Back

Equated Monthly Installments (EMIs)

Search for a word

Introduction

Equated Monthly Installments (EMIs) are fixed monthly payments combining both principal and interest, designed to help you repay loans over a set period.

As of March 2025, EMIs continue to be a key part of debt management in India, allowing people to afford major expenses like homes, education, and vehicles without needing all the cash upfront.

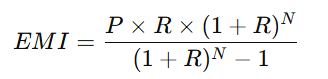

The formula to calculate an EMI is:

Where: P = Principal (₹)

R = Monthly interest rate

N = Loan tenure (months)

For example, a ₹50 lakh home loan at 8.5% interest over 30 years results in an EMI of around ₹38,446.

Why EMIs Matter in Financial Planning

EMIs create predictable expenses, making it easier to budget and manage cash flow. Knowing your fixed monthly outgoings helps you plan for other financial commitments.

Paying EMIs on time also builds your credit score, improving your chances of getting better loan offers in the future.

EMIs have made high-cost purchases more accessible, even on everyday items like electronics, thanks to options such as "No Cost EMI" on digital platforms.

Challenges of EMI-Based Loans

One major downside is the interest burden. Longer loan tenures reduce your monthly EMI but increase the total interest you pay. For instance, a ₹10 lakh loan at 9% over 10 years leads to ₹5.9 lakh in interest.

Many loans also carry prepayment penalties, typically between 2% and 5% of the outstanding balance, which discourages early closure.

For loans in foreign currencies, like education loans in USD, currency fluctuations matter. If the rupee weakens, your EMIs increase. For example, at ₹87/USD in 2025, EMIs may rise by 16% compared to 2022 rates.

How to Manage EMIs Effectively

Choose floating interest rates if possible. With the RBI expected to reduce repo rates in 2025, you could save around ₹800–₹1,000 per month on a ₹50 lakh loan.

Use online EMI calculators to simulate payments, especially if you are planning partial prepayments or moratoriums.

Whenever possible, aim for shorter loan tenures. A ₹20 lakh loan at 9% over 5 years saves about ₹4.2 lakh in interest compared to a 10-year tenure.

Don’t forget tax benefits. Home loan EMIs qualify for deductions under Section 24(b) (up to ₹2 lakh on interest) and Section 80C (up to ₹1.5 lakh on principal).

Most importantly, never miss an EMI. A single default can lower your credit score by 50–100 points and attract penalties of around 2% per month on the overdue amount.

Final Thoughts

EMIs are essential for making large purchases manageable, but they work best with proper planning. By managing tenures, tracking interest rates, and staying disciplined with repayments, you can reduce costs and maintain long-term financial stability while enjoying the benefits of credit.

Start your journey towards financial well-being

Your first financial plan is FREE.Download the app and schedule a meeting with us now!

Download the app

4.7

Average app rating

Start your journey towards financial well-being

Your first financial plan is FREE. Download the app and schedule a meeting with us now!