What is asset allocation? Understanding its meaning, importance, advan...

Asset allocation means spreading your money across different types of investments, li...

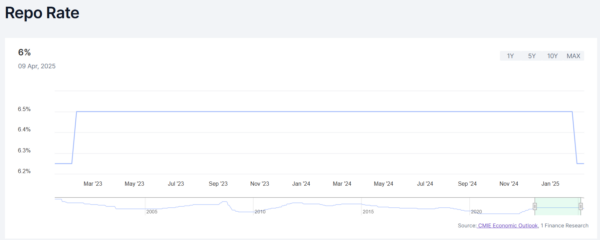

The Reserve Bank of India has cut the repo rate by 25 basis points once again, bringing it down to 6.0%. While the macroeconomic rationale for the cut is clear—to support domestic consumption and revive business sentiment—the question that matters most is: How does this affect your personal finance?

In this blog, we break down the implications of this policy decision on your loans, FDs, investments, and real estates.

This year, it’s the second time RBI cut the rates, last time it was in February, when it cut the rate by 25 bps.

At the 9th April 2025 meeting, the Monetary Policy Committee (MPC) of the Reserve Bank of India (RBI) unanimously voted to reduce the policy repo rate by 25 bps to 6.0%.

https://indiamacroindicators.co.in/data-at-a-glance/repo-rate

https://indiamacroindicators.co.in/data-at-a-glance/repo-rate

The RBI is acting to cushion the Indian economy from external shocks. With global trade disruptions and slowing growth, monetary easing is seen as a tool to:

1 Finance’s Macroeconomic research team anticipates that a further cut of 50 to 75 basis points could happen over the next year.

The extent of easing will depend on how quickly India can resolve the trade tensions with the US and how global demand evolves.

| Scenario | Additional Rate Cut Forecast |

| Trade tensions ease by end-2025 | 50 basis points |

| Uncertainty persists, and growth slows | 75 basis points |

Now the bigger and more important question is how will this repo rate impact your personal finance. Let’s talk about it one by one.

If you’re repaying a home loan, the RBI’s latest repo rate cut could work in your favor. But the impact on your monthly EMI depends on what kind of interest rate your loan is linked to. Let’s understand the effect of repo rate cut based on your type of interest rate:

A) Repo-Linked Floating Rate Loans

These are directly tied to the RBI’s repo rate. When the RBI cuts the rate, banks usually pass on the benefit quickly often within one to three months. If you have Repo-Linked Floating Rate Loans you may notice a drop in your EMI or a reduction in loan tenure, depending on the structure of your loan. Since October 2019, most new retail loans are offered under this format due to RBI regulations. This is the most responsive loan type to repo changes.

If your bank revises its interest rate, use this calculator to instantly see how it impacts your loan: Floating Interest Rate Calculator

B) MCLR-Linked Floating Rate Loans

MCLR (Marginal Cost of Funds-Based Lending Rate) is an internal benchmark set by each bank. While repo cuts influence MCLR, the transmission is indirect and delayed. Changes in your loan rate will only happen when your MCLR reset date arrives, typically every six or 12 months. So, the impact could take three to six months or even longer to reflect in your EMIs. These loans were more common before the repo-linked structure was mandated.

C) Fixed Rate Home Loans

Fixed rate loans do not change with repo rate movements during their lock-in period. Unless your agreement includes a reset clause, you won’t benefit from a rate cut. If rates drop significantly, you may consider refinancing to a floating-rate loan. These loans offer stability in a rising rate environment but can be a disadvantage when rates fall.

D) Loans Linked to External Benchmarks

Some loans are pegged to other external benchmarks like the Treasury Bill yield or the RBI repo rate, but with different reset cycles (monthly, quarterly, etc.). The effect of a repo rate cut depends on how frequently your bank resets the rate. Most borrowers will see changes within 3 months, making this structure fairly efficient and transparent.

Here’s summarised table for above information-

| Type of Loan | Effect of Repo Cut | Timeline of Impact |

| Repo-Linked Floating Rate Loan | Directly linked to the RBI’s repo rate | EMI or tenure may reduce in 1–3 months |

| MCLR-Linked Floating Rate Loan | Change depends on bank’s internal MCLR reset policy | Can take 3–6 months or longer |

| Fixed Rate Home Loan | No impact during lock-in period unless a reset clause is included | No change until reset or refinance |

| Loans Linked to External Benchmarks | Impact based on the specific benchmark and bank’s reset cycle | Usually within 3 months |

If you’re not seeing benefits or if your rate is higher than prevailing market rates:

In most cases, yes—but not immediately. Banks have recently been competing to attract deposits by offering higher FD rates, and many may prefer to hold current rates steady for a while despite the policy rate cut. However, if this rate cut cycle deepens, expect FD rates to gradually drift lower.

Currently, average FD rates across major banks remain close to 7%, but you should be prepared for downward revisions in the coming quarters.

FD rates may remain attractive in the short term, but if this repo rate cut marks the start of a broader easing cycle, FD returns might trend lower in the coming quarters.

At first glance, repo rate cuts are usually a good sign for the stock market. They lower borrowing costs, boost corporate margins, and support economic activity—all of which tend to push equity prices higher.

But today’s market environment, overwhelmed by global uncertainty, is more complicated than previous times. Here’s where we need to focus.

So while the RBI’s move is market-friendly on paper, equity markets remain cautious and volatile in the short term.

Plan for the long-term and stay invested. Focus on quality stocks that might benefit from lower interest rates.

Continue with SIP and Maintain discipline. Market dips can be an opportunity for cost averaging and planning for long-term investment.

Don’t time the market and avoid reacting to short-term volatility. Remember the saying “Time in the market is more important than timing the market”

Focus on Asset Allocation and rebalance your portfolio based on your financial personality, Generational profile and life goals.

Debt mutual funds are one of the quiet winners when interest rates fall—and the RBI’s repo rate cut could open the door for stronger returns, especially in select categories.

When interest rates decline, the price of existing bonds (issued at higher rates) rises. Debt mutual funds that hold these bonds see capital appreciation as a result. Let’s understand this in easier terms –

Imagine you bought a bond last year that pays 8% interest, but now, because the RBI has cut rates, new bonds are being issued at only 6%.

If you try to sell your 8% bond, investors will prefer it over the new 6% ones. So, they will be willing to pay more than its face value to get that higher return.

The price of your bond goes up, and that gain is called capital appreciatin.

Interest rate fall also boosts the Net Asset Value (NAV) of the debt mutual fund. Which helps you earn more not only from interest but also from price gains.

That’s said, the benefit will also depend on the type of debt fund you have.

| Fund Type | Why It Benefits |

| Gilt Funds | Invest in long-term government securities; highly rate-sensitive |

| Dynamic Bond Funds | Actively manage duration based on interest rate outlook |

| Long Duration Funds | Higher potential gains when rates are falling |

| Corporate Bond Funds | May benefit from falling yields and lower credit risk |

Debt funds—especially gilt and dynamic bond funds — are well-positioned to benefit from a falling interest rate environment. For investors looking for stable returns with low equity exposure, this could be the right time to revisit your debt portfolio.

Lower interest rates make home loans cheaper, and in theory, this should boost housing demand — especially among first-time buyers. But the actual impact on property prices depends on several market factors.

When the RBI cuts the repo rate, banks often reduce home loan rates. This:

If you are more interested in real estate you can read : https://1finance.co.in/report/the-reality-of-mumbai-realty.pdf

These blogs might also help you:

The affordable and mid-income housing markets stand to gain the most from lower rates. But for the overall real estate sector, price movement may remain moderate due to already elevated valuations and macro uncertainties.

The repo rate cut will have both direct and indirect effects on your personal finances—from reducing EMIs to influencing FD returns, mutual fund performance, and even property affordability.

If you want to take effective steps in response to this shift, now is a good time to speak with a financial advisor. A qualified advisor will help you:

Make most of repo rate cuts by making right financial decisions with qualified financial advisors.

Q1. What is the repo rate?

A: The repo rate is the interest rate at which the Reserve Bank of India (RBI) lends money to commercial banks. It is a key monetary policy tool used to control inflation, manage liquidity, and stimulate or cool down economic growth.

Q2. Why does RBI change the repo rate?

A: The RBI adjusts the repo rate to influence borrowing costs in the economy. A rate cut makes loans cheaper and boosts spending, while a rate hike helps control inflation by making borrowing more expensive.

Q3. How will a repo rate cut effect me?

A: A rate cut usually leads to lower EMIs on home or car loans, can reduce fixed deposit returns, and may positively influence mutual fund and real estate investments.

Q4. What is the current RBI repo rate?

A: As of April 2025, the repo rate stands at 6.0%, following a 25 basis point cut.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Asset allocation means spreading your money across different types of investments, li...

This blog will help you understand how investing can be a game changer.

Priya Kumar, a 40-year-old IT professional from Bengaluru, earns ₹1,50,000 monthly....