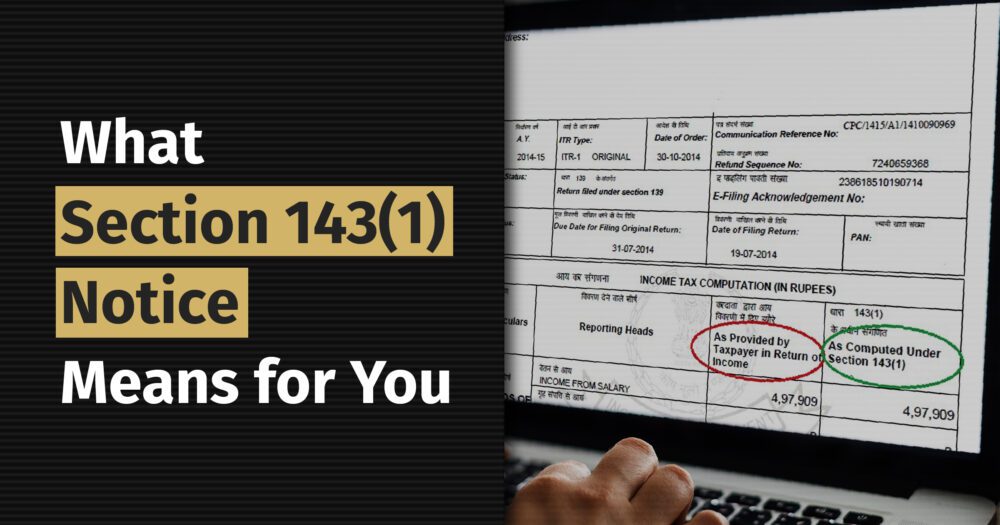

Received a Notice under Section 143(1)? Here’s what it means

Receiving a notice under Section 143(1) is a routine part of the income tax return pr...

When it comes to managing personal finances, understanding the intricacies of taxation is crucial. One area that often poses challenges for individuals is the calculation of capital gains tax. In India, capital gains tax is levied on the profits earned from the sale of capital assets. In this blog, we will delve into the nitty-gritty of capital gains tax calculation in India, providing a step-by-step guide along with practical examples to help you navigate this complex terrain and make informed financial decisions.

Before we dive into tax calculations, let’s clarify what constitutes a capital asset. In India, capital assets include real estate, stocks, bonds, mutual funds, jewelry, and other tangible and intangible assets held for investment purposes. However, following are excluded from the definition of capital assets as per Income tax act;

Any stock in trade ex. A car might be a capital asset for a normal taxpayer. However, the same will not be considered as a capital asset for a car dealer.

Personal assets except archaeological collections, drawings, paintings, sculptures or any work of art.

Rural Agricultural Land

Specified Gold or special bearer bonds notified by the government

Capital gains in India are classified into two types: short-term capital gains (STCG) and long-term capital gains (LTCG). The classification is based on the holding period of the asset and varies for certain assets. Below table specifies the holding period for specified assets to decide if the capital gains would be short term. In case it is held for more than the specified period, it will be considered as Long Term Capital gain and will be taxed accordingly.

| Asset | Considered short term if held for less than |

|---|---|

|

12 Months |

|

24 Months |

| Any other Capital Asset | 36 Months |

In case any of the above capital assets are held for (sold after) the period mentioned against respective assets, it will be considered as Long Term Capital Gain (LTCG).

| Particulars | Amount |

|---|---|

| Full value of Consideration (Sale Value) | XX |

| Less : Expenses incurred on sale | (xx) |

| Net Value of Consideration | XX |

| Less: Cost of Acquisition (*Indexed cost of acquisition in case of Long term capital gains) – Purchase cost | (xx) |

| Less: Cost of Improvement (*Indexed cost of improvement in case of Long term capital gains) – Major repair/ renovation cost | (xx) |

| Short/ Long Term Capital Gains | XX |

| Less: Exemptions (if any) | (xx) |

| Net Taxable Capital Gain | XX |

Indexation is a method used in Indian taxation to adjust the cost of acquisition of an asset for the effects of inflation. It is primarily applicable to the calculation of long-term capital gains tax on assets such as real estate, bonds, non-equity shares, and debt mutual funds.

The purpose of indexation is to ensure that the tax liability on long-term capital gains is fair and accounts for the impact of inflation on the value of the asset over the holding period. By adjusting the cost of acquisition for inflation, the taxable gain is reduced, resulting in a lower tax liability.

The Cost Inflation Index (CII) is used to determine the indexed cost of acquisition. The Central Board of Direct Taxes (CBDT) releases the CII figures each year, and they are applicable from the financial year in which they are notified.

The formula for calculating the indexed cost of acquisition is as follows:

Indexed Cost of Acquisition = (Cost of Acquisition) x (CII of the Year of Sale) / (CII of the Year of Purchase)

Here, the Cost of Acquisition refers to the original cost at which the asset was acquired, while the CII figures represent the cost inflation index for the year of sale and the year of purchase, respectively.

By multiplying the cost of acquisition by the ratio of the CII figures, the indexed cost of acquisition is obtained. This adjusted value reflects the impact of inflation and allows for a fair assessment of the actual gain on the asset during the holding period. You can refer to CII figures on the income tax website on this link

Tax rates applicable on Long term and Short term capital gains differ for certain capital assets.

On sale of Listed Equity shares where STT (Securities Transaction Tax) is paid or a transaction undertaken in foreign currency on a recognized stock exchange located in IFSC (International Financial Services Center) – 15%

Other assets where Short Term Capital Gain is earned – Added to income and chargeable at normal rate of Tax

The above tax rates are mentioned under section 111A of the Income Tax Act, 1961

On sale of Listed equity shares and units of equity oriented funds or a transaction undertaken in foreign currency on a recognized stock exchange located in IFSC (International Financial Services Center) – 10% on gains above Rs. 1,00,000/-

Unlisted shares of a closely held company – 20% with indexation

Listed securities or a zero coupon bond – 10% without indexation or 20% with indexation benefit

Other Long term capital gains – 20%

The above tax rates are mentioned under section 112 and 112A of the Income Tax Act, 1961

There are certain exemptions available on taxation of capital gains. Here are some key exemptions:

Exemption under Section 54: If you sell a residential property and reinvest the proceeds in another residential property within a specified time frame, you can claim an exemption on the Long term capital gains made from the sale. The exemption is available under Section 54 of the Income Tax Act.

Exemption under Section 54F: Similar to Section 54, Section 54F provides an exemption on long term capital gains arising from the sale of any asset other than a residential property. If you utilize the proceeds from the sale to purchase a residential property within the specified time frame, you can claim this exemption.

Exemption under Section 54EC: Under Section 54EC, if you invest the capital gains from the sale of a long-term capital asset in specified bonds issued by the National Highways Authority of India (NHAI) or the Rural Electrification Corporation (REC), you can claim an exemption on the capital gains. The investment must be made within six months from the date of sale.

Exemption under Section 54B: Under Section 54B, if you invest the capital gains from the sale of Urban Agricultural Land in rural/ urban agricultural land, you can claim an exemption on the capital gains. The investment must be made within two years from the date of sale.

It’s important to note that each exemption has its own set of conditions and limitations. It is advisable to consult a qualified tax professional or refer to the latest tax regulations for accurate and up-to-date information regarding exemptions on capital gains in India.

Let us consider an example of a transaction which you might be coming across in your financial journey.

Mr. A sold a flat on 25th December, 2022 for Rs. 1,00,000/- (One crore only) and paid a brokerage of 1%. He had purchased this flat on 30th April, 2015 for Rs. 50,00,000/- (Fifty Lakhs only). Tax payable by him on this transaction will be calculated as follows

Firstly, classification is required if the gains made by Mr. A would be Short Term or Long Term Capital Gain. As this is an immovable property, the period of holding (period for which asset was held by Mr. A) for determining if the asset is short or long term would be 24 months. He held the flat for more than 7 years, hence it will be considered as Long Term Capital Gain and the calculation of the capital gain is as follows;

| Particulars | Amount (in Rs.) |

|---|---|

| Sale value | 1,00,00,000/- |

| Less: Expenses on sale (Brokerage in this case) | 1,00,000/- |

| Net sales value | 99,00,000/- |

| Less: Indexed Cost of Acquisition 50,00,000 x 331/ 254 (CIIs of respective FYs of Sales and purchase of Asset)) | 65,15,748/- |

| Long Term Capital Gain (LTCG) | 33,84,252/- |

| Tax Payable on LTCG @ 20% | 6,76,850/- |

Had Mr. A used the amount received from sale of this flat to purchase another house property, he could have availed exemption u/s 54 and the Capital Gain would have reduced accordingly.

Also, had Mr. A purchased this flat on 30th April, 2021. His holding period would have been less than 24 months and the gain would have been considered as Short Term Capital Gain. It would have been as follows

| Particulars | Amount (in Rs.) |

|---|---|

| Sale value | 1,00,00,000/- |

| Less: Expenses on sale (Brokerage in this case) | 1,00,000/- |

| Net sales value | 99,00,000/- |

| Less: Cost of Acquisition | 50,00,000/- |

| Short Term Capital Gain (STCG) | 49,00,000/- |

| Tax Payable on STCG | Added in total income and charged as per slab |

Let us briefly go through some more examples.

Suppose Mr. B bought 100 shares of a company at Rs. 500 per share, and within a year, he sold them at Rs. 700 per share. The capital gain will be calculated as (700 – 500) * 100 = Rs. 20,000 and tax would be payable @ 15% on these gains.

If these shares were held for more than 12 months, the gain would have been considered as long-term capital gains (LTCG). LTCG on listed stocks is taxed at a flat rate of 10% if the gains exceed Rs. 1 lakh.

Let’s assume Mr. C purchased 100 grams of gold jewelry for Rs. 3 lakhs and sold it after two years for Rs. 4 lakhs. The capital gain will be (4 lakhs – 3 lakhs) = Rs. 1 lakh. If the gold is held for more than 36 months, it will be considered as long-term capital gains. Here, as the gold is held for less than 3 years, this will be considered as short term capital gain and will be added to income of Mr. C.

In case, a taxpayer has incurred loss on sale of capital asset, he can set off the same against gains made on sale of another capital asset. However the treatment for short term capital loss and long term capital loss is different.

STCL can be set off against both short-term capital gains (STCG) and long-term capital gains (LTCG) in the same financial year. For example, if you have incurred a loss by selling stocks within a year, you can set off the loss against any short-term or long-term gains made on other investments during that financial year.

LTCL can be set off against long-term capital gains (LTCG) only in the same financial year. Similar to STCL, if you have incurred a loss on the sale of a long-term asset like property, you can offset it against any long-term gains made during that financial year.

In case, the losses cannot be set-off as mentioned above, the same can be carried forward and set off against the gains in the next financial year. In case it is not set off even in the next year, it can be carried forward for upto 8 years starting from the year in which it occurred. However, timely filing of ITR is necessary to claim such carry forward of losses.

Disclaimer: Please note that the above tax slabs are indicative and may be subject to change. The information provided is based on research and personal opinion. It is advised to consult a tax advisor or a certified financial advisor for accurate advice tailored to your individual situations.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Receiving a notice under Section 143(1) is a routine part of the income tax return pr...

Receiving a notice from the income tax authorities can naturally cause anxiety, espec...

Taxpayers have multiple options to file their taxes, such as through paper returns or...