Book a free consultation

Book a free consultation

Here’s the Most effective Strategy for Retirement Planning

Discover a practical framework to plan for retirement with clarity and discipline.

Retirement is inevitable and the cruel equation of this phase is that your income stops, but your expenses don’t. In fact, as you get older, those expenses often multiply. You are entering a second life that could last thirty or forty years, a life where you need money to keep flowing even when you aren’t working to earn it.

You might have heard the advice to “save” for retirement, but in 2026, simply saving your money is a losing game. To survive, you have to invest. So how exactly do you invest for retirement? It starts by understanding why it’s important, choosing the right options in the right proportions, and knowing when to get professional help. In this article, we talk about exactly that.

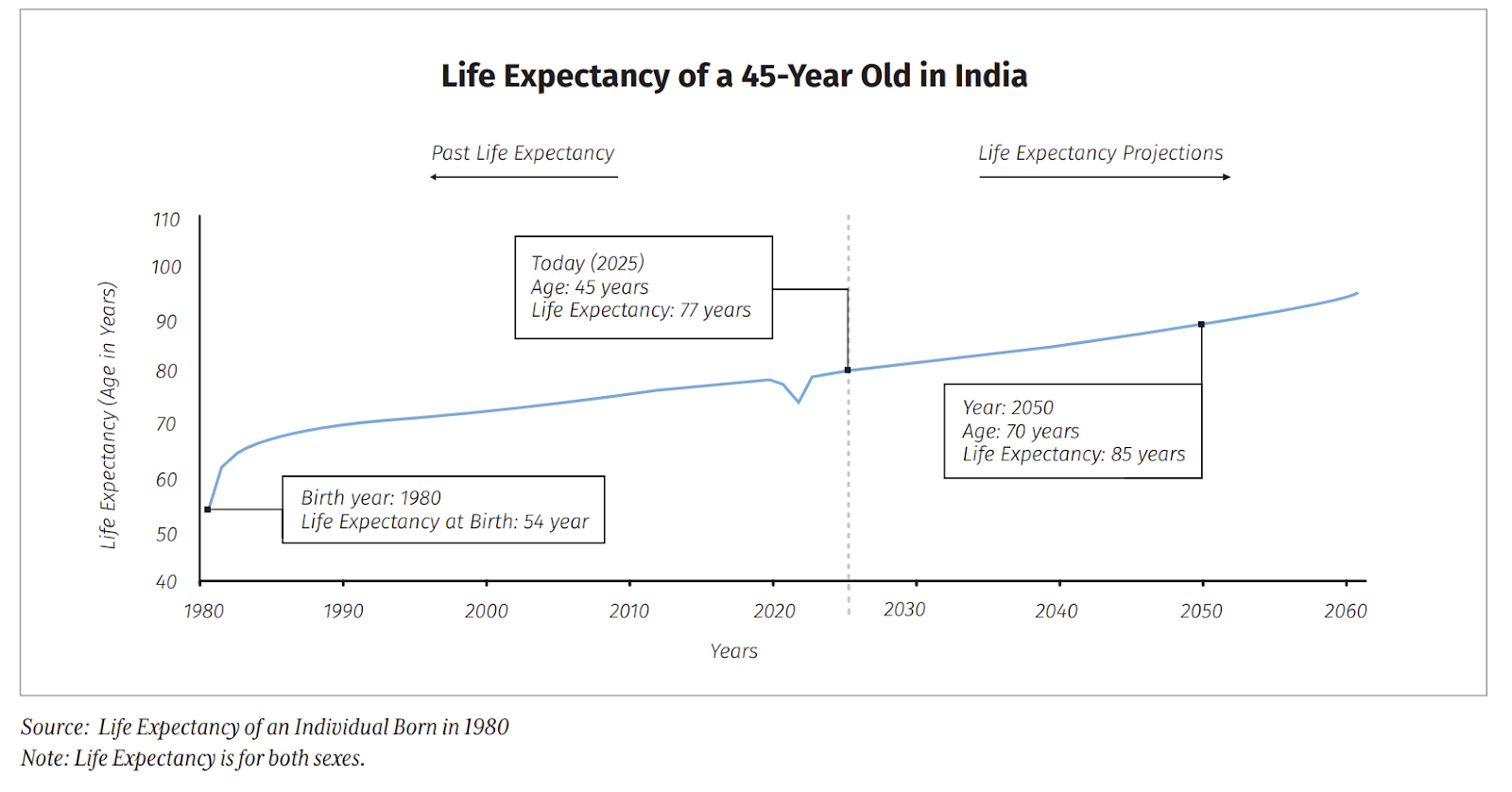

Gone are the days when retirement lasted just 10–15 years and you only had to plan for this short phase. With rising life expectancy, it can now stretch 30–40 years or more. The biggest threat here is longevity risk, the financial danger of outliving your savings because you live longer than expected.

As mentioned in 1 Finance magazine, according to UN data, if you were born in 1980, your life expectancy back then was around 54 years. Today, at 45, it has already increased to about 77. By the time you turn 70 in 2050, chances are you’ll live past 85, and there’s a 50% chance you’ll make it well into your 90s

Source: 1 Finance Magazine

This means you will have more years without income. But more than that, we also face a very real and very serious possibility of you outliving your money.

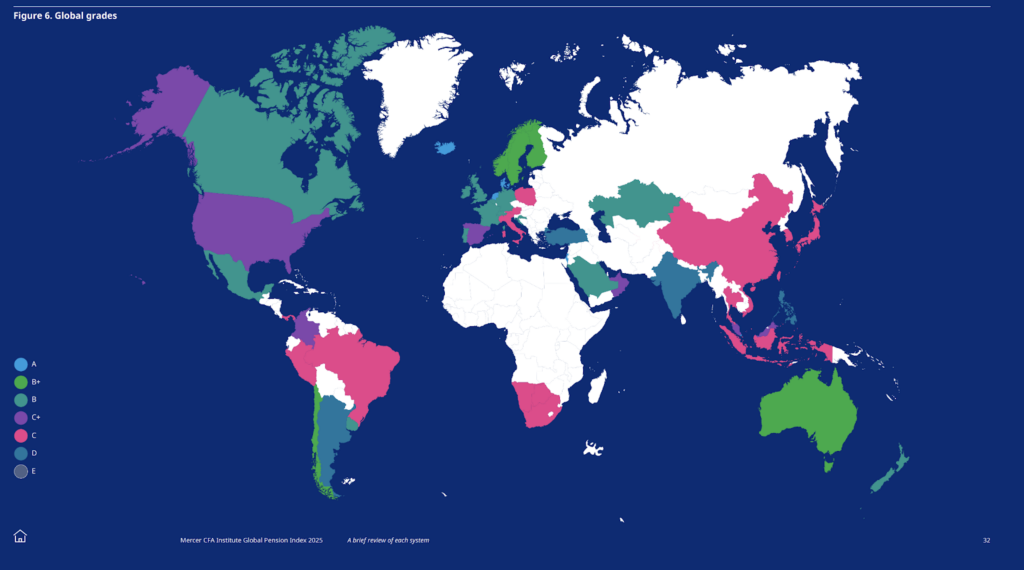

You might assume the system will take care of you. Unfortunately, India doesn’t have a universal social security safety net. Look at the map attached below.

According to the Mercer CFA Institute Global Pension Index, India’s pension system is rated D.

Source: Mercer CFA Institute Global Pension Index

India’s current retirement structure includes:

And if you work in the unorganised sector, there’s virtually no formal safety net at all.

In a country with rising longevity but no universal safety system, where medical costs have doubled every 5-7 years, your investment portfolio becomes your only parachute.

The earlier and smarter you invest, the greater your chances of living with dignity, not dependency.

You’ve probably heard people call retirement investing “saving for your golden years.” If you stick to the traditional idea of saving for retirement, you’re watching an ice cube melt in the Mumbai sun.

Today, retirement isn’t just an age. It’s a transition from human capital (your ability to earn) to financial capital (your money’s ability to earn). It’s about buying future cash flow.

Let’s put it simply: to survive a long retirement, your investments must do three things.

Let our Qualified Financial Advisors guide you

If you are waiting for a “stable” moment in your career or for your home loan to vanish before you start, you are doing great harm to yourself.

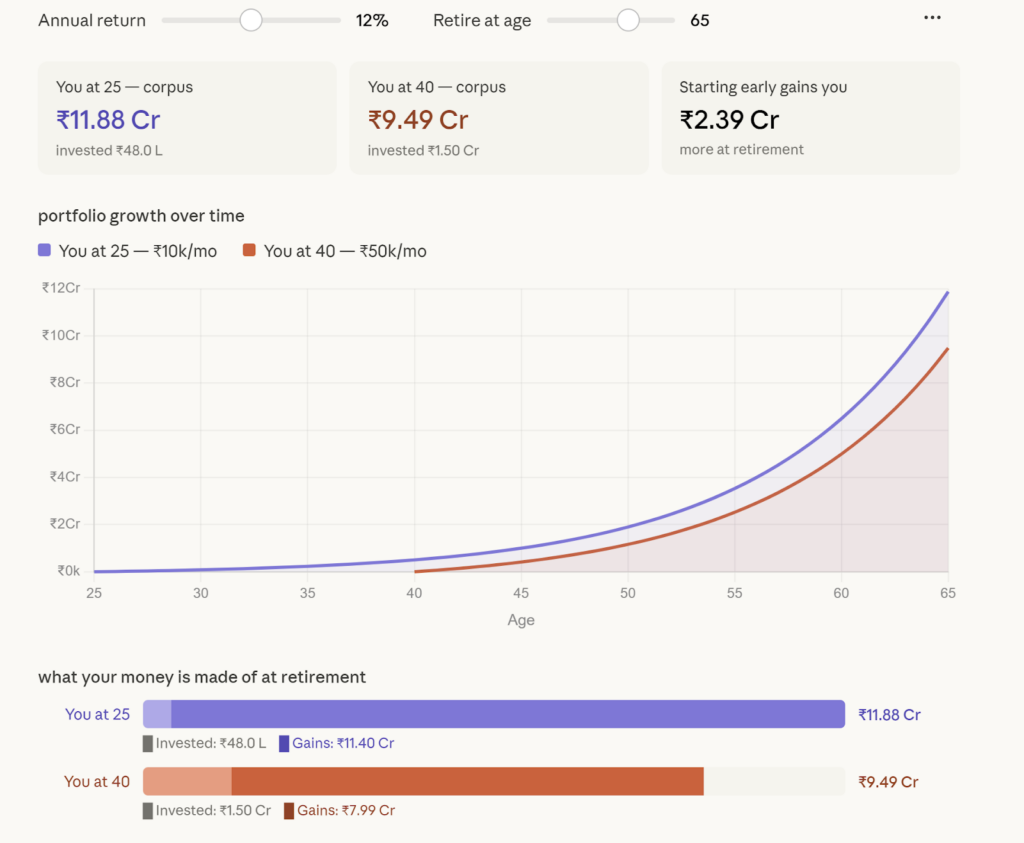

Every year you delay retirement, you lose the power of geometric growth.

If you start at 25 with ₹10,000 a month, you will almost certainly end up with a much larger corpus than a 40-year-old starting with ₹50,000. Why? Because the 25-year-old gave their money two extra decades to compound, to let the interest earn interest, and then let that interest earn even more.

Source: 1 Finance research

At the default 12% return retiring at 65, you investing ₹10k/month from age 25) builds ~₹11.7 Crore while you investing (₹50k/month from age 40) builds ~₹9.4 Crore, despite putting in 5x the monthly amount and investing over ₹1 Crore more in total.

In 2026, the “best time” to start was the day you got your salary. The second best time is right now. Every month you wait is another month you’ll have to work in your 70s.

The Indian landscape has matured, and the old “FD-only” strategy is now a way for financial erosion. You need to build your own parachute using these five specific pillars:

If you want to beat inflation and build a solid, reliable portfolio, equity is non-negotiable. Let’s look at some suitable instruments.

NPS is one of the best ways to save tax while building a retirement fund. Even under the New Tax Regime of 2026, it remains a strong option.

Pros:

Cons:

These are funds where experts try to beat the market and deliver higher returns.

You pay a higher expense ratio (0.5%–2%) for the chance to outperform the Nifty 50. Younger investors (30s and 40s) who can stomach the volatility for the “alpha” (extra returns) that compound significantly over 20 years.

Pros:

Cons:

Passive investing has exploded in India by 2026 because most large-cap active managers are failing to beat the index after fees.

Pros:

Cons:

You don’t buy debt to get rich; you buy it so that a bad year in the stock market doesn’t ruin your finances.

PPF remains the last standing fortress of Exempt-Exempt-Exempt (EEE) status.

Pros:

Cons:

B) Employee Provident Fund (EPF) & VPF

For the salaried class, the Employee Provident Fund is the default safety net.

Pros:

Cons:

C) Government bonds & treasury bills

Government bonds are direct loans to the government, hence they carry almost zero credit risk.

Pros:

Cons:

D) Corporate bonds

Loans to good companies (AAA/AA-rated) with slightly higher returns than government bonds.

Pros:

Cons:

E) Fixed deposits (FDs)

The most popular debt option for Indian households.

Pros:

Cons:

F) Debt mutual funds

These have undergone a radical change. Units bought after April 1, 2023, no longer get “indexation” benefits.

Pros:

Cons:

G) Senior Citizen Schemes: SCSS & PMVVY

These are only available once you hit age 60.

Pros:

Cons:

3. Real estate

Real estate can act as a long-term store of value, offer rental income, and provide some protection against inflation, especially in growing urban pockets. It is illiquid and concentrated though, so it should complement, not replace, your equity and debt investments.

Pros:

Cons:

REITs & InvITs

In 2026, SEBI has made these much more accessible. They are now officially treated as Equity-like instruments for taxation and liquidity.

They pay out 90% of their cash flow as dividends. It’s equity growth plus a “rent” check.

Pros:

Cons:

4. Gold and silver

Gold and silver work as crisis assets: they tend to hold value when currencies or markets are under stress, and they help diversify a portfolio that is otherwise heavy on equity and fixed income. For most investors, owning them through ETFs or sovereign gold bonds is cleaner and safer than dealing in physical metal.

Pros:

Cons:

Let our Qualified Financial Advisors guide you

Now that you know the instruments, the most dangerous thing you can do is throw your money at them disproportionately. In 2026, Asset Allocation is everything. In fact, you should think of it as the most fundamental law for a successful retirement.

You can’t just buy a little bit of everything and hope for the best. Asset allocation is about deciding exactly how much of your wealth goes into the “Growth Engine” (Equity), the “Shield” (Debt), and the “Diversifiers” (Gold/REITs). It is the difference between a portfolio that collapses during a market dip and one that survives for forty years. If your allocation is wrong, no single “great stock” or “high-interest FD” can save you.

Below is a sample asset allocation for an investor during the strong recovery phase:

| Age Group | Equity | Real Estate | Passive Income | Alt. Investments | Debt |

| Below 35 | 39% | 35% | 8% | 14% | 4% |

| 36–45 | 35% | 33% | 13% | 15% | 5% |

| 46–55 | 30% | 30% | 18% | 13% | 10% |

| Above 55 | 21% | 26% | 29% | 9% | 16% |

But remember: these are template allocation based on algorithms. A true asset allocation for you depends on various factors, such as your unique financial personality and risk tolerance. For this, you should always talk to a Qualified Financial Advisor to build a plan that fits your specific life.

If you enter your 60s without robust, independent health cover, you are simply self-insuring against a catastrophe. A single fortnight in a private ward for a heart procedure or a prolonged recovery can trigger a “wealth reset,” wiping out five years of disciplined SIPs in a matter of days.

Health insurance is non-negotiable. Ensure you buy a suitable policy that stands independent of any corporate cover.

Most importantly: Never commit the mistake of mixing insurance with investment. A product that promises to both protect your life and grow your money usually fails at both, leaving you under-insured and your returns trailing behind inflation.

Partner with a Qualified Financial Advisor

You wouldn’t perform surgery on yourself just because you read a medical blog, and you shouldn’t “self-medicate” your 30-year retirement plan either. Investing is a complex journey — with new instruments like REITs and the constant noise of social media “finfluencers.”

This is where a Qualified Financial Advisor becomes your most valuable asset. They aren’t just there to pick stocks; they are there to provide the “emotional guardrails” that keep you from making expensive mistakes when the market dips.

A good financial advisor solves your three biggest retirement headaches:

> They calculate how much money you’ll really need based on your lifestyle, not some generic formula.

> They plan withdrawals from NPS, EPF, and mutual funds so you keep more money and pay less tax.

> As you age, they move your money from risky growth investments to safer ones — so you don’t have to worry about timing the market.

A Qualified Financial Advisor doesn’t cost money. They save you from expensive mistakes that could ruin your retirement.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Discover a practical framework to plan for retirement with clarity and discipline.

Retirement planning is an essential aspect of personal finance, ensuring that you hav...

This blog explores modern alternatives to traditional pensions for retirement plannin...