Book a free consultation

Book a free consultation

One financial plan doesn’t fit all: The importance of personalised p...

Personalised financial planning starts with who you are.

There is a kind of optimism that costs nothing today and everything later. India’s soon-to-be retirees, I am afraid, have it in spades, and a survey by 1 Finance Magazine has put a number on it.

Key takeaways

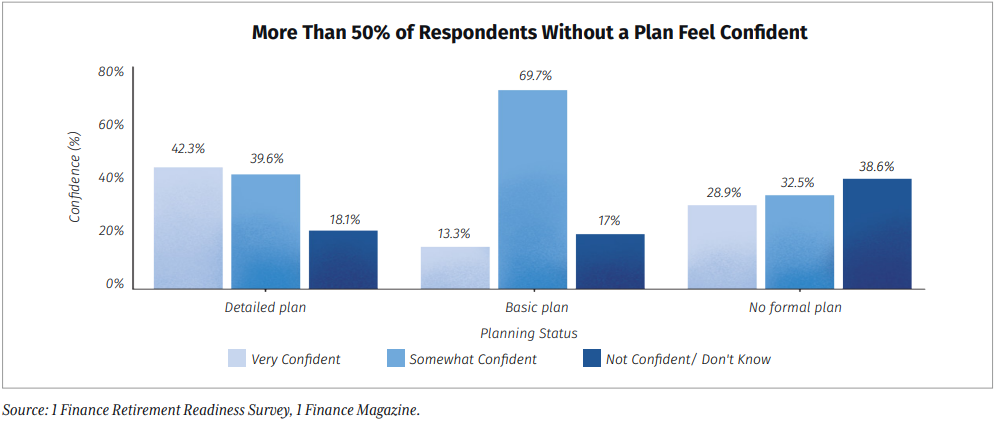

The survey, conducted by 1 Finance Magazine among 1,218 people aged 40 to 60, put the question to the generation now close enough to retirement to see it coming. Three out of four admitted they had no detailed plan for life after work. Fair enough; planning is tedious and the future is far away.

The part that stopped me and may also stop you cold is what came next. Of those who confessed to having no plan, 61.4% said they felt confident they would retire comfortably anyway.

In other words, the less someone had done about retirement, the better they felt about it. It has a name and the name is, the confidence-planning paradox.

Now you and I would expect the diligent saver, the one who has planned it all and has a number in mind, to sleep soundest when it comes to retirement planning. Instead, the survey found the opposite. Among Indians who had actually built a detailed plan, only 42.3% described themselves as very confident.

The planners, having looked under the bonnet, came away nervous for retirement. The non-planners, having never opened it, were relaxed.

Psychologists call this the Dunning-Kruger effect, the tidy little tragedy in which incompetence and confidence move in opposite directions, because the very knowledge that would humble you is the knowledge you don’t have.

A retirement plan, done properly, is essentially a machine for generating well-earned anxiety. It forces you to confront inflation, longevity and medical bills all at once.

Most Indians, I suspect, have simply never switched the machine on. Roughly 25% have a proper plan; about 50% have something they describe, charitably, as “rough”; the rest have nothing at all and feel terrific about it.

Let our Qualified Financial Advisors guide you

What makes the confidence so misplaced, to my mind, is the size of the gaps it is papering over.

The median retirement corpus among those surveyed was about ₹28 lakh, against a self-reported target of ₹1 crore, a shortfall of more than three times. You might assume this is a problem of the poor, of people who would love to save more and can’t. I assumed something like that too, and the data corrected me.

The gap actually widens as you climb the income ladder. At the top, the average corpus of ₹50 lakh sat against a target of ₹4 crore, an eight-fold shortfall. The rich are not better prepared. They are more expensively unprepared, and just as cheerful about it.

Then there is the small matter of how long retirement now lasts. Nearly six in ten respondents expected their money to run dry before they turned 80. The trouble is that an urban Indian who reaches 60 today can expect to live another 22 to 24 years, comfortably into the late eighties.

People are budgeting for a retirement that ends roughly when the real one is only getting going. I can think of no gentler way to put it than this: it is like packing for a weekend and then staying a fortnight.

The largest expense of old age is the one almost nobody is reading. Around 60% told the survey they expect their costs to fall once they stop working. For groceries and commuting, perhaps. But Indian healthcare inflation is running at 12% to 14% a year, several times the headline rate.

A hospital stay that costs ₹5 lakh today could cost ₹16–19 lakh by the time a 60-year-old turns 75. The expense people are most confidently assuming is the one most likely to bankrupt them.

You might wonder why nobody points this out to them. The answer is that almost nobody is asked. 76.9% of respondents said they had never once sought professional financial advice. Overconfidence is a hothouse flower; it thrives only where no outside voice is allowed in. The entire job of a financial planner is to be the irritating presence in the room muttering about inflation and life expectancy.

Let our Qualified Financial Advisors guide you

India has long treated retirement less as a financial event than as a sentimental one, a reward for decades of work, to be filled with grandchildren, temple visits and the travel you never had time for. Framed that way, it feels like something you have earned rather than something you must fund.

And lurking beneath the optimism is an older, fraying assumption: that the joint family will catch you. A good number of respondents still expect to lean on their children or their property if the savings run short. But the joint family was India’s original pension scheme, and it is being quietly wound up by nuclear households, migration and the rising cost of raising the very children who were meant to provide the safety net.

The truth is already leaking through the confidence, even if people won’t say it out loud. Some 64% told the survey they plan to keep working into their so-called retirement. For a lucky few that is a choice. For most it is a confession dressed as a plan, an admission that the comfortable retirement they feel so sure about will, in practice, require them never quite to retire.

What India’s middle-aged need is not more confidence. It is the useful, productive kind of dread that the survey shows actually visits the people who have done their sums. The first honest retirement plan a person draws up will almost certainly make them feel worse. That sinking feeling is not a flaw in the exercise. It is the entire point — and it is the one signal the confident majority is busy refusing to hear.

How do I plan for retirement in India?

Retirement planning works best as a sequence rather than a guess:

This is a general framework, not personal advice; a Qualified, fee-only adviser can tailor it to your situation.

How much retirement corpus do I need?

A widely used starting point is 25 to 30 times your expected annual expenses at retirement, which assumes you withdraw a sustainable 3–4% a year. If you expect to spend ₹6 lakh a year, that points to a corpus of roughly ₹1.5–1.8 crore in today’s terms — more once you adjust for inflation. The 1 Finance survey’s ₹1 crore median target shows most Indians are aiming low, and the typical ₹28 lakh corpus falls far shorter still.

Why do I need a financial advisor for retirement planning?

A good adviser does the work most people avoid: pressure-testing your assumptions about lifespan, inflation and medical costs, and stopping the false confidence the survey exposed. They build a withdrawal strategy, match investments to your timeline, and rebalance as you age. In India, look for a SEBI-registered investment adviser (RIA) — and note that 76.9% of those surveyed had never sought professional advice at all.

How can I get started with retirement planning today?

Start small and start now, because compounding rewards early movers:

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Personalised financial planning starts with who you are.

When it comes to managing money, everyone approaches financial decisions differently....

With MoneySign®, get personalized insights to build better money habits.