10 financial mistakes people make before divorce, and how to avoid the...

This financial mistakes before divorce will ruin you

Identify the personality traits and behavioural patterns that shape your financial choices.

The Public Provident Fund (PPF) is a mainstay of long-term investment in India. There are several reasons, including government backing that ensures the safety of capital, tax free interest income and even a reduction of taxable income on investment under Section 80C of the Income Tax Act, 1961.

An Indian citizen can invest up to ₹1,50,000 every financial year in PPF. The initial tenure of PPF is 15 years, which can be extended in blocks of 5 years after that.

You all must be aware of the conditions attached to investments in PPF around premature withdrawal. If not, let us talk about the impact on your withdrawal amount in case you have to withdraw within the extended block of 5 years after initial maturity.

There’s an interesting change that you need to know about. We’ll cover that as well in this article.

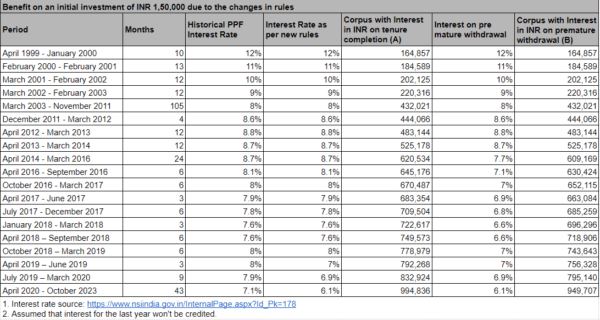

The previous rules were such that if you had to withdraw in, say, the 25th year, i.e., before completion of the tenure of 25 years (initial tenure of 15 years plus 5 years of tenure extended twice), the rate(s) at which you were credited interest from the 15th year onwards, i.e., after initial maturity of the PPF account, would get reduced by 1% each year.

Say, you had to redeem the investments in the 25th year due to some emergency.

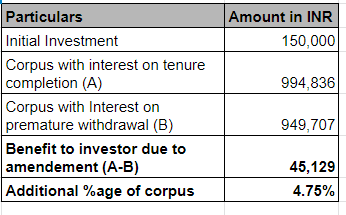

As per the existing rules, your initial investment of ₹1,50,000 (on April 1, 1999) will yield 1% less interest per year since the year 2014, i.e., after completion of the initial tenure of PPF of 15 years. This would yield a corpus of ₹9,49,707.

However, the new rules mandate that 1% less interest will apply only from the date of commencement of the current block period of five years, i.e., April 1, 2019, assuming that you extend your tenure to a block of 5 years immediately after completion of one extended block of 5 years ending on March 31, 2019.

As per the new rules, your corpus would yield ₹9,94,836 assuming a pre-mature withdrawal is made in the month of November 2023.

This simple change can drive ₹45,129 of additional corpus for investors or 4.75% more on the corpus that would’ve been withdrawn before the change in this rule.

Some advisors have interpreted that the penalty of 1% lesser interest in the previous law was applicable from the first year of making investment, i.e., in our case, the year 1999. However, we do not agree with this view.

This amendment is a boon, particularly for long-term investors. For those considering liquidity, this change also reduces the financial penalties associated with early withdrawals, allowing for more strategic financial planning.

Financial advisors and industry experts largely view this amendment as a positive development. “It aligns the PPF more closely with the needs of today’s investors, who require both stability and flexibility,” remarks a leading financial planner. Such insights underscore the importance of staying updated with policy changes and their potential impacts.

Given these changes, investors should re-evaluate their PPF strategies. It’s advisable to consider PPF as part of a diversified investment portfolio, balancing it with more liquid assets. Investors should also review their long-term financial goals and consult with financial advisors to optimize their investment plans in light of these amendments.

The recent changes to the PPF scheme are a significant development in India’s investment landscape. They offer a more investor-friendly approach, balancing security with flexibility.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Identify the personality traits and behavioural patterns that shape your financial choices.

This financial mistakes before divorce will ruin you

Empower future generations with financial literacy through this essential guide to te...

The Union Budget 2024 brings significant changes to the taxation of gold investments,...