Popular searches

Product scoring may vary based on gender, age, policy tenure and sum assured.

The lowest age in the selected range is considered for price evaluation (e.g., 25 - 29)

Updated ITR Filing

Updated ITR FilingFile your updated ITR

(ITR-U) now.

Avoid paying more tax later.

Request a callback *

By clicking 'submit' you allow 1 Finance to get in touch with you

File your updated ITR

(ITR-U) now.

Avoid paying more tax later.

When can you file an updated ITR

(ITR-U)?

You can file an updated ITR under Section 139(8A) in the following situations:

1

Missed the revised ITR deadline

If the deadline for revised returns has passed.

2

Discovered errors later

If you find omissions, underreported income, or incorrect deductions after the assessment year ends.

3

Want to declare extra income

If you need to report unreported income to avoid future notices or penalties, voluntarily.

4

AIS/Form 26AS mismatches

If your data doesn't match even after the original filing, and you want to correct it to ensure compliance.

What are the benefits of filing an

ITR-U?

Fix errors even late:

You can correct mistakes, omissions, or missed income/claims within 48 months from the end of the relevant assessment year.

Avoid bigger penalties later:

Voluntary disclosure reduces the risk of scrutiny, high penalties, or prosecution from the Income Tax Department.

Claim refunds or adjust taxes:

If corrections lead to a higher refund or lower liability (after any additional tax), you can benefit—even though extra tax applies if liability increases.

Why choose 1 Finance for your updated return filing?

Don't go DIY

Ensure accuracy to avoid extra penalties or complications. Consulting a qualified expert is a better option than doing it yourself.

Experienced CAs to file ITR

Our Chartered Accountants will handle your updated ITR filing from start to finish—no chatbots or AI involved.

Full compliance, guaranteed

We guarantee that your taxes are filed accurately and in compliance with current tax laws.

What is the last date to file an updated return?

You can file an updated ITR up to 48 months from the end of the relevant assessment year (e.g., for AY 2025-26, up to March 31, 2030).

What are the additional tax liabilities while filing updated returns?

Different additional tax rates apply based on timing:

a) Within 12 months from end of assessment year: Additional 25% tax on net tax + interest.

b) Within 24 months: Additional 50% tax on net tax + interest.

c) Within 36 months: Additional 60% tax on net tax + interest.

d) Within 48 months: Additional 75% tax on net tax + interest.

e) Beyond that: Filing an updated return is not allowed.

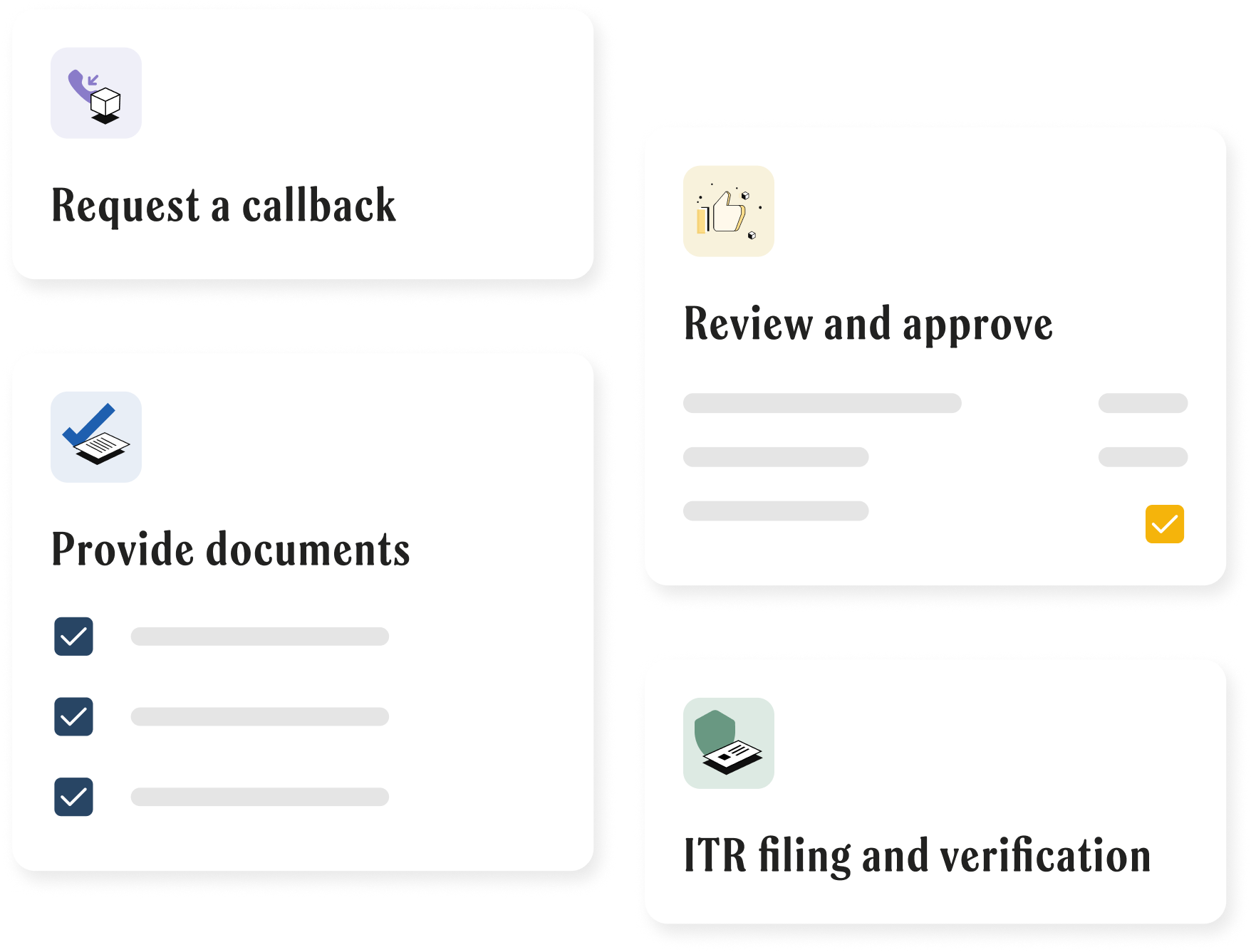

How to file your updated ITR with us

1

Contact us via WhatsApp or request a callback

Our team will reach out to you shortly.

2

Provide the necessary documents for ITR filing

Our CAs will send you the ITR computation.

3

You review and approve the tax computation

Then we will file your updated income tax return.

4

Once your ITR is filed, we will e-verify it

You will get ITR form and ITR acknowledgment via email.

FAQs on filing updated return (ITR-U) under Section 139(8A)

What is an updated ITR?

An updated ITR under Section 139(8A) is a tax return filed to correct errors, omissions, or to declare additional income after the deadline for original, belated, or revised returns has passed. It encourages taxpayers to comply voluntarily with tax regulations.

When should I file an updated ITR?

You should file an updated ITR if the deadline for revised ITRs has passed (for AY 2025-26, this was December 31, 2025) or if you later discover errors in your original filing.

Who can file an updated return?

Any taxpayer who has already filed an original return can file an updated ITR. This can even be done after receiving a notice, although it's preferable to file voluntarily to limit potential issues.

If I have not filed Original return, can I file now?

Yes, you can file an Updated Return even if you have not filed the Original or Belated Return for that year.

Do I need to e-verify the updated return?

Yes, you must e-verify the updated return, just like any regular ITR. If it is not e-verified, the updated return will be considered invalid.

Will I pay extra tax on the updated ITR?

Yes, if your tax liability increases. You will incur an additional tax of up to 75% depending on when you file updated ITR, along with interest.

Can I change the tax regime in an updated return?

No, you cannot change the tax regime selected in your original return. For specific queries, it's advisable to consult a Chartered Accountant.

Can I file an updated ITR for previous years?

Yes, you can file an updated ITR for past years, provided it's within 48 months from the end of the relevant assessment year.

How many times can I file an updated ITR?

You are allowed to file only one updated ITR per assessment year. This updated return will replace any previous filings for that year if submitted within the stipulated time.

Does an updated return substitute the original?

Yes, your updated return becomes the final corrected return for processing and supersedes any earlier versions for that assessment year.

Can I file an updated ITR after receiving a notice?

Yes, you can file an updated ITR after receiving a notice; however, it is generally better to file it voluntarily before any notices are issued to lessen the likelihood of incurring higher penalties. Our experts can provide guidance for your situation.

Thank you!

We'll get in touch with you soon.