If you’ve ever explored the world of investing, you’ve likely encountered the terms asset allocation and diversification. Though often used interchangeably, they represent distinct strategies that are fundamental to building a resilient investment portfolio. Asset allocation involves spreading investments across different asset classes—such as equities, debt, and real estate—while diversification refers to distributing investments within a single asset class to reduce specific risks. In this article, we’ll clearly define both concepts, examine their differences, and explain why understanding them is essential for navigating market volatility.

What is asset allocation?

Asset allocation is basically deciding how to divide your investment portfolio across broad asset classes such as equity, debt, gold, real estate, and alternatives—based on your financial personality, milestones, and investment horizon.

Asset allocation is important because it sets the foundation for your portfolio’s risk and return profile. It aligns your investments with your life stage and milestones like buying a house in five years or retiring comfortably in 20.

Let’s understand this with an example: a 30-year-old salaried professional aiming for long-term investment might allocate 60% to equity, 25% to debt, 10% to gold, and 5% to real estate. A retiree, on the other hand, might prefer 20% equity, 60% debt, and 20% gold to prioritize stability.

Read more about Asset Allocation : What is asset allocation? Understanding its meaning, importance, advantages, and disadvantages

What is diversification?

Diversification is taking one step ahead of asset allocation. What I mean by this is if asset allocation is diversifying across asset classes such as equity, debts, gold, real estate, diversification is diversifying within asset classes. In simple words, diversifying ensures

you don’t put all your money into a single stock, bond, or property, reducing the impact of a poor performer.

Let’s understand with this example, when you allocate your investments into equity, you might invest in a mix of large-cap, mid-cap, and small-cap mutual funds or stocks across sectors like IT, banking, and healthcare. In debt, you could diversify across fixed deposits (FDs), Public Provident Fund (PPF), and corporate bonds.

This is important because If you put all your money in one company’s shares and it fails, you could lose a lot. But if you spread it across many companies, one failure won’t hurt as much.

Here’s a simple table to help you understand difference between asset allocation and diversification

| Aspect | Asset Allocation | Diversification |

| Definition | Deciding the percentage of your portfolio for each asset class. | Spreading investments within an asset class. |

| Purpose | Balances risk and return based on goals and risk appetite. | Reduces risk by avoiding overexposure to a single investment. |

| Example | 50% equity, 30% debt, 10% gold, 10% real estate. | Within equity: 20% large-cap, 20% mid-cap, 10% small-cap funds. |

| Scope | Macro-level strategy across asset classes. | Micro-level strategy within an asset class. |

| Timeframe | Long-term, revisited annually or with life changes. | Ongoing, adjusted based on market conditions. |

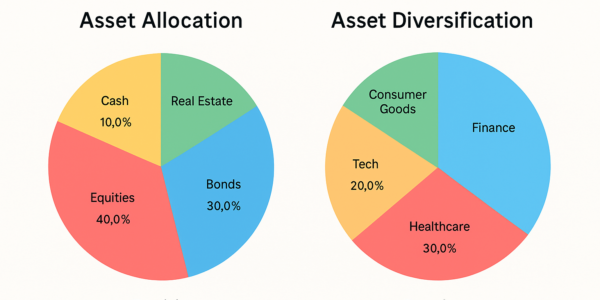

A pie diagram to help you understand better:

Why are asset allocation and diversification important?

Asset allocation and diversification are like the engine and wheels of your investment vehicle; both are essential to reach your financial wellbeing.

In 2025, when the world faced economic uncertainties such as global trade tensions and the RBI’s cautious monetary policy, strategic allocation set your risk-return balance, while diversification ensured that no single investment sank your portfolio.

Before starting, it is very important you define your financial milestones to allocate wisely. Financial advisors also emphasise that your asset allocation should be based on your age and life stages. They also recommend diversifying smartly and reviewing the allocation often.

It is also very important that you consult a qualified financial advisor to plan your investments along with your overall finances.