1 Finance Magazine

Featured Articles

View moreComprehensive stories to keep you updated about personal finance developments

Are You Paying an Advance for Your New Home? Don’t Miss This!

CEO, RARE Enterprises

Missed the Income Tax Return (ITR) Filing Deadline? You Have ITR-U to Fall Back On

CEO, RARE Enterprises

Investing in Cryptocurrencies in 2024

CEO, RARE EnterprisesInterviews

View moreConversations with industry stalwarts to give you differentiated insights

Nikhil Varghese

CEO, RARE Enterprises

Deepika Narayan Bharadwaj

CEO, RARE Enterprises

Ritesh Srivastava

CEO, RARE EnterprisesPrimary Research

View moreGet insights based on first-hand surveys and research

The Impact of Divorce on Finances in India

CEO, RARE Enterprises

The Mis-Selling Menace

CEO, RARE Enterprises

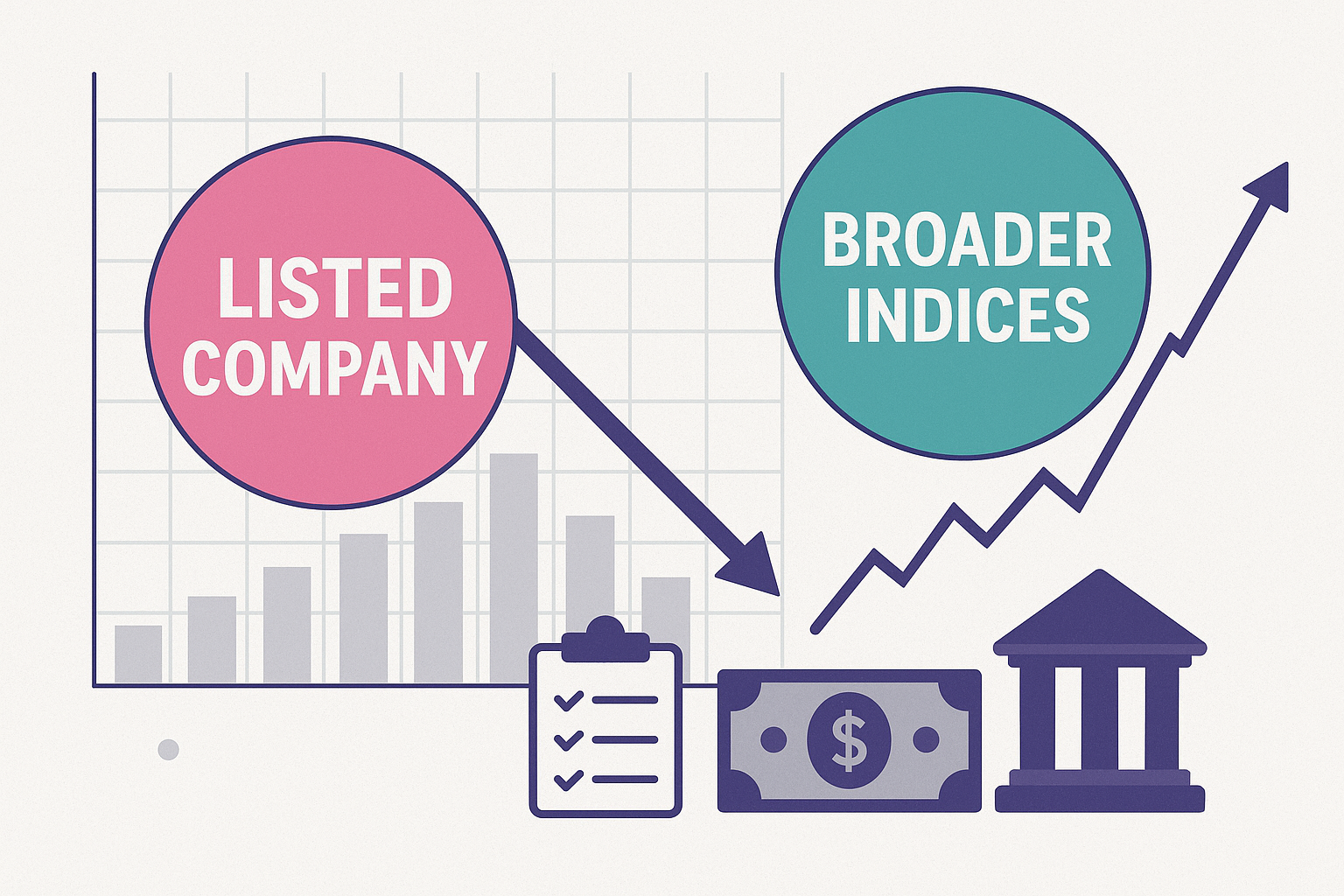

Companies That List Do Not Even Beat The Broad Indices

CEO, RARE EnterprisesJoin The Waitlist

Fill in your details to subscribe to the magazine

Thank you!

We will update you on mail.

Back

Frequently Asked Questions

The magazine is published quarterly.

1 Finance Magazine serves as a research handbook and knowledge repository for qualified financial advisors. By providing comprehensive, bias-free research across financial products, the magazine helps advisors make better choices for their clients. It also aids in effectively communicating the rationale behind these choices, enhancing client trust and satisfaction.

1 Finance Magazine offers in-depth coverage of financial topics and products. Our content includes research and analysis on investments, liabilities, insurance, mutual funds, real estate, arts and antiques and other financial product categories.

We aim to provide a comprehensive resource for financial advisors to make informed decisions and effectively communicate with their clients.

1 Finance Magazine is India’s only ads-free and bias-free print magazine dedicated to empowering financial research. Unlike other financial publications, the magazine provides a holistic view of personal finance through primary research, tailored specifically for qualified financial advisors. We cover all aspects of personal finance, including investment, liability, insurance and more, ensuring our content is relevant, unbiased and actionable.

The magazine is free from advertisements, ensuring that there is no influence from third parties. Our research is based on primary data, rigorously filtered to suit the needs of financial advisors, enabling them to make well-informed decisions and offer the best advice to their clients.