The new tax regime is the default way you are taxed for FY 2025-26 (AY 2026-27). It has lower slab rates than the old regime and an enhanced rebate that makes income up to ₹12 lakh tax-free. This guide lays out the slabs, explains the Section 87A rebate and marginal relief, shows the tax at different income levels with worked examples, and lists the few deductions you can still claim.

For a side-by-side comparison with the old regime, see our old vs new tax regime guide. For the full filing process, see our complete ITR filing guide for FY 2025-26.

Key takeaways

- Income up to ₹12 lakh is tax-free under the new regime because of the Section 87A rebate of up to ₹60,000.

- With the ₹75,000 standard deduction, a salaried person earning up to ₹12.75 lakh pays no tax.

- Marginal relief keeps the tax small for income just above ₹12 lakh.

- The new regime is the default under Section 115BAC, but removes most deductions like 80C, 80D, and HRA.

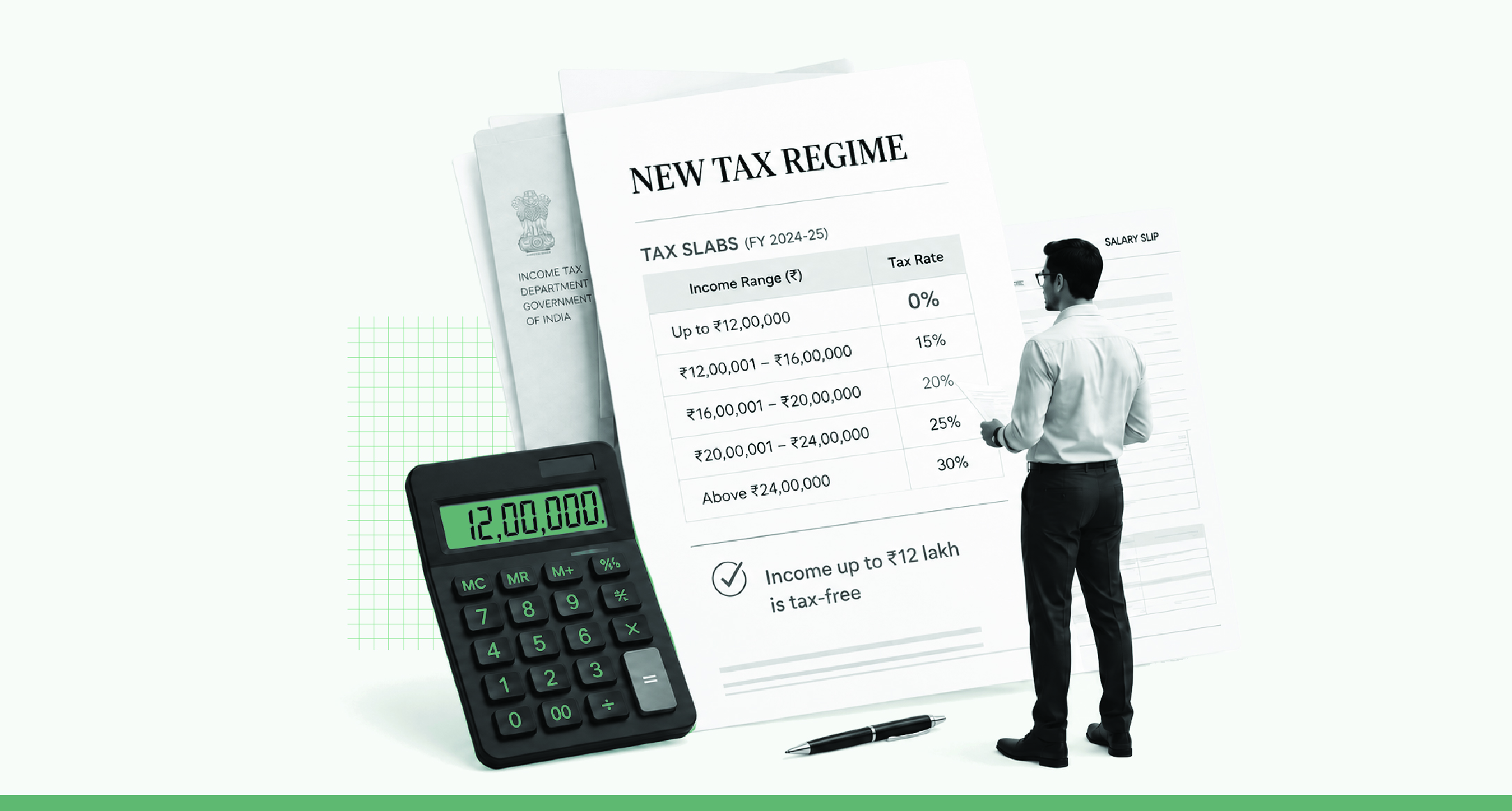

New tax regime slabs (FY 2025-26)

| Income slab | Tax rate |

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

These slabs are the same for everyone, including senior citizens. The new regime does not give the higher age-based exemption that the old regime does — the basic exemption is ₹4 lakh for all individuals. A 4% Health and Education Cess applies on the final tax under this regime, as it does under the old one. The same slabs continue for FY 2026-27, with no change announced in Budget 2026.

The Section 87A rebate: Income up to ₹12 lakh is tax-free

The biggest feature of the new regime is the Section 87A rebate. For FY 2025-26, a resident individual with taxable income up to ₹12 lakh gets a rebate of up to ₹60,000, which cancels out the tax entirely. So if your taxable income is ₹12 lakh or less, your tax is zero.

Two conditions are worth remembering. The rebate is only for resident individuals, and it applies only to normal income. Special-rate income such as capital gains under Sections 111A and 112A is not covered by the rebate, so you can still owe tax on that part even if your total is around ₹12 lakh.

The ₹75,000 standard deduction: ₹12.75 lakh tax-free for the salaried

Salaried individuals and pensioners get a standard deduction of ₹75,000 under the new regime, raised from ₹50,000. This is subtracted from your salary before tax is calculated.

Because of it, a salaried person earning up to ₹12.75 lakh has taxable income of ₹12 lakh after the standard deduction, which the rebate then makes tax-free. This is why ₹12.75 lakh is the tax-free salary figure you often see for the new regime, while ₹12 lakh is the tax-free figure for taxable income.

Marginal relief: What happens just above ₹12 lakh

Without a cushion, earning slightly more than ₹12 lakh would create a sharp tax jump, because the rebate stops applying. Marginal relief prevents this.

If your taxable income crosses ₹12 lakh by a small amount, your tax is limited to the amount by which your income exceeds ₹12 lakh. For example, with a taxable income of ₹12,25,000, the normal slab tax would be ₹63,750, but marginal relief caps it at ₹25,000 — the excess over ₹12 lakh — which becomes ₹26,000 after cess. This relief continues until roughly ₹12.70 lakh of taxable income, after which the regular slab tax applies in full.

Worked examples: Tax at different income levels

These figures are for a salaried person with only the ₹75,000 standard deduction, and include 4% cess.

| Gross salary | Taxable income (after ₹75,000 deduction) | Tax payable (incl. cess) |

| ₹8,00,000 | ₹7,25,000 | ₹0 |

| ₹12,00,000 | ₹11,25,000 | ₹0 |

| ₹12,75,000 | ₹12,00,000 | ₹0 |

| ₹13,00,000 | ₹12,25,000 | ₹26,000 |

| ₹16,00,000 | ₹15,25,000 | ₹1,13,100 |

| ₹20,00,000 | ₹19,25,000 | ₹1,92,400 |

| ₹24,00,000 | ₹23,25,000 | ₹2,92,500 |

| ₹30,00,000 | ₹29,25,000 | ₹4,75,800 |

Take the ₹20,00,000 salary. After the ₹75,000 deduction, taxable income is ₹19,25,000. The tax is nil on the first ₹4 lakh, ₹20,000 on the next ₹4 lakh (5%), ₹40,000 on the next ₹4 lakh (10%), ₹60,000 on the next ₹4 lakh (15%), and ₹65,000 on the remaining ₹3.25 lakh (20%) — ₹1,85,000 in total, or ₹1,92,400 after 4% cess.

Deductions you can still claim in the new regime

The new regime removes most deductions, but a few remain:

- Standard deduction of ₹75,000 for salaried individuals and pensioners.

- Employer’s contribution to NPS under Section 80CCD(2), up to 14% of basic salary. This is the most valuable deduction available in the new regime for salaried taxpayers.

- Family pension deduction — the lower of one-third of the pension or ₹25,000.

- Contribution to the Agniveer Corpus Fund under Section 80CCH.

- Interest on a let-out property under Section 24(b) (but not on a self-occupied home).

- Exemptions such as gratuity, leave encashment, and NPS maturity proceeds, where conditions are met.

Deductions you cannot claim in the new regime

These common deductions and exemptions are not available:

- Section 80C investments — PPF, ELSS, life insurance premiums, EPF, and home loan principal.

- Section 80D health insurance premiums.

- House Rent Allowance (HRA) and Leave Travel Allowance (LTA).

- Home loan interest on a self-occupied property under Section 24(b).

- Self-contribution to NPS under Section 80CCD(1) and 80CCD(1B).

- Section 80TTA and 80TTB deductions on interest income.

If you rely heavily on these, compare the regimes before choosing, since the old regime may save you more.

Surcharge and cess

For higher incomes, a surcharge applies on the tax: 10% above ₹50 lakh, 15% above ₹1 crore, and 25% above ₹2 crore. The new regime caps the surcharge at 25%, removing the 37% rate that applies in the old regime above ₹5 crore. A 4% Health and Education Cess is then added on the tax plus surcharge. Marginal relief also applies at the surcharge thresholds, so a small rise in income does not cause a disproportionate jump in tax.

Is the new regime right for you?

The new regime suits you if your income is up to ₹12.75 lakh, if you have few deductions, or if you prefer simple filing without locking money into tax-saving products. The old regime can still work out better if you have large deductions such as a home loan, HRA, full 80C investments, and health insurance. Add up your real deductions and compare both before you decide. Our old vs new regime guide shows the break-even point at each income level.

The new regime is the default under Section 115BAC. If you are salaried with no business income, you can choose the old regime each year while filing. If you have business income, you must file Form 10-IEA before the due date to opt for the old regime.

Frequently asked questions on new tax regime

What are the new tax regime slabs for FY 2025-26?

Nil up to ₹4 lakh, 5% from ₹4–8 lakh, 10% from ₹8–12 lakh, 15% from ₹12–16 lakh, 20% from ₹16–20 lakh, 25% from ₹20–24 lakh, and 30% above ₹24 lakh. A 4% cess applies on the final tax.

Is income up to ₹12 lakh really tax-free?

Yes. The Section 87A rebate of up to ₹60,000 makes taxable income up to ₹12 lakh tax-free for resident individuals. For the salaried, the ₹75,000 standard deduction lifts the tax-free salary to ₹12.75 lakh. The rebate does not cover capital gains.

What is marginal relief in the new regime?

If your taxable income is slightly above ₹12 lakh, marginal relief limits your tax to the amount by which your income exceeds ₹12 lakh, so a small rise in income does not cause a large jump in tax. It applies up to about ₹12.70 lakh of taxable income.

Which deductions are allowed in the new tax regime?

The standard deduction of ₹75,000, employer NPS contribution under Section 80CCD(2), the family pension deduction, the Agniveer Corpus Fund deduction, and interest on let-out property. Most others, including 80C, 80D, and HRA, are not allowed.

Is the new regime better than the old regime?

For most people with ordinary deductions, yes, because of the lower rates and the ₹12 lakh rebate. The old regime wins only when your total deductions are large. Compare both based on your actual deductions.

Do senior citizens get a higher exemption in the new regime?

No. The new regime applies a flat ₹4 lakh basic exemption to everyone. The higher age-based exemptions (₹3 lakh or ₹5 lakh) exist only in the old regime.

Sources and references

- Income Tax Department, e-filing portal — incometax.gov.in

- Income Tax Act, 1961 — Sections 115BAC, 87A, 80CCD(2), 80CCH, 24(b)

- Tax rates, rebate, and surcharge as provided through the Finance Acts of 2025 and 2026

Disclaimer

This guide is for general informational purposes and is accurate to the best of our knowledge as of June 2026. The tax figures are illustrative and assume the stated income and deduction levels; your actual tax depends on your full income, deductions, surcharge, and other factors. Tax laws can change, and individual circumstances vary. Please verify current details on incometax.gov.in and consult a qualified Chartered Accountant or tax advisor before acting on any information here.