When you look at equity mutual funds, the first thing that comes to your mind is growth, a way to build wealth in the long run. But then the real question tags along: where should you put your money? Large-caps feel safe with their steady compounding, mid-caps hold the promise of growth, and then there are small-caps, which look tempting with their high-risk but high-reward appeal. Multi-cap funds, one type of equity mutual funds, resolve this issue, by giving you a bit of everything in just one single scheme.

In September 2020, Securities and Exchange Board of India (SEBI), the market regulator in India, brought in a rule that changed entirely the way multi-cap funds are structured with a simple intent. They wanted to ensure genuine diversification in the fund and maintain transparency between the AMCs and investors.

However, in reality, it also brought a fair amount of rigidity. We will be focusing on this aspect and the implications it can have on your strategy. Let’s begin with understanding what are multi-cap funds and the SEBI’s rule in detail.

What are multi-cap funds?

Think of a multi-cap fund as a three-legged stool, where each leg represents large-cap, mid-cap, and small-cap stocks. If one leg (say, small-caps) stumbles, the other two can help steady the portfolio.

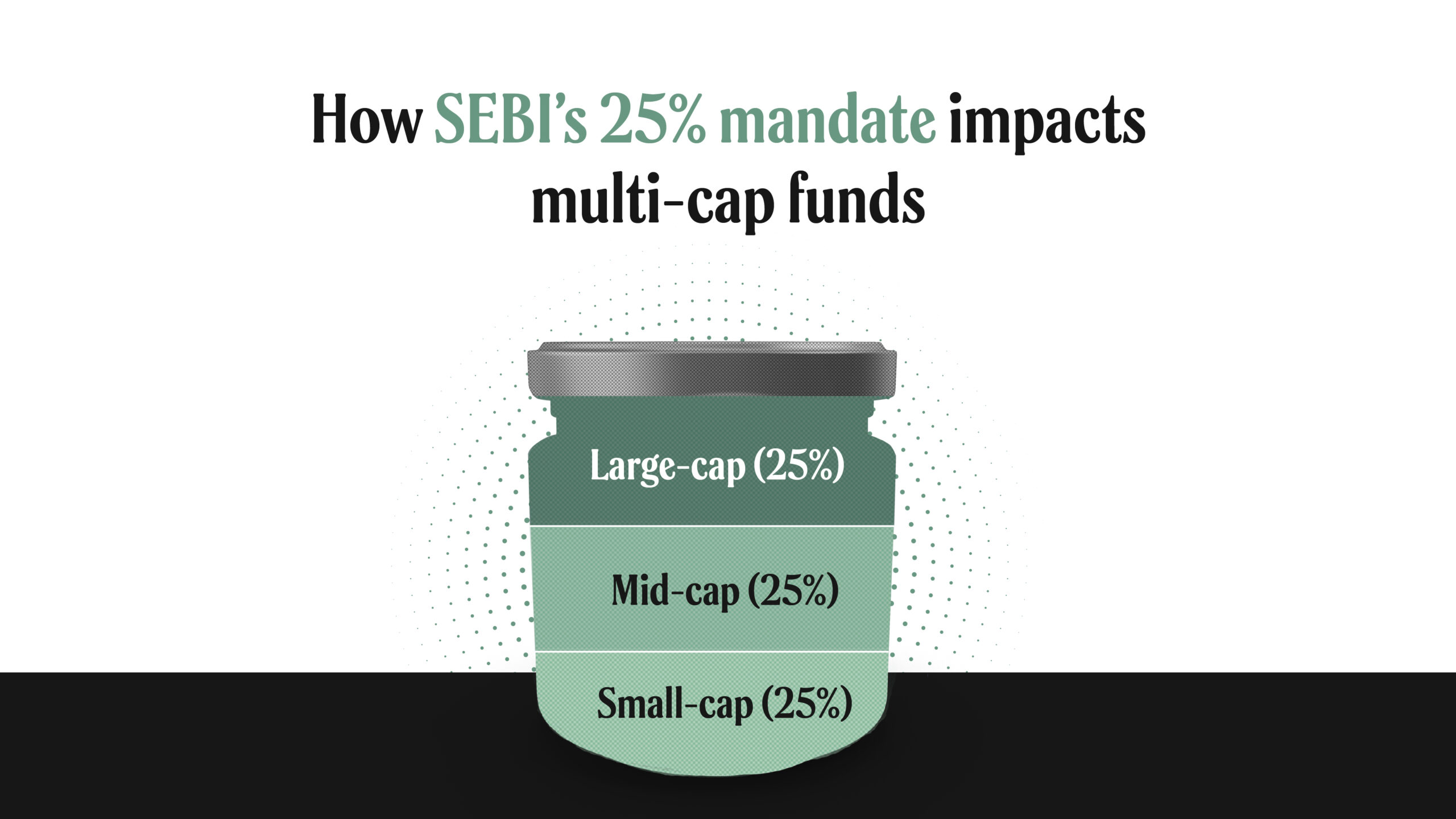

By definition, these funds invest across the market spectrum. According to SEBI, to be classified as a multi-cap fund today:

- At least 75% of the total portfolio allocation must go into equities

- Within this, 25% each must be compulsorily allocated to large, mid, and small-caps

This rule is also reflected in the Nifty500 Multicap 50:25:25 Total Return Index (TRI), which acts as the benchmark for these funds.

Why SEBI introduced the 25% rule for multi-cap funds

SEBI identified the following reasons that necessitated in implementation of this rule:

Many multi-cap funds were benchmarked to indices like NIFTY 200 or NIFTY 500, but in reality, their portfolios were dominated by large-cap stocks (sometimes, more than 80%). In such cases, they should have been closer to NIFTY 50, as this benchmark better represents the top 50 large-cap companies. The NIFTY 200 AND NIFTY 500 have a broader exposure that may also cover mid-cap and small-cap stocks too.

Despite the “multi-cap” label, exposure to mid and small-caps was negligible in several schemes like ICICI Pru Multicap Fund, where its allocation to small-cap companies was less than 10%. This, in a way, lacked true to its label.

A quick look at ICICI Pru Multicap Fund’s allocation over the years shows how dynamics shifted (before and after the rule was implemented).

ICICI Pru Multicap Fund: Average asset allocation (%) for 2019-21

| Year | Large-cap (avg. %) | Mid-cap (avg. %) | Small-cap (avg. %) |

| 2019 | 70.97 | 12.77 | 9.37 |

| 2020 | 68.43 | 16.44 | 9.74 |

| 2021 | 42.80 | 26.17 | 28.58 |

Source: 1 Finance Research

Prior to the rule, the fund tilted heavily toward large-cap stocks, with 70.97% in 2019 and 68.43% in 2020. However, by 2021, the allocation realigned with the new SEBI regulation, with large-cap exposure dropping to 42.80%, while mid-cap and small-cap allocations rose to 26.17% and 28.58%, respectively.

With this 25% rule for multi-cap funds, SEBI also targeted misleading scheme names. At that time, high-profile funds like HDFC Equity Fund or Motilal Oswal Multicap 35 had more than 80% invested in large-caps while marketing themselves as multi-caps. Investors were essentially buying large-cap funds under a different name.

So, SEBI’s intention was clear. They wanted to make sure multi-cap funds remain multi-cap. But here comes the twist you may have overlooked. Diversification is generally good, but a fixed allocation isn’t investor-friendly as it can become a problem when markets turn volatile.

Check out: Curious to know if your mutual fund holdings are truly diversified and don’t overlap across different schemes? Try Mutual Fund Overlap Calculator to find out.

How does this fixed allocation expose multi-cap funds to market risks

Markets are cyclical, with different equity segments outperforming at different times. However, multi-cap funds face structural limitations in adapting to these shifts.

In particular, small-cap and mid-cap stocks tend to be more volatile when the market trends lower during the bearish phase. Despite this, the 25% mandate compels the 50% allocation in these segments, significantly amplifying the downside risks as they cannot reallocate towards relatively stable large-cap stocks.

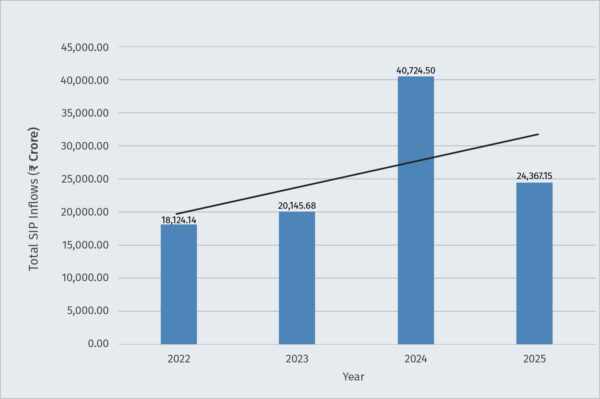

As per 1 Finance research, August 2025 data, total SIP asset under management (AUM) in multi-cap funds stands around ₹205141.4846 Crore, almost 128% increase from August 2023, with the total number of folios reaching 10582438.

The situation is even more critical, as over the last 3-5 years, these funds have seen a steady rise in the retail participation of SIPs. The chart below clearly illustrates this trend, showing how SIP inflows in multi-cap funds have consistently increased year after year, despite market volatility. The year 2025 has already reached almost ₹25,000 Crore mark.

Total SIP inflows (₹ Crore) in multi-cap funds: from years 2022 - 2025

Source: 1 Finance Research

With retail investments continuing to pour into these funds, this rigid allocation requirement may inadvertently be fueling a bubble in the mid-cap and small-cap space. Despite these stocks becoming over-valued, fund managers can do nothing about it.

Multi-cap funds performance review: When broad exposure doesn’t mean lower risk

Drawdowns reveal the real pain investors experience during a market downturn, and how long it takes to recover. While traditional metrics like standard deviation focuses on volatility, they don’t clearly convey the depth of loss and time of recovery. An analysis of HDFC Multi Cap Fund, Kotak Multi Cap Fund, and SBI Multi Cap Fund highlights this point clearly.

Key metrics to understand

- Drawdown: measures the percentage decline in the investment from its highest value to its lowest over a specific period

- Net Asset Value (NAV): the price of the one unit of a fund

The table presents the drawdown figures for their corresponding dates, along with the time taken to recover from its value lowest.

Multi-cap funds: Drawdown and recovery data

| Fund name | Period considered | Maximum Drawdown | Peak to Final Recovery Date | Days of recovery |

|---|---|---|---|---|

| Quant Multi Cap Fund | 27-09-2024 to 03-03-2025 | -24.71% | Not recovered | Uptill now not recovered |

| Kotak Multi Cap Fund | 27-09-2024 to 03-03-2025 | -21.00% | Not recovered | Uptill now not recovered |

| HDFC Multi Cap Fund | 27-09-2024 to 03-03-2025 | -20.20% | Not recovered | Uptill now not recovered |

| SBI Multi Cap Fund | 27-09-2024 to 28-02-2025 | -14.74% | 30-06-2025 | 276 |

Source: 1 Finance Research

1 Finance research makes this clear.

- From September 2024, all major funds experienced steep double-digit drawdowns, despite being positioned as diversified.

- What’s more striking is that both funds, HDFC Multi Cap Fund and Kotak Multi Cap Fund, still haven’t clawed back to their earliest highs, even after months. Investors remain in the red.

- Only SBI Multi Cap Fund managed to recover, and even that took nearly nine months (276 days), just to recover losses.

This evidence challenges the assumption that all in one fund style alone ensures stability during market shocks. So, while SEBI’s rule spreads risk, it also forces the portfolio to become vulnerable to market volatility, especially from mid-caps and small-caps. And neither fund managers nor investors can do much if the conditions worsen.

How the 25% rule restricts fund managers' flexibility

Fund managers’ expertise lies in spotting opportunities, rebalancing risk, and shifting allocations based on market cycles. They are also responsible for selecting valuable stocks. However, multi-cap funds have a paradoxical case. Being marketed as actively managed funds that require complete fund managers’ supervision, instead, this rule ties their hands, not allowing them the flexibility to take calls.

So, you aren’t getting the best of both worlds. You are paying the active management fees, yet not able to use it optimally. In such cases, it is arguably better not to have an active fund manager at all, rather than have one who cannot exercise judgment when it is needed the most.

Considering these strategic limitations, naturally, this brings us to an important aspect investors should consider, which is taxation. Has the 25% rule for multi-cap funds changed how multi-cap funds are taxed? Not really.

How are multi-cap funds taxed

As equity-oriented funds, multi-caps follow the same tax rules:

- Short-Term Capital Gains (STCG): If you sell within 12 months, gains are taxed at 20%.

- Long-Term Capital Gains (LTCG): If you sell after 12 months, gains up to ₹1.25 lakh in a financial year are tax-free. Gains above ₹1.25 lakh are taxed at 12.5% (without indexation).

What this means for investors

The core question that matters to us: Is a multi-cap fund optimizing for market participation, strategic exposure, or just regulatory compliance?

The way most of us look at multi-cap funds is simple. We fall prey to this subtle mental trap that we can handle a little bit of volatility in the mid-cap and small-cap stocks just for higher returns. However, this same allocation can feel unbearable during unfavorable market conditions. What looked like diversification now feels like “too risky”. Investors often think, “The fund manager will handle it.” But in this case, you cannot rely on external expertise when markets get rough. Your emotions during market downtrends don’t care about SEBI’s 25% rule.

So the bigger question is about our psychology:

- Do we anchor our expectations on past performance, ignoring how we actually feel when markets are underperforming?

- Does the appearance of diversification make us more easy-going about the risks sitting quietly inside the portfolio?

If the decision seems too confusing, you can consult a Qualified Financial Advisor (QFA) who can guide you properly, while considering your financial interests.

Multi-cap funds are not good or bad. They are simply structured in a specific way. As investors, understanding that structure and its implications during both good and bad times is what really matters. Because in the end, it’s not about avoiding risk, but about knowing the kind of risk you are signing up for.