Popular searches

Product scoring may vary based on gender, age, policy tenure and sum assured.

The lowest age in the selected range is considered for price evaluation (e.g., 25 - 29)

Best NPS Fund Manager

Compare and find out the best NPS fund manager using our scoring and ranking model.

Featured List

Analysis was last updated in .

What is 1 Finance Score?

The 1 Finance Score involves a thorough evaluation and comprehensive analysis of various key parameters to assess all equity, corporate debt, and government securities under NPS schemes in India, with a maximum track record of over ten years. record of over ten years. This approach enables you to choose an NPS scheme that aligns with your preferences, ensuring your decision is backed by extensive research and unbiased analysis.

Each fund is assigned a score on a scale from 1 to 100 based on the evaluation of all relevant factors. Here’s an overview of our scoring system:

- High (75 – 100)Top NPS with strong risk-adjusted returns and YTM, low costs, long history, portfolios with good quality & well diversified, low volatility, and strong track record.

- Medium (50 – 75)NPS with average risk-adjusted returns and YTM, moderate costs, a reasonable track record, slight volatility, and fair quality and diversification.

- Low (1 – 50)NPS with poor risk-adjusted returns, high costs, limited track record, low YTM, poor quality/diversification, high volatility, and inconsistent returns.

- The model begins with a comprehensive analysis of 106 NPS schemes, focusing specifically on NPS Tier 1 Scheme E, Scheme C, and Scheme G. These schemes have been selected due to their high subscriber base and widespread adoption.

- We have identified essential factors affecting NPS performance. These unbiased inputs help subscribers choose the right scheme.

- We have structured and Organised data for accurate analysis.

- Each parameter was assigned a numerical value based on both quantitative and qualitative factors.

- After evaluating all parameters, we have derived a single 1F Score and 1F Rank for each NPS scheme, making decision-making simpler.

- We quarterly update our scoring model to reflect any changes in the schemes, ensuring users always get the latest information.

The National Pension System is regulated by Pension Fund Regulatory and Development Authority (PFRDA) . It is often regarded as one of the best options for retirement planning because it is flexible and portable, giving you the freedom to save at your own pace.

The National Pension System can be a smart way to enhance retirement income while enjoying tax benefits. Selecting the best NPS fund manager is crucial to align with your retirement goals and risk tolerance.

- The NPS Tier 1 account is primarily aimed at building a retirement corpus. It has restrictions on withdrawals to ensure disciplined savings over the long term.

- Only under specific conditions, you can withdraw a portion of your savings before retirement.

- Contributions to NPS Tier 1 accounts are eligible for tax deductions:

a. Section 80C: Up to ₹1.5 lakh as part of the overall 80C limit.

b. Section 80CCD(1B): An additional ₹50,000 over and above the 80C limit, making it a total tax benefit of up to ₹2 lakh per financial year. - At retirement, up to 80% of the corpus can be withdrawn as a lump sum, of which 60% of the corpus is tax-free and 20% is taxable under the income tax slab of the subscriber and the rest 20% is annuity, which is also taxable.

- Tax benefits for NPS Vatsalya

- Minimum contribution at the time of opening: ₹500.

- Minimum annual contribution: ₹1,000 (may vary with updates).

- Allows you to save systematically even with modest contributions.

- You have two options for managing your investments:

a. Active Choice: You decide how much to invest in equities (E), corporate debt (C), and government securities (G) based on your preferences.

b. Auto Choice: A smart option where your investments are automatically adjusted based on your age. It starts with higher equity exposure when you're younger and shifts to safer investments as you get closer to retirement. - Equity investments are capped at 75%, ensuring a good balance between growth potential and risk.

- You can withdraw 80% of the total corpus as a lump sum if the NPS corpus is over ₹12 lakh. The remaining 20% must be used to purchase an annuity.

- If the NPS corpus falls between ₹8 lakh and ₹12 lakh, you can withdraw up to ₹6 lakh as a lumpsum and opt for Systematic Unit Redemption(SUR) for the remaining balance over a minimum span of six years.

- If the NPS corpus is up to ₹8 lakh, you can withdraw the entire amount at once or SLW or SUR.

It is designed primarily for individuals who are not covered under government or corporate NPS models (self-employed individuals, professionals, freelancers, etc.). Subscribers can choose their pension fund manager and asset allocation (Equity, Corporate Debt, Government Securities), with flexibility under common schemes.

Under this model:

- Both the employer and the employee can contribute.

- Employer contributions qualify for tax benefits under Section 80CCD(2).

- It offers portability (employees can retain the same PRAN when changing jobs).

- It includes a mandatory Tier I account and an optional Tier II account.

A subscriber can maintain multiple PRANs (Permanent Retirement Account Numbers) and can also open multiple Tier I and Tier II accounts, even across different Pension Funds and schemes. This allows the investor to diversify investments, choose different asset allocations, and align each account with specific financial or retirement goals.

The MSF provides greater control over investment decisions, enabling subscribers to select schemes based on their risk appetite, return expectations, and fund performance. Importantly, under MSF, subscribers can now opt for up to 100% equity exposure, offering higher growth potential for long-term retirement planning.

Key Features of NPS Tier 1 Account

- Contributions to NPS Tier 1 accounts are eligible for tax deductions:

- Section 80C: Up to ₹1.5 lakh as part of the overall 80C limit.

- Section 80CCD(1B): An additional ₹50,000 over and above the 80C limit, making it a total tax benefit of up to ₹2 lakh per financial year.

- At retirement, up to 80% of the corpus can be withdrawn as a lump sum, of which up to 60% of the corpus is tax-free and 20% is taxed under the subscriber's income tax slab. (Non-government subscribers (including the All-Citizen model))

- Your funds stay locked until you complete 15 years from the date of joining or reach 60 years of age (whichever is earlier).

- Early withdrawals are allowed only under specific conditions.

- Subscribers can take out a loan against their NPS balance.

- You can withdraw only under specific purposes like:

- Higher education.

- Marriage expenses.

- Purchase or construction of a house (only once during the tenure).

- Medical emergencies for self or family, including spouse/children/parents.

- At the age of 60 (retirement age):

- 80% of the corpus can be withdrawn as a lump sum, of which up to 60% of the corpus is tax-free and 20% is taxed under the subscriber’s income tax slab, (Non-government subscribers (including the All Citizen model))

- The remaining 20% must be used to purchase an annuity, which provides a regular pension post-retirement.

- Subscribers can defer withdrawals or annuity purchases until the age of 85 years.

Conditions for Premature Exit from NPS Tier 1 Account

- Premature exit is allowed before 60 years, but only 20% of the corpus can be withdrawn as a lump sum. The remaining 80% must be used to purchase an annuity.

- Under the All-Citizen Model & Corporate Sector (CS & MSF) for a corpus less than ₹5 lakh, 100% lump sum or SLW or SUR or up to 20% and at least 80% annuity. For corpus over ₹5 lakh, up to 20% lump sum and at least 80% annuity.

- The minimum lock-in period for the Non-Government Sector All-Citizen model (Common Scheme and MSF) has been removed before 60 years or from 15 years from the date of subscription. (Whichever is earlier).

- If there is any exit due to the death of the subscriber, then under the All-Citizen Model & Corporate Sector (CS & MSF), 100% lumpsum option for annuity is available, if desired. (Remains the same). Additionally, SLW or SUR is available as an option.

Who Should Opt for a NPS Tier 1 Account?

- Individuals looking for a disciplined, long-term retirement savings plan.

- Salaried and self-employed individuals seeking tax-efficient investments.

- Those wanting a low-cost investment option with flexibility in contribution amounts.

Key Features of NPS Tier 2 Account

- NPS Tier 2 is an add-on account available only to subscribers of the NPS Tier 1 account.

- It is not mandatory and is entirely optional for those who want additional flexibility with their savings.

- Unlike the NPS Tier 1 account, the NPS Tier 2 account allows you to withdraw your funds anytime without restrictions. This makes it highly liquid and suitable for short-term financial needs.

- There is no lock-in period for the NPS Tier 2 account, except for government employees who wish to avail tax benefits (3-year lock-in applies in such cases).

- For other subscribers, contributions and withdrawals are entirely at their discretion.

- Contributions to NPS Tier 2 accounts do not qualify for tax deductions under Section 80C or any other section.

- Exception: Central government employees can avail of tax benefits under Section 80C for NPS Tier 2 contributions, but only if they opt for a 3-year lock-in.

- NPS Tier 2 accounts are purely optional and are best suited for those who want an additional savings avenue with high liquidity.

Differences Between NPS Tier 1 and NPS Tier 2 Accounts

| Feature | NPS Tier 1 Account | NPS Tier 2 Account |

| Purpose | Long-term retirement savings | Flexible, short-term savings |

| Tax Benefits | Yes (₹2 lakh max under 80C and 80CCD) | No (except for govt employees with 3-year lock-in) |

| Withdrawal | Restricted (only under specific conditions) | Unlimited and anytime |

| Lock-In Period | All Citizen Model: Minimum tenure of 15 years. Corporate Model: Investment continues until age 60. | None (except 3 years for govt employees claiming tax benefits) |

| Minimum Contribution | ₹500 (initial); ₹1,000/year | ₹1,000 (initial); no annual requirement |

| Investment Options | Active Choice / Auto Choice | Active Choice / Auto Choice |

Who Should Opt for a NPS Tier 2 Account?

- Individuals looking for a flexible investment option with no restrictions on withdrawals.

- Investors seeking to leverage the benefits of professional fund management for short-term and medium-term goals.

- Those who already have a NPS Tier 1 account and want an additional avenue for savings and investments.

- Central government employees looking for tax benefits (with a 3-year lock-in).

- This option allows investors to decide how their funds are allocated across different asset classes. It is best suited for individuals who actively track markets and want to customise their portfolio based on their risk appetite and return expectations.

- NPS Subscribers who had opted for Scheme A in Tier I (Active Choice) can exercise additional choice of switching their wealth from Scheme A into any other asset classes of their choice without any additional cost till 25th Dec 2025 as per applicable guidelines.

| Feature | Details |

| Investor Control | Full control over asset allocation. |

| Available Asset Classes | Equity (E), Corporate Debt (C), Government Securities (G) |

| Maximum Equity Allocation | NPS Tier 1: Up to 75% NPS Tier 2: Up to 100% |

| Risk Suitability | Suitable for investors seeking higher returns and comfortable with actively managing investments |

* The maximum equity allocation is capped at 75% up to the age of 50, and it gradually reduces by 2.5% each year.

- In Auto Choice, asset allocation is automatically adjusted based on the subscriber's age. As the investor grows older, the portfolio shifts toward safer assets, making it ideal for those who prefer a hands-off approach.

- Types of Auto Choice Investment Options

- NPS offers Four Auto Choice Lifecycle Funds, each designed for different risk levels:

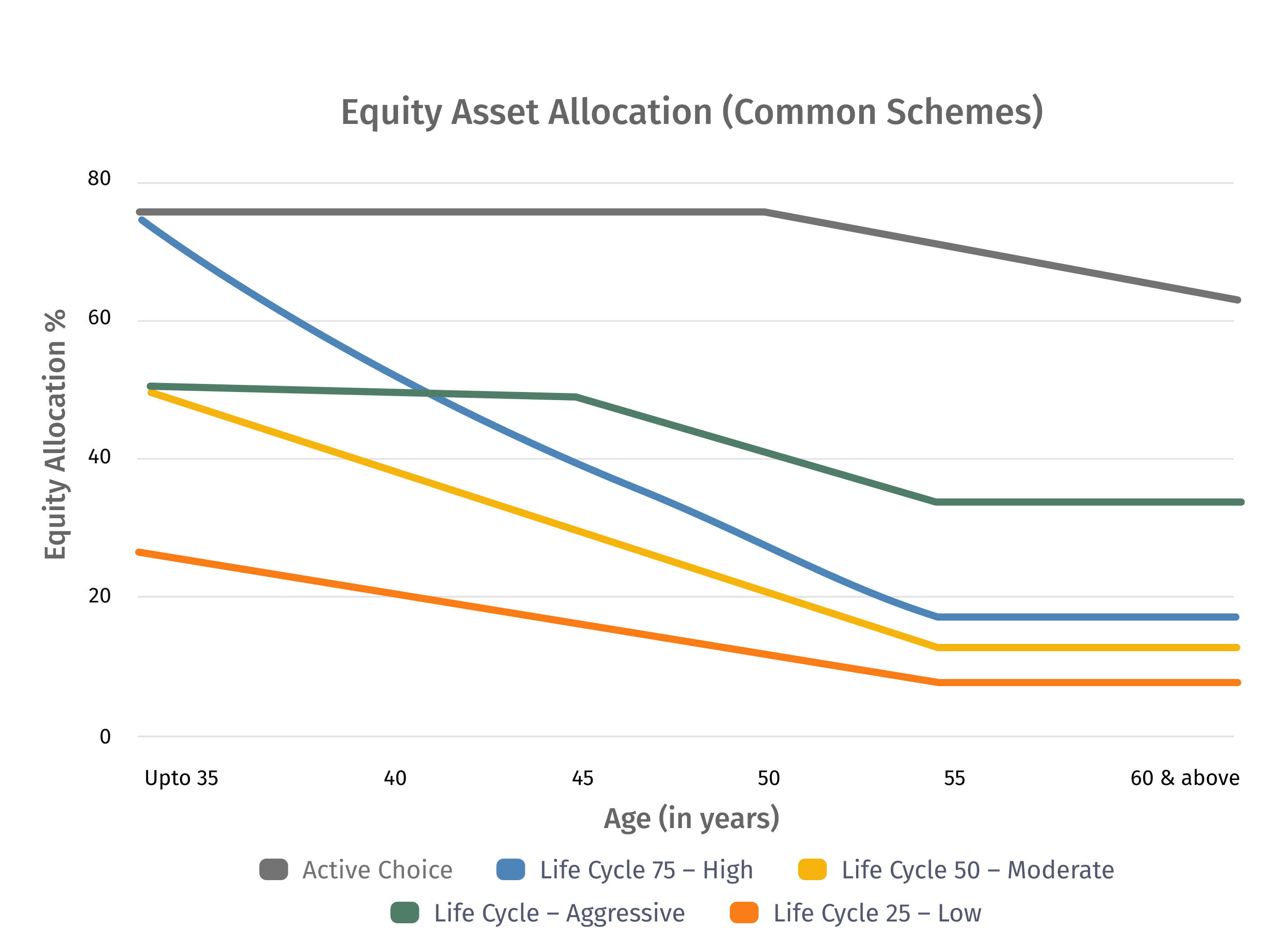

| Previous Names | New Names | Equity allocation (%) | Branding Tagline & Market Positioning |

| LC 25 (Conservative Life Cycle Fund) | Life Cycle 25 – Low (5E / 55 Y) | 25% up to 35 years, falling to 5% at 55+ | “Preserve your savings with steady growth — designed for stability as you near retirement.” |

| LC 50 (Moderate Life Cycle Fund) | Life Cycle 50 – Moderate (10E / 55 Y) | 50% up to 35 years, falling to 10% at 55+ | “Balance growth and protection — a steady path for building and safeguarding retirement wealth.” |

| LC 75 (Aggressive Life Cycle Fund) | Life Cycle 75 – High (15E / 55 Y) | 75% up to 35 years, falling to 15% at 55+ | “Accelerate wealth creation early — harnessing high equity for your retirement goals.” |

| Balanced Life Cycle Fund | Life Cycle – Aggressive (35E / 55 Y) | 50% up to 45 years, falling to 35% at 55+ | “Be aggressive & stay invested longer in growth assets — for a stronger retirement corpus.” |

- If you want full control → Active Choice

- If you prefer automatic adjustments → Auto Choice (Aggressive, High, Moderate, or Low based on risk level)

The Life Cycle 75 – High option begins with the highest equity allocation of around 75% for younger investors and gradually reduces over time. The Life Cycle 50 – Moderate starts with approximately 50% equity, providing a balanced approach between growth and stability. The Life Cycle 25 – Low begins with about 25% equity and is designed for investors seeking lower risk and greater stability.

The Balanced Life Cycle Fund (BLC), however, exhibits a relatively higher equity allocation at key age milestones such as 45 and 55 years when compared to the LC 75 Fund, which is currently categorized as an Aggressive Life Cycle Fund under Auto Choice. This structure allows investors to maintain relatively higher growth exposure during mid-career years while still gradually transitioning toward lower risk assets closer to retirement.

Overall, these life cycle options help investors align their asset allocation with their age, risk appetite, and retirement goals, ensuring a gradual shift from growth-oriented investments to more stable income-generating assets.

- The National Pension System (NPS) provides subscribers with the flexibility to allocate their investments across four distinct asset classes. Each asset class has its own risk-return profile, making it essential for investors to select allocations based on their financial goals and risk appetite.The three asset classes available under NPS include Equity (E), Corporate Debt (C) and Government Securities (G).

- Scheme A has been merged with Schemes C and E. This ensures that NPS contributions are invested in larger, more diversified, and more liquid portfolios, enabling smoother management and more efficient long-term growth.

- Equity investments are considered the most high-risk, high-return asset class in NPS. Asset Class E primarily invests in stocks of listed companies, making it market-linked and volatile, yet offering the highest potential for long-term capital growth.

- This asset class is suitable for investors with a high-risk appetite who are willing to withstand short-term market fluctuations in pursuit of higher returns over time.

- In NPS Tier 1 accounts, the maximum allocation allowed in Equity is 75% (This is applicable for the Common Scheme), whereas in NPS Tier 2 accounts, investors can allocate up to 100% (Common Scheme). This makes it a preferred choice for individuals looking for long-term wealth accumulation.

- Following any changes in the NIFTY 250 Index, Pension Funds are required to rebalance their portfolios in line with the revised eligible stocks within a period of six months.

- Investment is now permitted in units issued by Gold and Silver ETFs regulated by SEBI.

- However, the aggregate investment units of REITs, Equity-Oriented AIFs and Gold & Silver ETFs shall not exceed 5% of the AUM of Scheme / Asset Class E.

- Corporate debt investments offer a balance between risk and returns, making them a moderate-risk, moderate-return asset class.

- Asset Class C includes corporate debt and debentures issued by corporate entities, including banks and public financial institutions, with at least an AA rating. These instruments generate stable interest income while offering some capital appreciation.

- Although corporate debt is less volatile than equity, it is still market-dependent. Investors seeking a balanced portfolio with a mix of growth and stability may find this asset class an ideal choice.

- Government Securities provide the safest investment option within the NPS framework. Asset Class G primarily consists of government securities (G-Secs) and units of mutual funds set up as dedicated funds for investment in government securities. The allocation to mutual funds shall not exceed 5% of the AUM under Scheme G at any point in time.

- This asset class is ideal for conservative investors who prioritise capital protection over aggressive growth. However, one limitation is that returns from government securities are often lower than inflation, which could reduce the purchasing power of savings over time.

- Despite this, Asset Class G remains a preferred choice for individuals nearing retirement or those who prefer stability and security in their investments.

- Any Indian citizen (resident or NRI) aged 18 to 85 can open an NPS account.

- Citizens of INDIA, Including NRI’s & OCI Card holders.

- Any salaried or individual person can open an NPS account.

- You can open an NPS account online or offline:

- Online Registration (eNPS Portal or CRA Platforms like NSDL, KFinTech)

- Visit the official eNPS website and select "Join NPS".

- Enter your details (Name, DOB, PAN, Aadhaar, Mobile Number, Email).

- Choose between NPS Tier 1 (mandatory) and NPS Tier 2 (optional) accounts.

- Complete KYC verification via Aadhaar or PAN.

- Upload documents (photo, signature, PAN, bank details).

- Make an initial contribution (minimum ₹500).

- Complete OTP or e-sign verification.

- Receive your Permanent Retirement Account Number (PRAN) via email/SMS.

- Offline Registration (Through PoPs like Banks & Post Offices)

- Visit the nearest PoP (Point of Presence) and collect the NPS form.

- Fill in your details and attach KYC documents (PAN, Aadhaar, Photo).

- Submit the form & make the first deposit (minimum ₹500).

- Receive a PRAN kit with your account details.

- Contribute to NPS Tier 1 or NPS Tier 2 accounts via the eNPS website or at a PoP center.

- The minimum annual contribution is ₹1,000 for NPS Tier 1.

- Choose a Pension Fund Manager (PFM) from options like SBI, HDFC, ICICI, Kotak, LIC, UTI, etc.

- Select your investment strategy:

- Active Choice – You decide how funds are allocated across Equity (E), Corporate Debt (C), and Government Securities(G).

- Auto Choice – The system automatically adjusts your investments based on age.

- Once you contribute, funds are invested and units are credited to your NPS account in T+2 days.

- You can nominate up to 3 people and assign a percentage of your savings to each nominee.

- Track and manage your investments through the NSDL NPS portal.

- Contributions and fund allocation can be adjusted over time.

- NPS subscribers can claim tax deductions under Section 80CCD(1) of the Income Tax Act, 1961.

- The deduction limit is ₹1.5 lakh per year within the overall Section 80C limit.

- An extra deduction of ₹50,000 is available under Section 80CCD(1B) for contributions to NPS Tier 1 NPS accounts.

- This benefit is over and above the ₹1.5 lakh deduction under Section 80C, making the total tax-saving potential ₹2 lakh per year.

- Under the old regime, the contributions made by your employer to NPS are eligible for deductions, capped at 10% (14% for central government employees) of your basic salary plus dearness allowance (if any), with a maximum limit of ₹7.50 lakh under Section 80CCD(2).

- Under the new regime, the contributions made by your employer to NPS are eligible for deductions, capped at 14% of your basic salary plus dearness allowance (if any), with a maximum limit of ₹7.50 lakh under Section 80CCD(2).

- The total deduction for PF, NPS, and superannuation funds combined is capped at ₹7.5 lakh per year.

New purpose added: Settlement of a financial obligation of the subscriber taken from a regulated financial institution against a lien/charge on the NPS account.

Individuals joining NPS after the age of 60 years (All Citizen Model)

- The vesting period is removed.

- The withdrawal limit has changed to up to 80% lump sum, of which 60% is tax-free and 20% is taxable under the income tax slab and at least 20% annuity.

- Another change is that for a corpus of less than ₹12 lakh, 100% lump sum is allowed or SLW or SUR OR up to 80% lump sum and at least 20% annuity.

- Similarly, for a corpus above ₹12 lakh, 80% lump sum and at least 20% annuity is allowed.

- For Premature Exit: The vesting period has been removed.

- For Exit due to Death: 100% lumpsum permitted; Option for annuity, if desired. (Remains the same). Additionally, an option for availing SLW or SUR is available.

1 Finance Private Limited operates independently. The information presented in the scoring and ranking model is solely for educational and informational purposes and should not be construed as financial advice. Before making any financial decisions, it's essential to undertake your own thorough research and analysis. If you're uncertain about any financial matters, we strongly recommend seeking guidance from a qualified financial advisor.