Death doesn’t come knocking. Apart from dealing with the emotional pain of losing a family member, the family also goes through a lot of struggle in getting the assets of the deceased transferred in their name.

More so, you would have seen that people in their 50s and 60s do not even recall all their demat accounts, bank deposits, matured insurance policies, etc. Even if someone were to make a will and a proper succession plan, how would they plan for the transmission of such assets?

But SEBI’s recent circular can help the family members of the deceased person discover the shares, mutual funds, etc., they did not even know existed.

How will this happen? Let us discover this in this article.

But before this, let me explain… ‘The Problem of Unclaimed Assets in India’

₹82,025 Crores lying in unclaimed bank accounts, life insurance, mutual funds, and PF

An article shared by the Economic Times in 2021 claimed that ₹82,025 crores were lying in these financial instruments.

Another article shared by The Hindu claimed that ₹1,50,000 crores are lying as unclaimed deposits/amounts with various Indian banks and insurance companies as of December 2020.

The article by Economic Times further shared that on the completion of 25 years of a flagship equity scheme, the fund house wrote to the investors who remained invested for more than 20 years. What followed was a perplexing flurry of redemptions from the “long-term investors.”

Clearly, it shows that people don’t even know where all their assets are parked. The magnitude of unclaimed assets, as you can see, is so huge, i.e., ₹82,025 crores.

But the authorities are working hard towards resolving this problem. Be it the RBI’s UDGAM Portal, which helps users get information about their bank deposits, or SEBI’s circular to implement a centralised mechanism for reporting the demise of an investor through KRAs.

SEBI mandated centralised mechanism to report the demise of an investor through KRA

Let’s understand how the SEBI mandated centralised mechanism will work.

Say Mr. Dad had three demat accounts, one each with HDFC Securities, ICICI Securities and Groww. Mr. Son (Mr. Dad’s son) knew about his father’s demat account with Groww but not the ones with HDFC Securities and ICICI Securities.

Unfortunately, Mr. Dad passed away due to COVID. At present, Mr. Son would be in a position to get only those securities transferred in his name that he knows exist, i.e., the ones that lie in Mr. Dad’s Groww’s demat account. The ones lying with HDFC Securities and ICICI Securities might never be discovered.

Mr. Mayank Lunawat of Green Stapler told us that the SEBI mandated mechanism, which will come into effect w.e.f. January 1, 2024, will help Mr. Son discover the securities lying in the demat accounts of HDFC Securities and ICICI Securities as well.

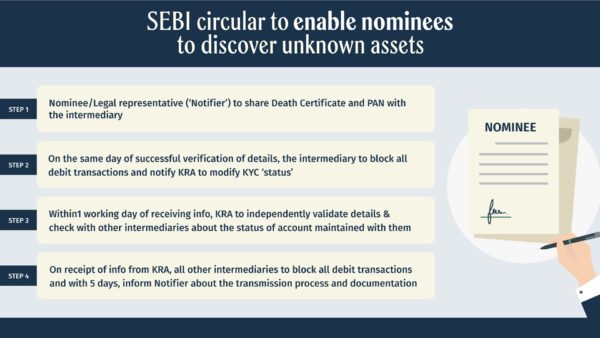

But how? Once Mr. Son shares Mr. Dad’s death certificate and PAN with the intermediary (a broker or Groww in this case), the intermediary (Groww) will verify the details.

On successful verification of details, the intermediary will block all debit transactions from Mr. Dad’s account and ask the KRA to modify KYC status on the same day of successful verification of details.

Within one working day of receiving the information, the KRA will independently validate the details and check with other intermediaries about the status of the account maintained with them.

On receipt of information from the KRA, all other intermediaries must block all debit transactions within 5 days and inform Mr. Son about the transmission process and documentation.

If implemented well, this step from SEBI can help the investors’ nominees / legal representatives get access to funds that they are the rightful owners of. The funds that deceased family member worked hard to generate but couldn’t get a chance to talk about in their lifetime.

Mrs. Shilpa of Green Stapler added, “Please note that it’ll be possible for the KRA and intermediaries to perform this process only if you have appropriately performed your KYC process with them.”

Small efforts required from investors end up leading to a smooth transmission process

While Mr. Son will definitely get access to assets he didn’t know about, the transmission process might get painful if the nominees are not appropriately declared with the intermediaries.

Mr. Nikhil Varghese of Yellow told us that if the nominee information is not appropriately disclosed, the transmission process might require you to get the deceased’s Will probated by the court if jurisdiction falls within the cities of Mumbai, Chennai and Kolkata, which takes around six months or more.

“If the deceased didn’t leave a Will, a succession certificate will be required to be obtained from the court, but that can take ‘n’ number of years if the legal hiers are not in agreement. Hence, it is very important that everyone get a Will drafted by a professional and get it registered. An ill-drafted Will can also be the cause of conflict between legal representatives of the deceased,” Mr. Nikhil added further.

Nominee is only a custodian or trustee of the asset but not a legal heir. Whether or not you have made an appropriate nomination, a legal heir is determined either by a Will or in its absence by Indian succession laws. Further, the transmission isn’t restricted to only shares and securities as one leaves assets like real estate, bank deposits, jewellery, etc. as well. Thus, irrespective of whether one has a nomination in financial assets or not, it is important to have a valid Will to avoid any conflict between legal representatives.

Financial planning is the architecture of your entire life’s choices—every goal, every risk, every decision flows through it. It’s not about chasing returns, but creating alignment between income, expenses, assets, and aspirations. Our Qualified Financial Advisor helps you design a cohesive plan that adapts to life’s changes while keeping your long-term vision intact—so your money works in harmony with your purpose.

Conclusion:

With this information, the key action points for the readers should be to:

1. Share this information with their loved ones,

2. Complete the KYC procedure and fill nomination details with all their intermediaries and

3. Speaking to the family about succession planning and getting a Will drafted and registered.

As we had begun the article saying, “Death doesn’t come knocking,” so do not wait for you to turn 60 to write your Will or complete your KYC process. If you or your loved ones have assets, get started with all this today.