The journey of cultivating, multiplying and accumulating wealth unfolds over several generations, and while it’s certainly not linear at all times, it is always ongoing. At 1 Finance, we’ve been fortunate to come from decades of observing wealth creation in India — it’s helped us develop a deep understanding of personal finance that informs our advisory services. We’ve seen that financial freedom depends, at least in part, on what we inherit and how we build upon it. In India, our social and domestic fabrics place value and virtue in earning and saving for the purpose of safeguarding the future of the next generation. People also typically attain financial independence at a later age than is the norm in the West. We’ve also noticed that with each passing generation, financial traits, needs and goals evolve. It’s highly relevant then that financial planning and investment strategies also align with these changing ambitions.

Like what you're reading?

Get our latest, straight to your inbox.

Traditionally, personal finance advice draws on limited insights into a person’s financial status and follows a rigid bucketing of risk appetites, not accounting for behavioural quirks and psychological characteristics that shape choices, or the upbringing and family background that inform attitudes towards money. For us, taking these factors into consideration is paramount — it gives us a clearer picture of the individual’s financial standing, helps us figure out how protected or vulnerable they may be with respect to their financial security, and allows us to measure how flexible they can afford to be in terms of experimenting with financial products.

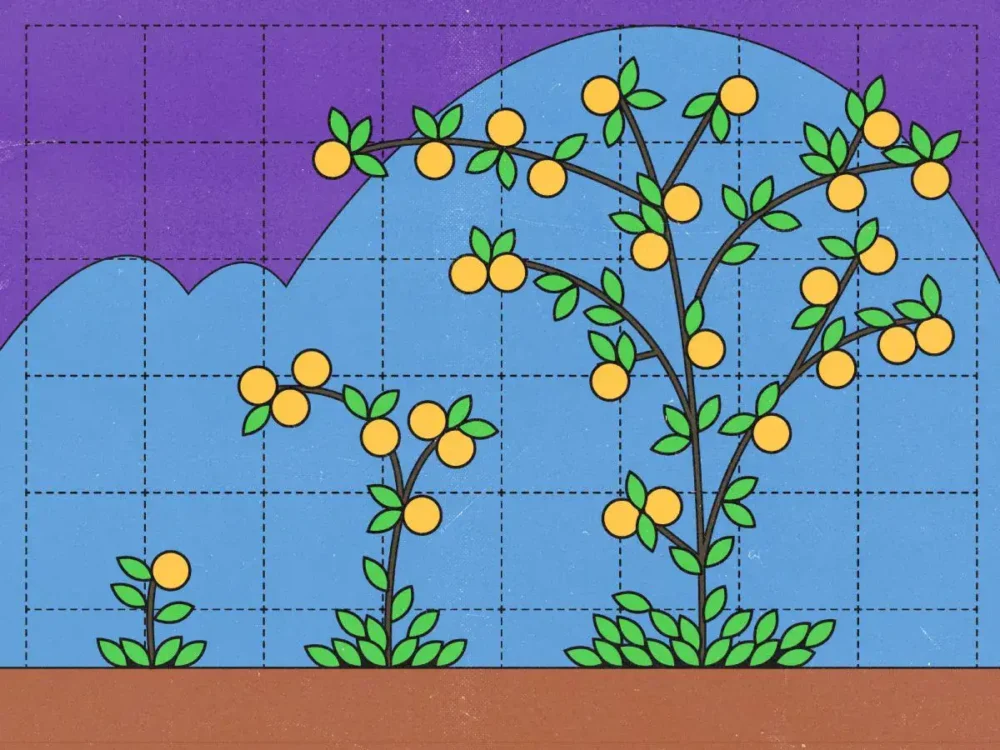

With that in mind, we set out to develop certain markers that would help us ascertain what stage of wealth creation a person may be at. We found that, at any given point in life, regardless of age, people largely fall under one of three phases — or ‘generations’ — of wealth creation.

Generation one comprises unskilled, under-educated people, who may be the sole breadwinners for their family, keen to provide a sense of financial security to their family and a good education to their children. Consequently, generation two includes qualified professionals, working towards attaining financial freedom and affording a decent lifestyle for their family. They may be mindful of their savings, conservative in their approach to investments, keen to buy a home or a car, and intentional about building a nest egg for their kids. Generation three, with a stable financial backing and no liabilities, may more easily be able to follow their passions, have entrepreneurial ambitions, spend on luxuries, and so on. They would have a high appetite for risk, an interest in multiplying their wealth, and curiosity about new, high return–generating asset classes.

These generations also reflect in investment choices. For those only beginning to accumulate wealth, low-risk, reliable investments like savings accounts, government bonds or life insurance are most preferred. Those further on their journey may be open to riskier assets like mutual funds, bank deposits, home loans, credit cards, equity, etc. And those who have an inheritance to fall back on may be comfortable venturing into alternative investment options — think crypto, international stocks, art, NFTs, and the like.

This spectrum is bound to have exceptions — people who are financially proficient may move from one generation to the next within the same lifetime, others may run into significant issues that may set them back financially, and some could be so risk-averse that they do not progress to the next generation. There may also be complications in financial behaviour that arise from psychological and cognitive pitfalls that people across generations are likely to encounter — like a first-generation wealth creator severely lacking curiosity and being far too cautious about maintaining the status quo, or a third-generation investor lacking self-control or displaying overconfidence while making investing decisions.

Even with this sense of framework in place, at the end of the day, it’s highly dependent on the individual in focus. Everyone has a different starting point in the journey to financial well-being, but the broad aim of the pursuit for wealth is common — to achieve a state of satisfaction and security with money within our lifetime, and for some, to offer a head start to the generations that follow. This is why we carefully tailor our advice to each person. Knowing which generation an individual belongs to helps us understand what financial well-being would look like for them, and how far they may be from attaining it. Plus, it brings in deeper insights that we use for refining and moulding our recommendations to their financial disposition.