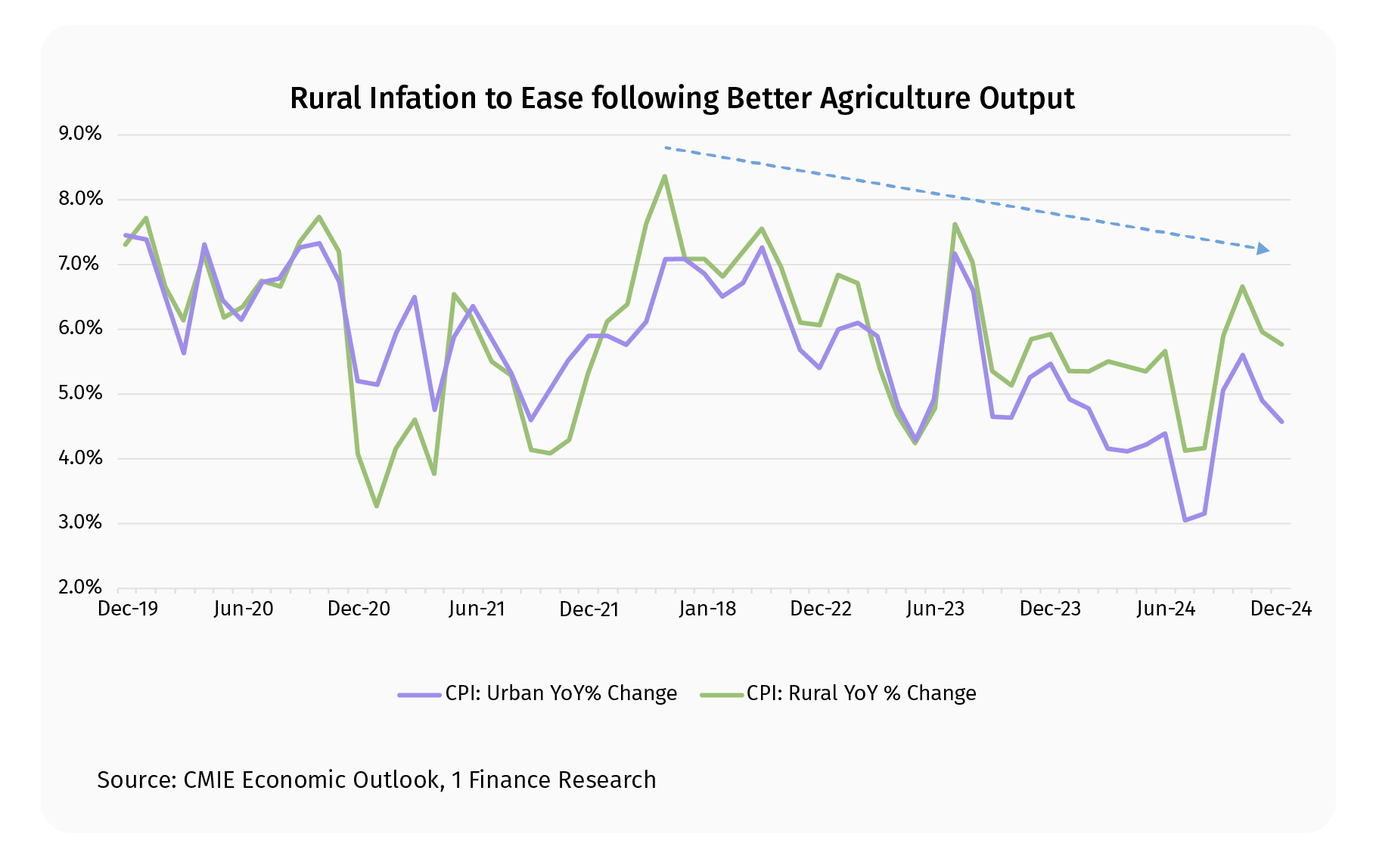

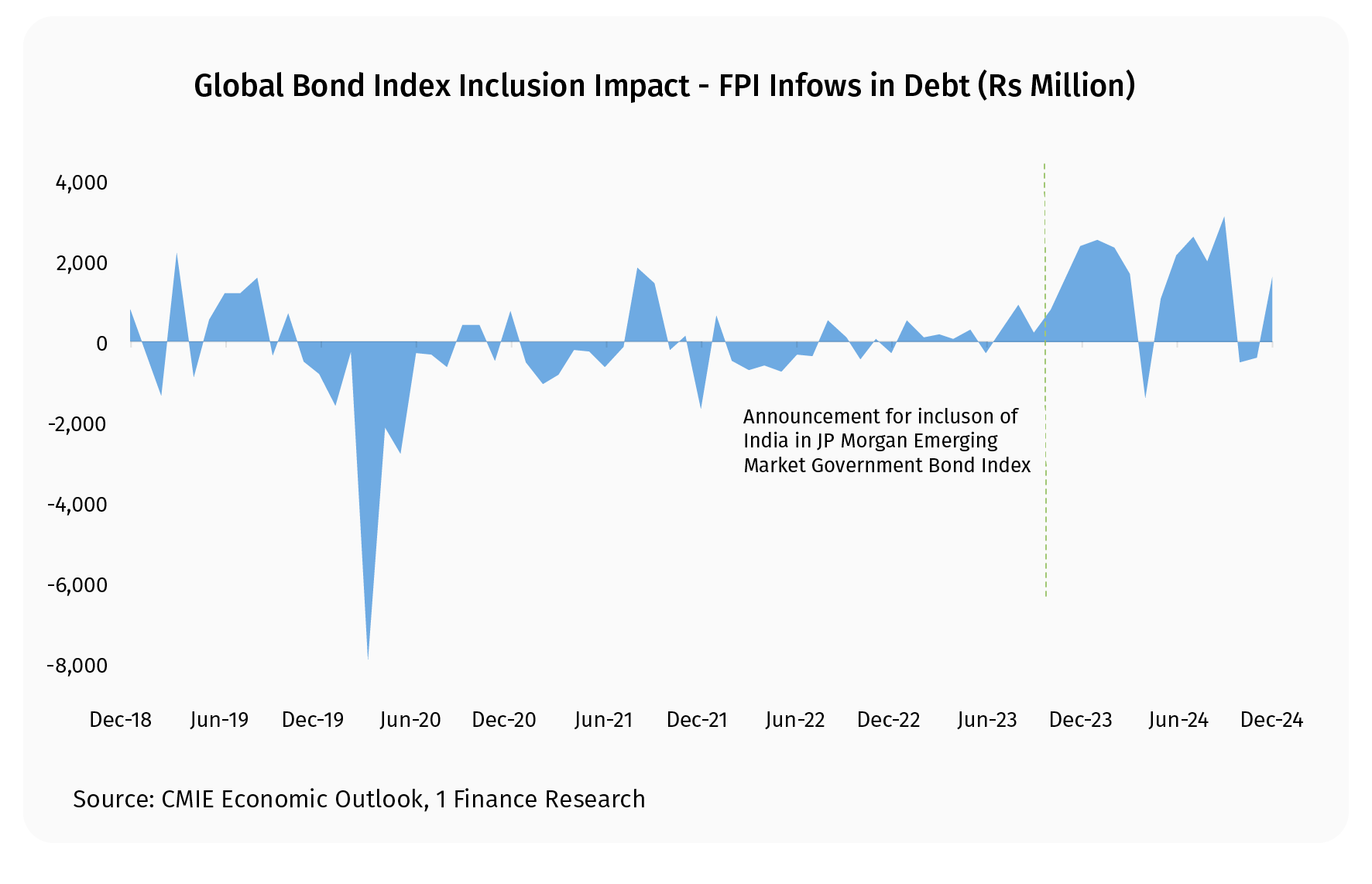

India’s economic growth took a hit because of several domestic and external factors like high and volatile food inflation, weak consumption demand, low employment generation, and low global growth. However, several positive catalysts emerged like strong credit growth, bond market inflows from FPIs and consistent inflows from domestic investors.

As we progress through 2025, India is poised to become the world's fourth-largest economy, surpassing Japan's $4.1 trillion GDP, though significant per capita differences remain. Below are a few factors that are working in India’s favour:

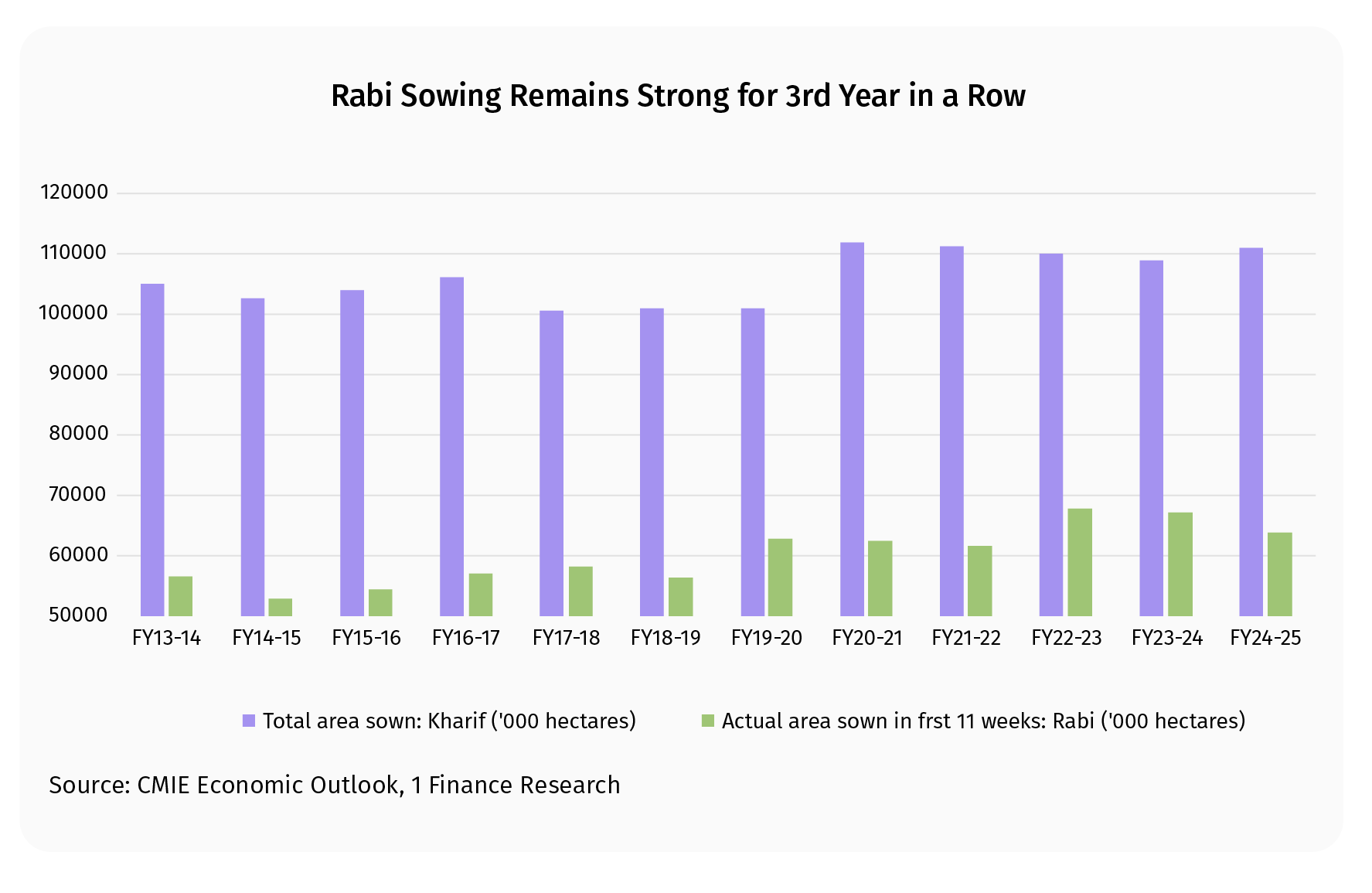

- Food inflation is moderating with strong agricultural output expected.

- Rural consumption is recovering, supported by good monsoons and falling agri input costs.

- The manufacturing sector shows readiness for capex with healthy balance sheets.

- Global growth, projected at 3.3% by the IMF, offers a marginal improvement over 2024's 3.2%, despite rising protectionist pressures.

This outlook weighs these factors to present our comprehensive analysis across asset classes, focusing on key themes that will shape investment opportunities in 2025.

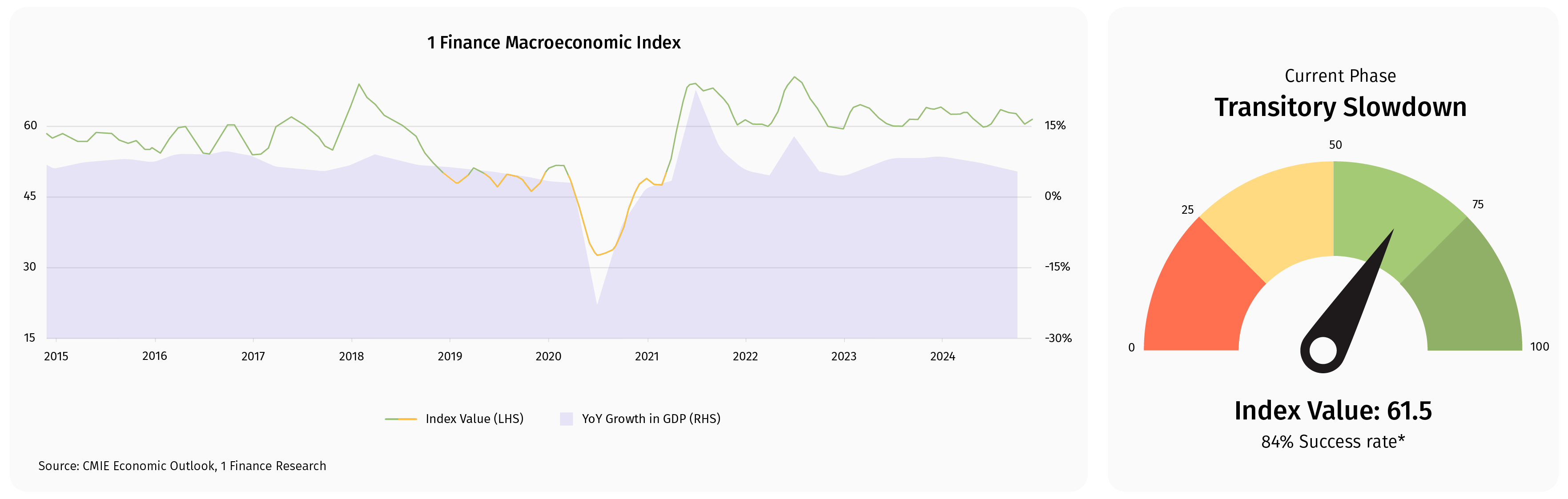

1FMI is an index integrating multiple sub-indices derived from high-frequency indicators, offering nuanced insights into India’s economic trends, phases, and near-to-medium-term outlook.

*Success Rate is a measure of how well 1FMI has historically predicted GDP Growth

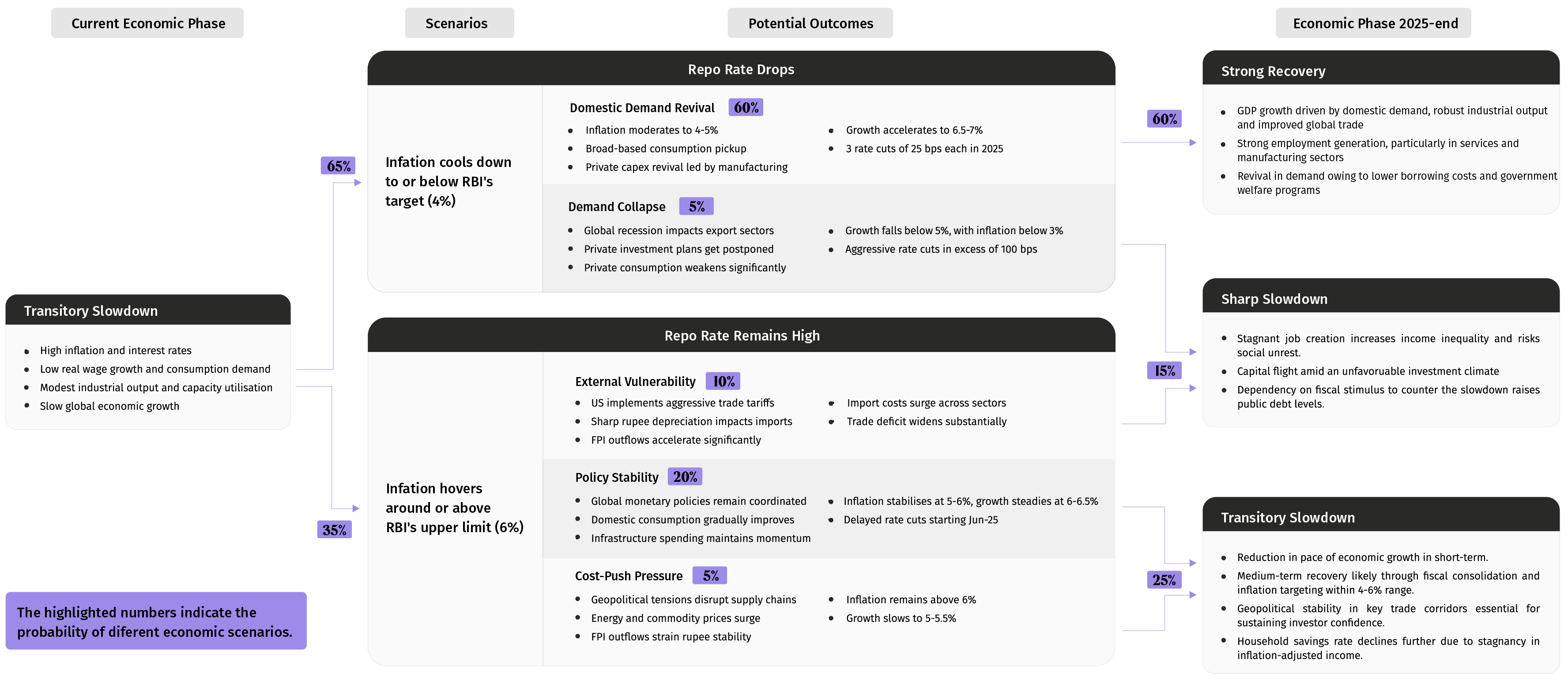

The probabilities stated reflect 1 Finance's proprietary framework combining quantitative and qualitative factors. Our methodology evaluates macroeconomic indicators to assess the likelihood of various scenarios, their probable outcomes and their transition into different economic phases.

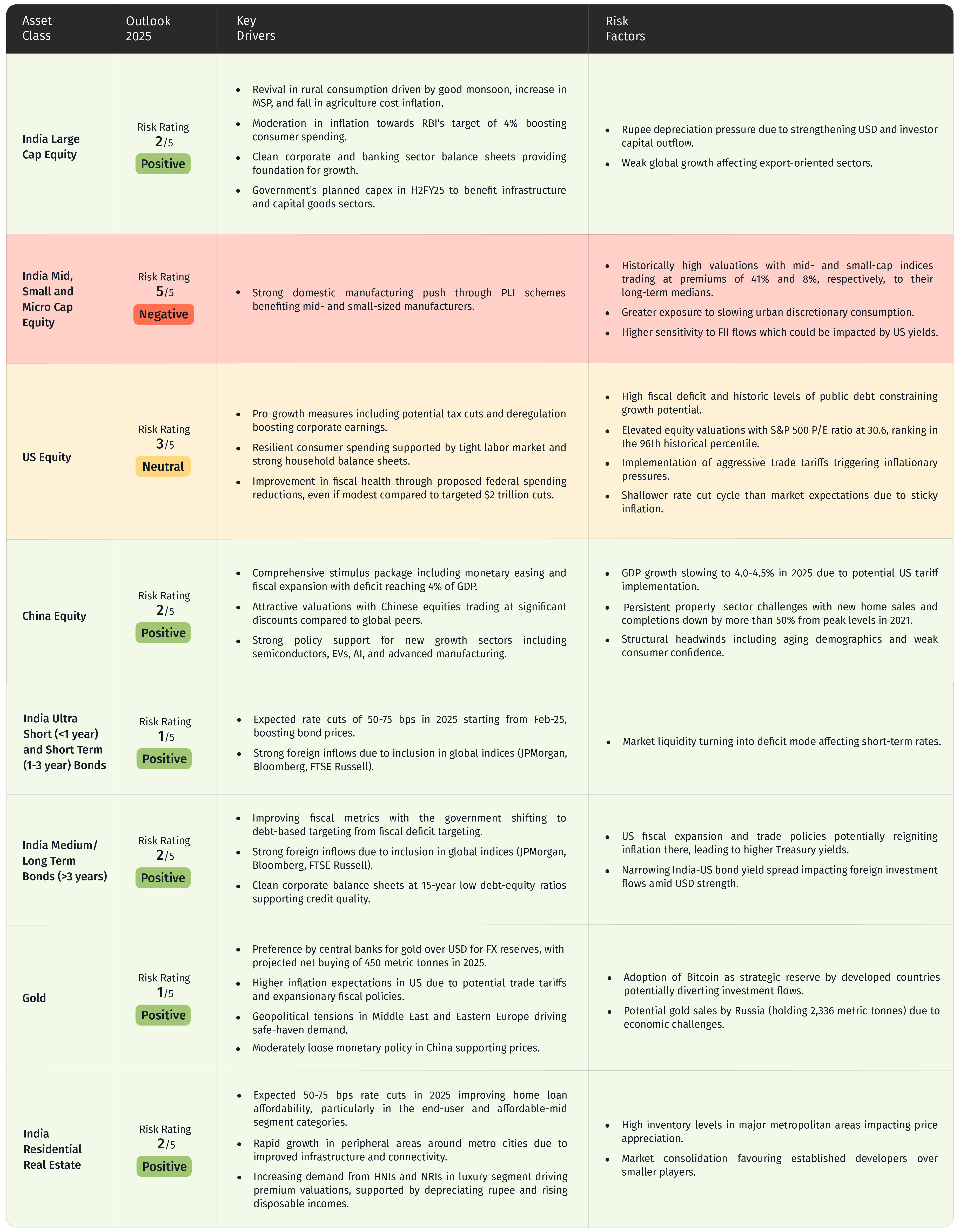

Risk Rating reflects 1 Finance's proprietary framework combining quantitative and qualitative factors to assess downside risks across asset classes. Our methodology evaluates macroeconomic indicators, valuations, and market dynamics to assign ratings from 1 (lowest risk) to 5 (highest risk).

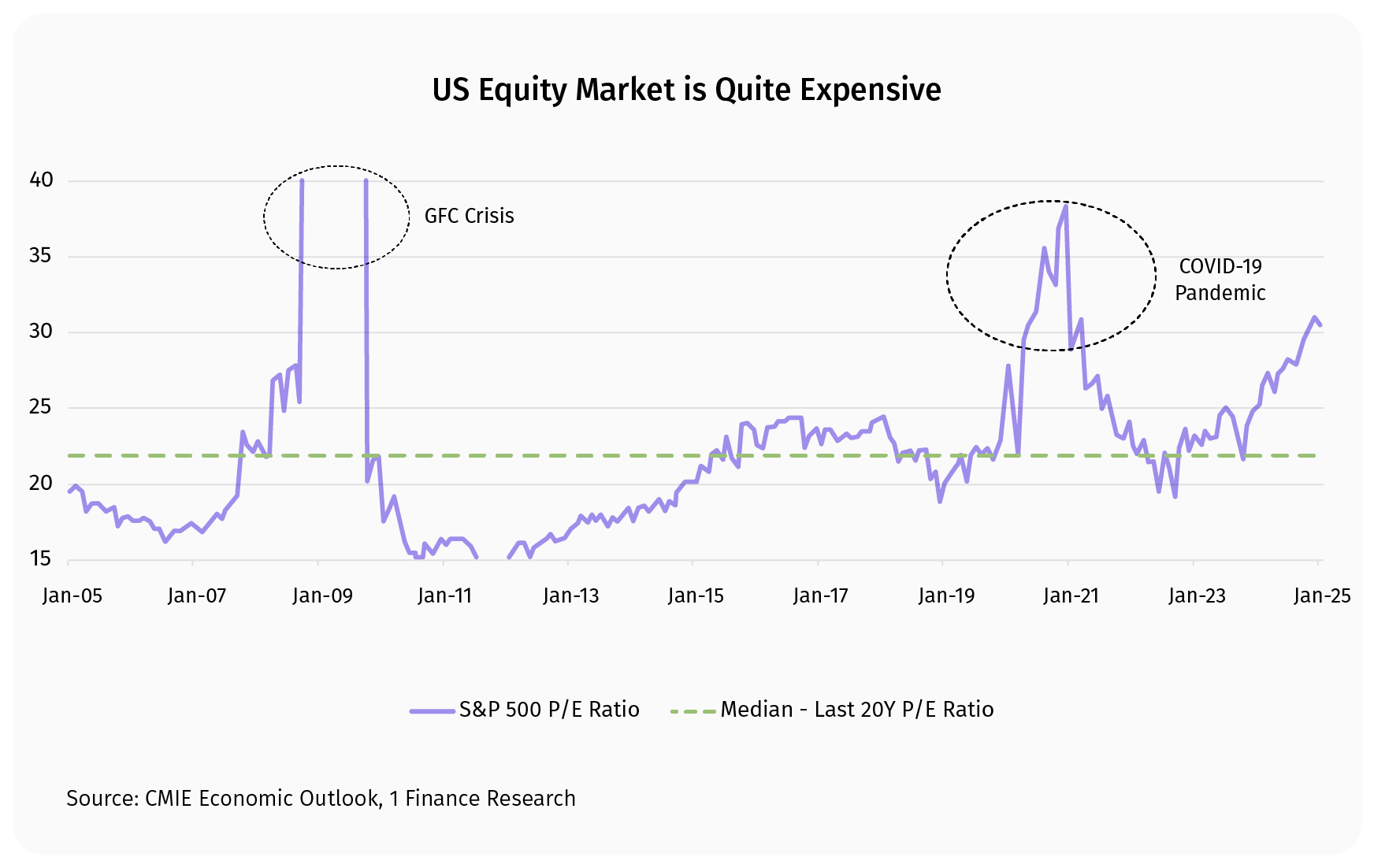

The proposed federal spending reductions, even if modest compared to the targeted $2 trillion cuts, could help improve fiscal health. However, this comes amid concerns about sticky inflation and potential trade tariffs that could trigger inflationary pressures. The Fed's likely shallower rate cut cycle than market expectations adds another layer of uncertainty.

The combination of high fiscal deficit, historic levels of public debt, and elevated equity valuations creates a challenging environment for US equities in 2025. While pro-growth measures including potential tax cuts could boost corporate earnings, the market appears to have already priced in an optimistic scenario.

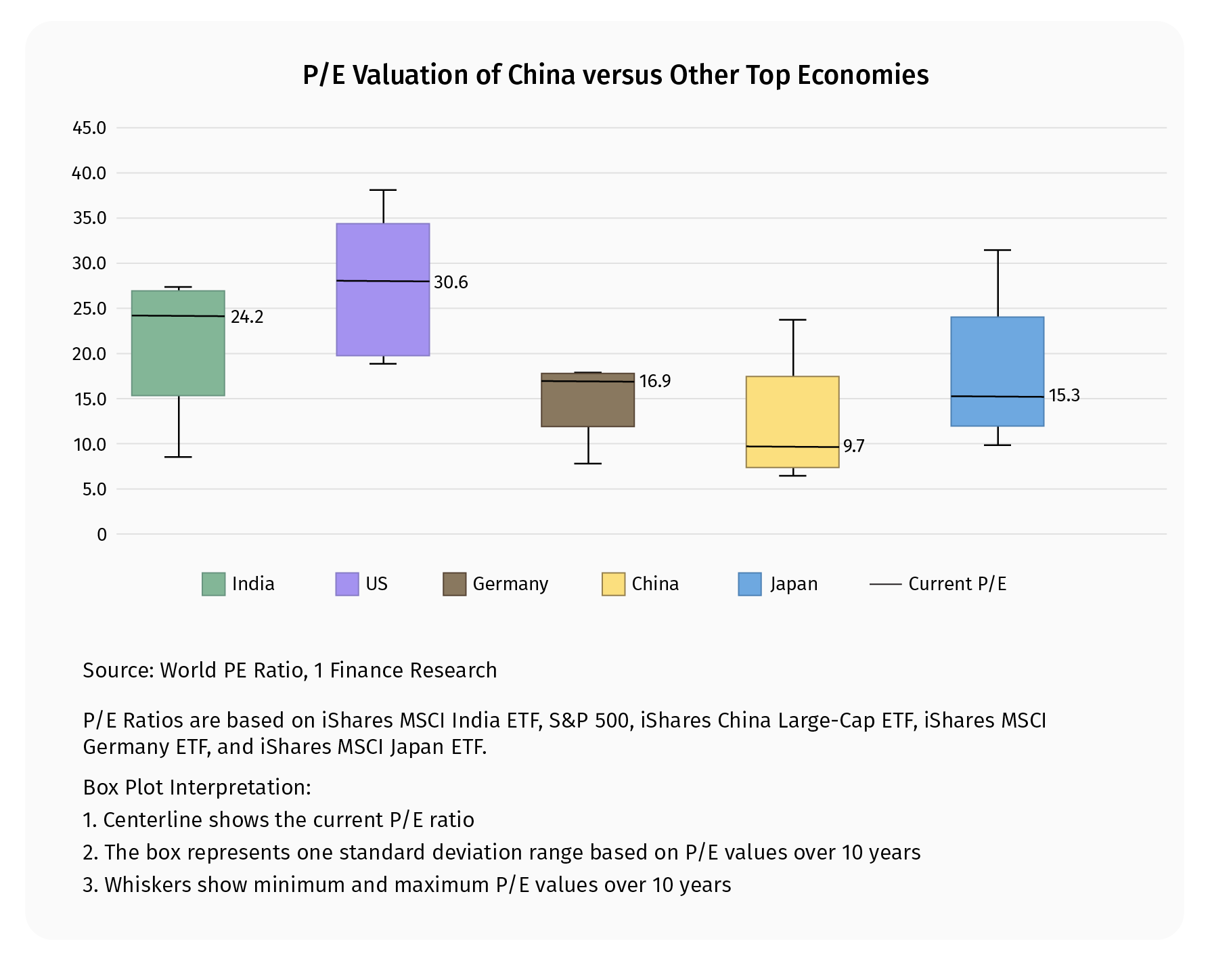

The government's strong policy support for new growth sectors, including semiconductors, EVs, AI, and advanced manufacturing, demonstrates a clear shift towards high-value industries. This transition, backed by moderately loose monetary policy, positions China's technology and manufacturing sectors for potential outperformance.

However, structural challenges persist. GDP growth is expected to moderate to 4.0-4.5% in 2025 due to potential US tariff implementation. The property sector continues to struggle, with new home sales and completions down by more than 50% from 2021 peaks. Ageing demographics and weak consumer confidence present additional headwinds that could limit the pace of economic recovery.

As we enter a period of significant economic transitions - from rate cuts to shifting global trade conditions - your financial decisions require careful consideration. A Qualified Financial Advisor can provide a comprehensive assessment of your financial situation:

- Evaluating loan refinancing opportunities as interest rates shift

- Protecting your purchasing power when the dynamics of inflation change

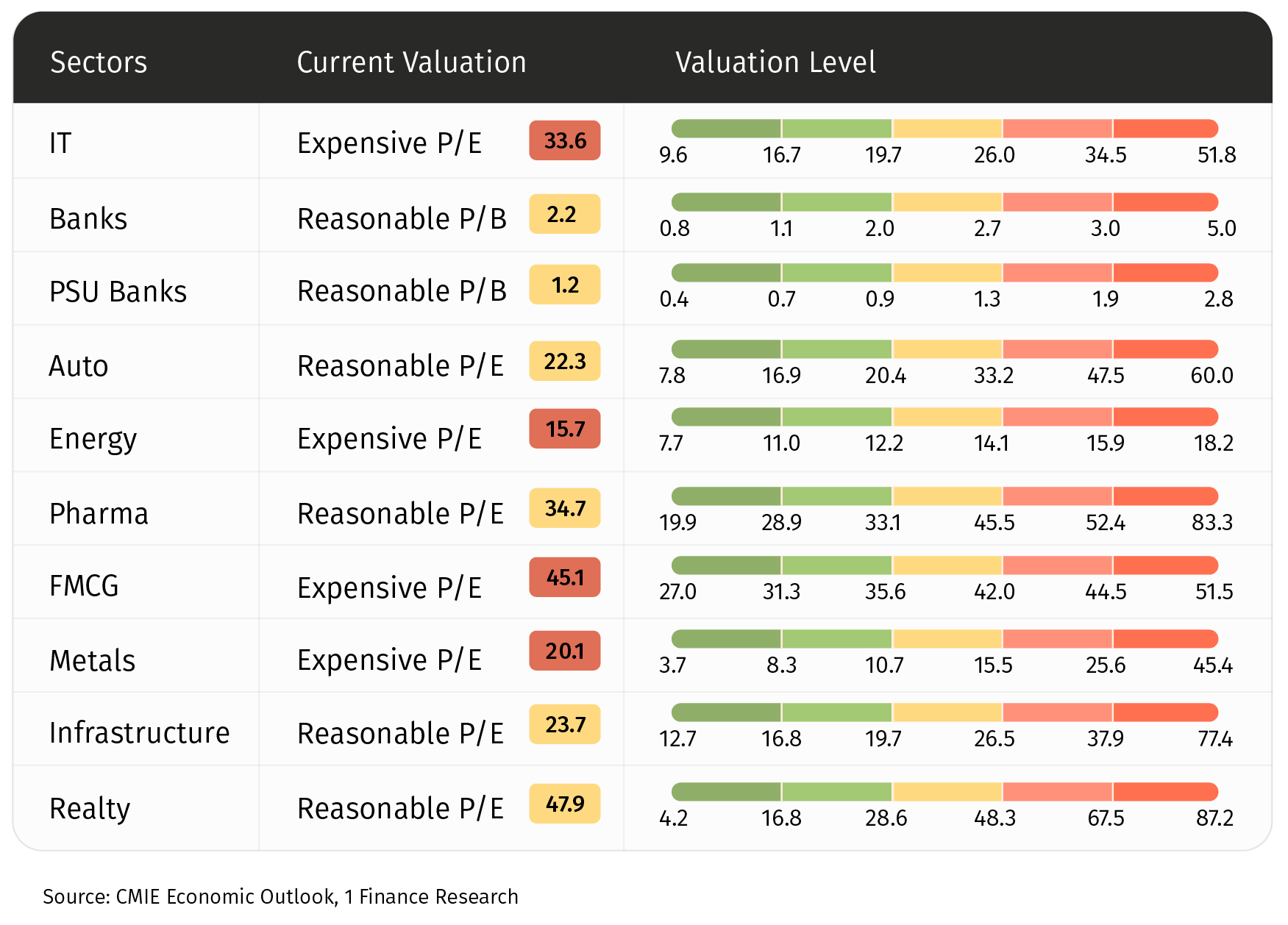

- Balancing exposure between large caps and mid/small caps given the valuation divergence

- Optimising fixed income allocation ahea0d of expected rate cuts

- Evaluating international diversification opportunities amid changing trade dynamics

- Assessing gold allocation as a hedge against market volatility