Book a free consultation

Book a free consultation

How to Invest in Mutual Funds

“Mutual funds were created to make investing easy, so consumers wouldn’t ...

Book a free consulation

Book a free consulation

Get advice on investing, insurance, tax planning, loan management, etc, for free with a Qualifed Financial Advisor

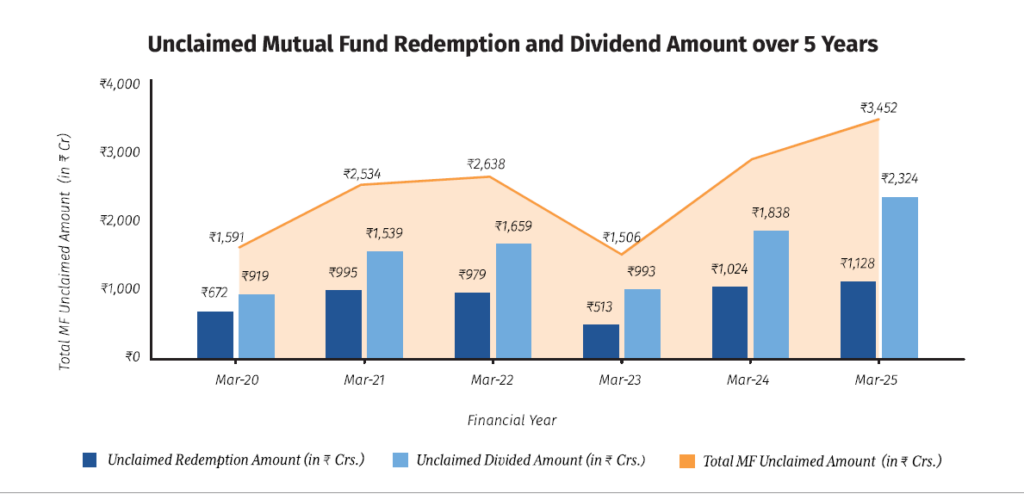

Unclaimed mutual funds in India are no longer a rounding error. It’s a ₹3,542 crore reality from FY 2024-25, built up from dividends and redemption proceeds that never made it back to investors’ bank accounts. Data from regulators, analysed by 1 Finance Magazine, shows this pot has been rising every single year. Most investors are unaware these units exist in their names, let alone how to check or claim them.

That being said, there’s a real chance a portion of this “forgotten money” could be linked to your PAN without you realising it. That’s why Securities and Exchange Board of India (SEBI) has built tools to help you trace inactive folios and unclaimed mutual fund units across asset management companies (AMCs) in one place. And turn what feels like a vague possibility into a clear yes-or-no answer about whether some of that ₹3,542 crore is actually yours.

When you invest in mutual funds, the fund house allots units to your folio (your unique account with that fund house). These units keep moving in value with the fund’s NAV (net asset value). Over time, though, some units may simply fall off your radar; you don’t redeem or track them. There’s no activity on that folio for years, even though the investment itself is still active. In simple terms, these are “unclaimed” mutual fund units; investments that exist in your name, but are no longer being followed or acted upon by you.

Unclaimed isn’t the same as lost, though the fund house continues to hold those units against your folio until you step in and claim/redeem them.

A few small, unattended gaps for years are enough to turn a regular, active folio into “unclaimed”, while you stay completely unaware. They include:

The investor passes away without a proper nomination: This is often the single biggest driver of unclaimed mutual fund assets. When no nominee is registered, or the nominee has no idea the investment exists, the units just sit in the folio, legally intact, but practically invisible to the family.

Outdated or incorrect contact details: You change your mobile number, email, or address, but don’t update it with the fund house or in your KYC. Over time, emails bounce, SMS alerts stop reaching you, and the folio slowly slips into dormancy.

Old investments that are simply forgotten: A one‑time lump‑sum from years ago, a small SIP you stopped without redeeming, or even MF units received as a gift. Once they fall off your mental map, they just keep existing in the background somewhere in some folio.

Dividend cheques that were never deposited: If you had chosen the dividend payout option and cheques were repeatedly undelivered or never banked, those unpaid payouts get tagged as unclaimed. The units are still there, but the cash flows linked to them pile up in the unclaimed bucket.

Technical or mismatch issues: Even fully aware investors can get stuck because of a mismatch in PAN, name spelling, bank account, or address. Until those errors are fixed, the fund house cannot complete the payout, and the amount due to you quietly migrates into the unclaimed pool.

That ₹3,452 crore figure from FY 2024-25 is the latest point in a steady yearly climb in unclaimed dividend and redemption amounts. As reported by 1 Finance Magazine, citing SEBI Annual Reports FY25, the overall pool of unclaimed mutual fund money has grown by more than 20% annually, from ₹2,862 crore in FY 2023-24.

Each bar in that chart you see represents mutual fund units that are very much alive inside investor folios. However, they have effectively become invisible to the people who own them.

For the first 30 days, any unpaid redemption or dividend simply remains as an unpaid entry in your folio at the AMC/RTA (Registrar and Transfer Agent) level. After that, SEBI prescribes a clear regulatory framework for what fund houses must do with unclaimed amounts. Let’s break it down:

The 3-year rule: where your money goes after 30 days

If mutual fund redemption amounts or dividend payouts remain unclaimed for more than 3 years, the fund house transfers that money to a separate plan under the scheme, called Unclaimed Dividend/Redemption Scheme (UDRS).

During these initial 3 years, the money is parked in very low-risk, liquid instruments, like call money, money market instruments or in a separate plan of overnight/liquid/money market schemes. So, it continues to earn some income instead of lying idle. Hence, the money doesn’t go to the government immediately.

The units in this scheme are typically allotted on a weekly or fortnightly basis. This depends on when banks report which cheques or credits have remained paid. The key point for you: the amount is still mapped to your AMC folio in a conservative, liquid‑like plan, and you can claim it at any time in this period.

The critical 4th Year: When IEPF enters the picture

After those first 3 years, if you still haven’t claimed your amount by then, SEBI’s framework says you will only get:

From the fourth year onwards, any further income earned on that unclaimed corpus is no longer credited to you. Instead, it is transferred to the Investor Education and Protection Fund (IEPF). In other words, the longer you wait beyond 3 years, the more appreciation you forfeit to the IEPF, even though the principal amount is still yours.

The good news: There is no expiry date on your right to claim your unclaimed mutual fund assets; they are still redeemable. So, how do you even find it out? Let’s get into that.

Method 1: MF Central and MITRA

MF Central, the industry‑wide service platform jointly run by CAMS and KFintech, is your first stop. Within MF Central, SEBI has introduced MITRA (Mutual Fund Investment Tracing and Retrieval Assistant), a dedicated search tool that lets you track across fund houses in one place. Along with missed payouts, it flags both unclaimed amounts and inactive folios that may still hold units linked to your PAN.

Here’s how you can use it:

You will see a consolidated view of folios, along with links or instructions to initiate the claim process with the respective fund houses. If there are none, you will simply “No Data Found”.

Method 2: AMFI’s official website

Association of Mutual Funds in India (AMFI) offers a central lookup for unclaimed mutual fund redemption and dividend amounts, which works well as a quick, no-login cross-check.

Here’s how:

Method 3: Individual AMCs’ websites

If you remember the AMCs you invested with, you can check directly on their websites. Each fund house must disclose unclaimed redemption/dividend amounts and how to claim them.

The AMC’s must:

However, the onus of actively claiming the money still rests with you.

Method 4: CAMS & KFintech (RTAs)

Most mutual funds in India are serviced by two RTAs, CAMS and KFintech; they maintain your folio‑level records and help you generate a Consolidated Account Statement (CAS) that includes active as well as unclaimed units.

CAMS: Under the Unclaimed IDCW / Redemption section, you can check if any unpaid dividends or redemption amounts are lying against your PAN. Enter your PAN, date of birth, and mobile number to receive an OTP, and the system will display any unclaimed entries linked to your details. You can also request a Consolidated Account Statement (CAS) using your PAN and registered email to see all CAMS‑serviced mutual fund folios in one statement, including active and unclaimed amounts.

KFintech: Similarly, KFintech provides an online facility to check unclaimed IDCW/redemption amounts for schemes it services. Visit the relevant unclaimed amount page, enter your PAN and other basic credentials, and follow the prompts to view any unpaid amounts mapped to your folios.

In both cases, you can also email CAMS (support@camsonline.com) or KFintech (investorrelations@kfintech.com) with your PAN and registered email ID, requesting a CAS.

Now, the process to reclaim them depends on whether you are the original investor or a legal heir. Let’s cover both scenarios.

You are the original investor

You are a legal heir (Claiming on behalf of a deceased investor)

Documents you will need for Transmission of Units:

| In case of death of sole or all unitholders (For nominee) | In case of death of sole or all unitholders (When there’s no nominee) | In case of death of the 1st holder | In case of death of 2nd and/or 3rd holder |

|---|---|---|---|

| 1. Transmission Request Form (Form T3) 2. Death certificate of the investor 3. Birth Certificate (Nominee is minor) 4. PAN Card (Nominee) 5. KYC Acknowledgment 6. Cancelled cheque with Nominee’s name/Recent Bank Statement/Passbook 7. ID proof [PAN/Redacted Aadhaar/Voter ID / Passport] of the deceased | 1. Transmission Request Form (Form T3) 2. Death certificate of the investor 3. Birth Certificate (Nominee is minor) 4. PAN Card (Nominee) 5. KYC Acknowledgment 6. Cancelled cheque with Nominee’s name/Recent Bank Statement/Passbook 7. ID proof [PAN/Redacted Aadhaar/Voter ID / Passport] of the deceased | 1. Transmission Request Form (Form T2) 2. Death certificate of the investor 3. PAN Card of the surviving jointholder 4. Cancelled Cheque of the new first holder/Recent Bank Statement/Passbook 5. KYC Acknowledgment | 1. Transmission Request Form (Form T1) 2. Death certificate of the investor 3.Fresh Bank Mandate Form 4. Cancelled cheque of the new bank account 5. Fresh Nomination Form (or Nomination Opt-out form) 6. KYC Acknowledgment or KYC Form of the surviving unit holder(s) |

Scroll right to view full table →

For a complete breakdown of how transmission and death claims work for mutual fund units in India, you can refer to AMFI’s official guidelines “Procedure to Claim Units / Proceeds upon death of a Unitholder”.

Here’s the step-by-step process:

If the unclaimed amount <₹5 lakh, most fund houses allow an indemnity‑based process without a court succession certificate. For the amount between ₹5 lakh – ₹10 lakh, you may need Registered Will, Legal Heirship Certificate, etc. For >₹10 lakh, a succession certificate is usually required.

After the money hits your account, you can either keep it as cash, reinvest it into your current asset allocation, or choose to stay invested.

Let our Qualified Financial Advisors guide you

The key is to consciously place it back into your overall financial plan instead of letting it drift again. Our qualified financial advisor (QFA) can help you run a complete audit of your existing investments, identify any unclaimed or dormant assets, and help you build a personalised plan going forward. Reach out to us, this is exactly what we are here for.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Get advice on investing, insurance, tax planning, loan management, etc, for free with a Qualifed Financial Advisor

Explore

“Mutual funds were created to make investing easy, so consumers wouldn’t ...

Know the risks of multi-asset funds, not just returns

Explore the versatility of Hybrid Mutual Funds, from their diverse categories to the ...