Comprehensive Guide to Exchange-Traded Funds (ETFs): What You Need to ...

Exchange-Traded Funds (ETFs) have become increasingly popular investment vehicles in ...

Priya, a 28-year-old IT professional based in Bangalore has recently received a bonus of Rs. 5 lakhs and wants to invest this money wisely. Priya’s parents have always favoured fixed deposits because they are flexible and safe – the guaranteed returns and complete capital protection offered by Fixed Deposits seem attractive.

However, Priya is also aware of another avenue which is becoming more and more well-liked, i.e. Debt mutual funds. Despite the market risk, they provide higher returns and offer similar stability.

So what shall Priya do? Should she follow the traditional wisdom and park the money in trusted fixed deposits? Or should she explore debt mutual funds instead? Bank fixed deposits (FDs) and debt mutual funds (DMFs) are two of the few well-liked investment choices for those seeking greater returns. FDs are safe, whereas Debt MFs have the potential to provide higher returns. In this blog, we will weigh the legacy appeal of FDs against the smarter flexibility of debt MFs which will help you gain better clarity when making this critical investment choice.

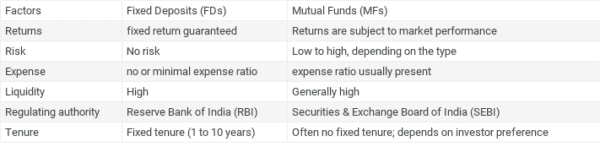

A fixed deposit is a financial product offered by banks and non-banking financial firms (NBFCs) that allows you to deposit a large sum for a certain period and earn a predefined rate of interest.

Individuals prefer bank fixed deposits (FDs) for several reasons.

Guaranteed returns: Fixed Deposits (FDs) offer guaranteed returns, with interest rates predetermined at the time of investment.

Benefits for taxes: Tax saving FDs are deductible up to Rs. 1.5 lakh under Section 80C of the Income Tax Act. Additionally, senior adults who earn interest on FDs are eligible for a tax benefit.FDs. If you invest 5 lakh rupees in an FD, you can claim a deduction of up to Rs. 1.5 lakh under Section 80C.

The tax savings will depend on your income tax slab rate. For example, if you fall in the 20% income tax bracket, the tax savings would be calculated as follows:

Tax Savings = Amount Invested × Income Tax Rate

Tax Savings = Rs. 1,50,000 × 20% = Rs. 30,000

So, in this example, you would save Rs. 30,000 in taxes by investing Rs. 5 lakh in an FD and claiming the maximum deduction under Section 80C.

Liquidity: If necessary, depositors of FDs have the option of early withdrawal, which allows them to take their money before the maturity date. But it might also lead to penalties and a drop in the interest rate.

Though all this may seem like an easy promise to build wealth for novice investors, let us look at some disadvantages of this way of investing.

Taxable Interest The interest earned on a fixed deposit is classed as ‘Income from Other Sources’ and is taxable in the investor’s hands. Because the FD interest is added to your total income and subsequently taxed, the tax rate that applies to you is determined by your income bracket.

For example, if you are in the 20% income tax band, your FD interest will likewise be taxed at 20%. Hence if you earn Rs. 35,000 of interest on an investment of 5 Lakhs you will be paying 20% of tax i.e. Rs. 35,000 × 20% = Rs. 7,000. This taxation occurs every year, regardless of whether you withdraw your FD or not.

The Tax saving FDs will have lock-in period of 5 years -A potential disadvantage of Tax Saving Fixed Deposits is the mandatory lock-in period of 5 years, which means investors cannot access their funds during this time without forfeiting tax benefits.

Reduced Profits: Fixed deposits typically yield lower returns on investment compared to other investment options, although they are considered safer. The FD rate is influenced by factors such as the bank, your age, and the duration of the deposit. One of the primary drawbacks of fixed deposits is their relatively lower interest rates compared to alternative investment options. For example, Equity Linked Savings Schemes (ELSS) typically offer interest rates ranging from 10% to 15%

Penalties for Early Withdrawal: An excellent feature of FDs is the premature withdrawal facility, but it comes with a price. Banks typically charge a penalty when you choose to withdraw your fixed deposit early, which may range from 1% to 3% of the total amount of interest.

Maybe Not Enough to Beat Inflation: After taxes are deducted, ideally, an investment’s return should exceed the current inflation rate. However, the interest rate on a fixed deposit typically falls short of the inflation rate. For instance, with FD rates around 7% and inflation upwards of 5%, the compounded effect may result in insufficient returns in the end. Hence even if you earn an interest of, after a year, the value of money will decrease due to inflation. The real return on the FD would be calculated as follows:

Real Return = Nominal Return – Inflation Rate = 7% – 5%= 2%.

So, after accounting for inflation, the real return on the FD is only 2%. This means that even though the FD earns 7% interest, the purchasing power of the returns is eroded by inflation.

Interest rate loss if you withdraw in between: Withdrawing funds before the maturity date, can lead to a loss of interest, diminishing the overall returns on the investment.

Can not withdraw partial amount: FDs generally do not allow the partial withdrawal of funds before maturity, requiring investors to either break the entire deposit or wait until the end of the term to access their money.

Investors who are risk averse: Because fixed deposits ensure a return on investment, they are seen as low-risk investment options. FDs are an option for investors who do not want to take on any risk.

Seniors: Banks frequently give older persons better interest rates on fixed-rate deposits (FDs). Seniors searching for a secure investment choice with better returns should therefore give FDs more thought.

A debt fund is a mutual fund scheme that invests in fixed-income instruments, such as Corporate and Government Bonds, corporate debt securities, and money market instruments etc. that offer capital appreciation. Debt funds are also referred to as Income Funds or Bond Funds.

Debt funds are less volatile and, hence, are less risky than equity funds. If you have been saving in traditional fixed-income products like Term Deposits, and looking for steady returns with low volatility, debt mutual funds could be a better option, as they help you achieve your financial goals in a more tax-efficient manner and therefore earn better returns.

Here the fund manager invests in a basket of bonds and securities and earns interest regularly.

There are various types of debt funds, high-risk funds and low-risk funds, investors should also choose investing based on their investment horizon.

Reduced Risk Elements: In terms of risk, debt funds, particularly debt mutual funds, are characterised by reduced risk elements compared to investments in the stock market. Unlike stocks, the volatility of the share market does not directly impact debt funds. Instead, they are primarily influenced by interest rates and their movements within the broader economy. While interest rates can fluctuate, these fluctuations are typically not as extreme as those witnessed in the stock market. Debt funds invest in assets that offer fixed returns, such as bonds, with predetermined interest rates and maturity dates. Consequently, the risk associated with debt mutual funds is considerably lower, making them a more stable investment option.

Professionally managed: Professional fund managers, armed with the knowledge and tools required for investment analysis and wise decision-making, oversee mutual funds. Consequently, investors can benefit from the experience of these fund managers.

Flexibility: You can make a one-time or ongoing systematic investment plan (SIP) or lump sum investment in mutual funds. The amount that can be invested is unlimited.

Tax Benefit on Redemption Section 54F of the Income Tax Act provides individuals and HUFs with an exemption from long-term capital gains arising from the sale of assets other than residential houses. To qualify, the net sale consideration must be invested in a residential property within a specified timeframe, contingent upon meeting specific conditions. Notably, this exemption is applicable only if the individual or HUF does not own more than one house on the date of the asset sale.

Taxation arises only when you withdraw your funds and book capital gain

Better return than Bank FD – Debt mutual funds often offer the potential for higher returns compared to traditional Bank Fixed Deposits (FDs). While FDs provide guaranteed returns at fixed interest rates, the returns are typically lower compared to the potential returns from debt mutual funds. Debt funds invest in a variety of fixed-income securities, such as government bonds, corporate bonds, and money market instruments, which may yield higher returns over the long term. Additionally, the flexibility of debt mutual funds allows fund managers to actively manage the portfolio to capitalise on market opportunities and maximise returns. Therefore, for investors seeking higher returns while maintaining a certain level of safety and stability, debt mutual funds can be a preferable alternative to Bank FDs.

No lock-in period – After the exit load period expires, investors can withdraw their funds at any time without incurring additional penalties, and they can continue to enjoy the same returns.

You might be tempted to invest in MFs to avail these benefits, but before that, let’s examine the disadvantages:

Variable Returns: Returns on mutual funds are not fixed percentage like bank FD. these returns may stay in a range depending on the category of debt fund but will not stay same percentage.. Therefore, before investing, investors need to be informed of the fund’s risk profile.

Does not offer guaranteed returns like bank FD – Unlike bank FDs which offer guaranteed returns at fixed interest rates, debt mutual funds do not provide such assurances. The returns from debt mutual funds are subject to market risks and may fluctuate based on the performance of the underlying securities in the fund’s portfolio.

Post removing the Indexation benefit the taxation is the same as bank FD –Post removing the indexation benefit, the taxation on debt mutual funds becomes comparable to that of bank fixed deposits (FDs). Without the advantage of indexation, both debt mutual funds and bank FDs are taxed similarly. Interest income from both investments is subject to tax at the investor’s applicable income tax slab rate.

Interest rate movement risk – Interest rate movement risk” refers to the potential risk associated with changes in interest rates that may affect the value of investments, particularly fixed-income securities in debt mutual funds. When interest rates fluctuate, the prices of fixed-income securities can experience changes inversely correlated with the movement of interest rates.

For example, when interest rates rise, the prices of existing fixed-income securities tend to decrease, as newer securities with higher interest rates become more attractive to investors. Conversely, when interest rates fall, the prices of existing fixed-income securities may increase, as they offer higher yields compared to newly issued securities with lower interest rates.

Corporate default risk – if there is a default by any corporates the losses are borne by investors. When a DMF invests in corporate bonds or other debt instruments issued by corporations, there is a risk that one or more of these corporations may default on their payments. If a default occurs, it can lead to a decline in the value of the affected securities held by the mutual fund. As a result, the Net Asset Value (NAV) of the DMF may decrease, causing losses for the investors who hold units of the fund.

Not Beginner Friendly: For novice investors, navigating Debt Mutual Funds (DMFs) can be overwhelming due to the variety of options available. With numerous types of debt funds offering different risk profiles and investment objectives, selecting the right one can be challenging. Simplifying the selection process through educational resources, risk profiling tools, and user-friendly comparison platforms can make DMFs more accessible to beginners. Additionally, seeking guidance from financial advisors can provide personalised recommendations tailored to individual investment needs, helping new investors make informed decisions and embark on their investment journey with confidence.

For many years, FDs have been the preferred choice for Indian investors. As a result, many investors buy them without even giving them a second thought. Mutual funds, though, might be a superior choice. They are not only more capable of producing returns, Mutual funds do not require tax payment while your earnings are growing. Only when you sell or redeem your mutual fund units for a profit, you have to pay taxes. Not with FDs, though. Even when interest is being accrued, FDs are subject to taxation. Also, mutual funds perform rather well in terms of outpacing inflation.

For top mutual funds scored and ranked by us do visit the 1 Finance Mutual Fund scoring and ranking page!!

Always consult a qualified financial advisor to choose the right debt mutual funds for your requirement.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Fixed Deposits are investment instruments offered by banks and non-banking financial companies, where you can deposit money for a higher rate of interest than savings accounts for a certain period. Hence answer to the question "What are Fixed Deposits"

Tax efficiency refers to the ability of a mutual fund to generate returns while minimizing its tax liability. A tax-efficient mutual fund minimizes capital gains, dividend, and income distributions to investors, reducing their tax burden.

While mutual funds can offer higher returns, they also come with risks. Market volatility can impact your fund's value. However, over the long term, these risks are often balanced out by the potential for higher returns. It's crucial to choose funds that align with your risk tolerance and retirement goals.

Exchange-Traded Funds (ETFs) have become increasingly popular investment vehicles in ...

Choosing between a new fund offer (NFO) and an existing mutual fund scheme depends on...

When it comes to investing in mutual funds, people generally fall into two camps: tho...