Most Indians assume they are heading towards a comfortable retirement. Our latest retirement readiness survey across 1,218 individuals in 20+ Indian cities tells a quieter, more uncomfortable story. While 75.5% of respondents have no detailed retirement plan, the majority still feel confident about retiring on schedule. The biggest shortfall in 2026 has less to do with money and more to do with structure.

Awareness around retirement has arguably never been higher. EPF and NPS coverage has widened and online calculators are everywhere. Even so, only one in four respondents had anything close to a real plan. The rest were getting by on rough estimates, loose timelines and the hope that things would work themselves out.

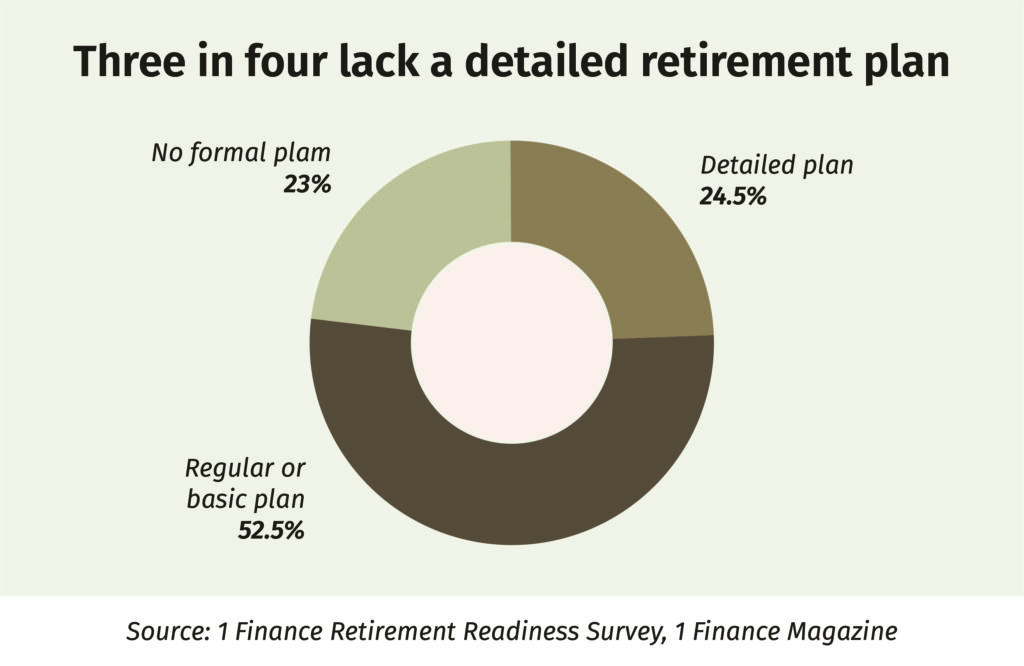

A primary survey conducted by 1 Finance, covering 1,218 individuals across 20+ Indian cities, found that 75.5% of respondents do not have a detailed retirement plan.

Complete survey findings: For full methodology and findings, kindly access the report here.

Three in four plans are running on guesswork

Only 24.5% of respondents reported having a detailed retirement plan. Another 52.5% had a rough or basic one and 23.0% had no formal plan at all. In practice, three out of four Indians approaching retirement are doing it without a blueprint. They know they should save and invest, but they have not sat down to work out how much they will actually need.

Confidence, though, tells a different story. Among those without a formal plan, 61.4% still describe themselves as somewhat or very confident about retiring on time. For a lot of people, that confidence rests on instinct rather than calculation.

A 3.6x gap between what people have and what they want

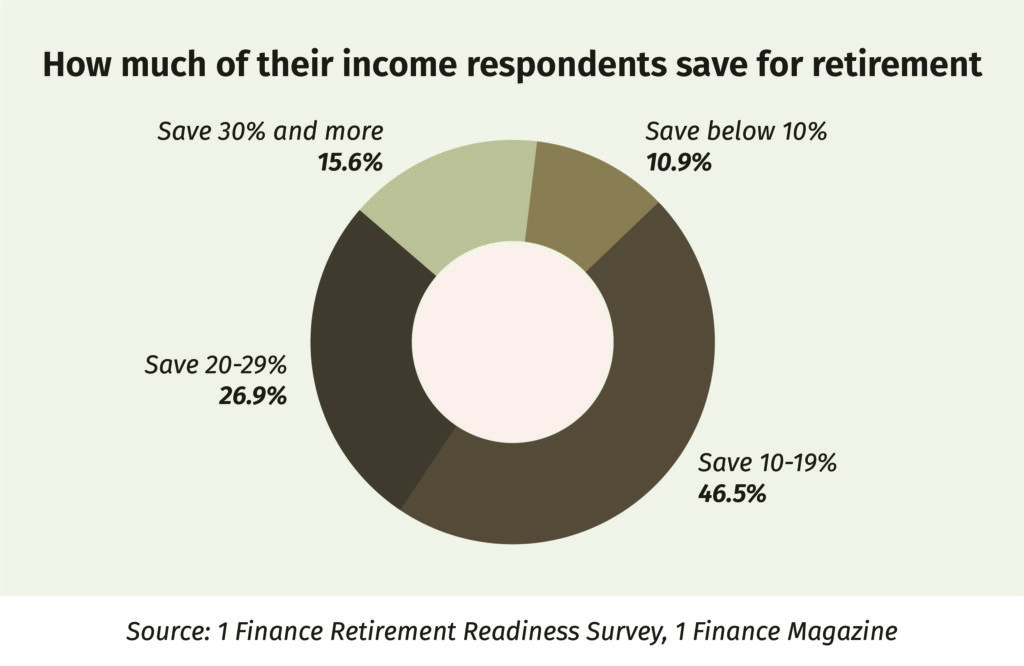

The math behind retirement planning in India in 2026 is sobering. The median respondent has built a corpus of ₹28 lakh but expects to retire with ₹1 crore, a gap of 3.6 times. Most are planning to bridge it in 10 to 20 years, often saving 10 to 19% of annual income, the bracket 46.5% of respondents fall into.

Compounding can do a lot of work in that window, but only if the starting numbers, return assumptions and timelines line up. The median respondent started planning at age 39, late enough that the runway is already shorter than most people assume.

A simple anchor helps here. For someone expecting to spend ₹50,000 a month after retirement in today’s value, that works out to ₹6 lakh a year. At a rough 25 to 30 times multiple, the required corpus would fall between ₹1.5 crore and ₹1.8 crore.

Without an anchor like this, retirement savings tend to drift towards whatever feels comfortable rather than what is actually required.

Metro vs non-metro: a 3.8x corpus target on 2.3x the income

One of the clearest divides in the survey is geographic. Metro respondents earn 2.3 times more than their non-metro peers (₹20.5 lakh vs ₹8.8 lakh in median annual income), but they are targeting retirement corpuses that are 3.8 times bigger (₹2 crore vs ₹52.5 lakh).

Two things are driving this. Metro respondents are pricing in higher lifestyle costs, urban inflation and longer life expectancy. Non-metro respondents lean more on owned housing, family support and lower projected expenses. Both views have their own logic and the gap between them is a useful reminder that retirement readiness is rarely a single figure. It shifts with location, lifestyle and whatever social safety net a household can realistically rely on.

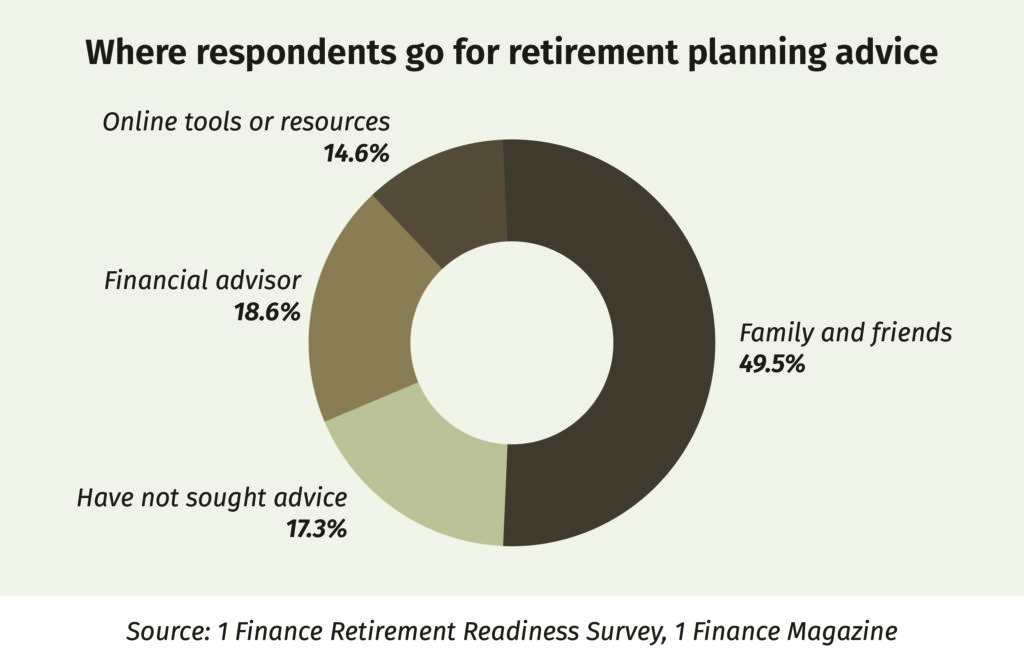

Family and friends, not advisors, drive most decisions

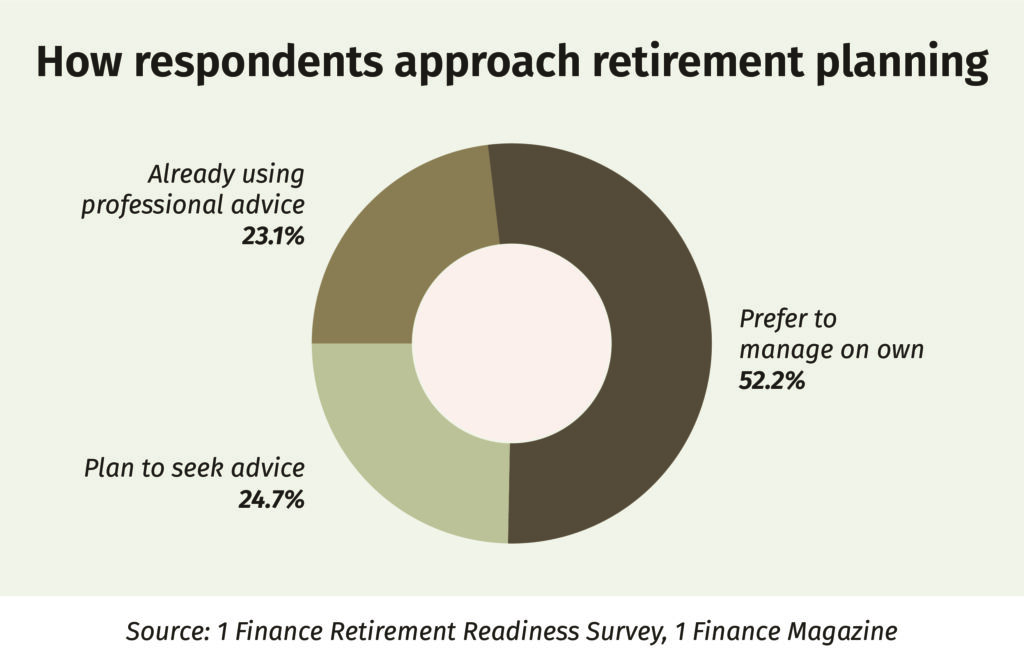

The advice picture is telling. A clear 76.9% of respondents plan for retirement without any professional help. Family and friends are the primary source for 49.5%, far ahead of financial advisors at 18.6% and online resources at 14.6%, while 17.3% have not sought advice from anyone.

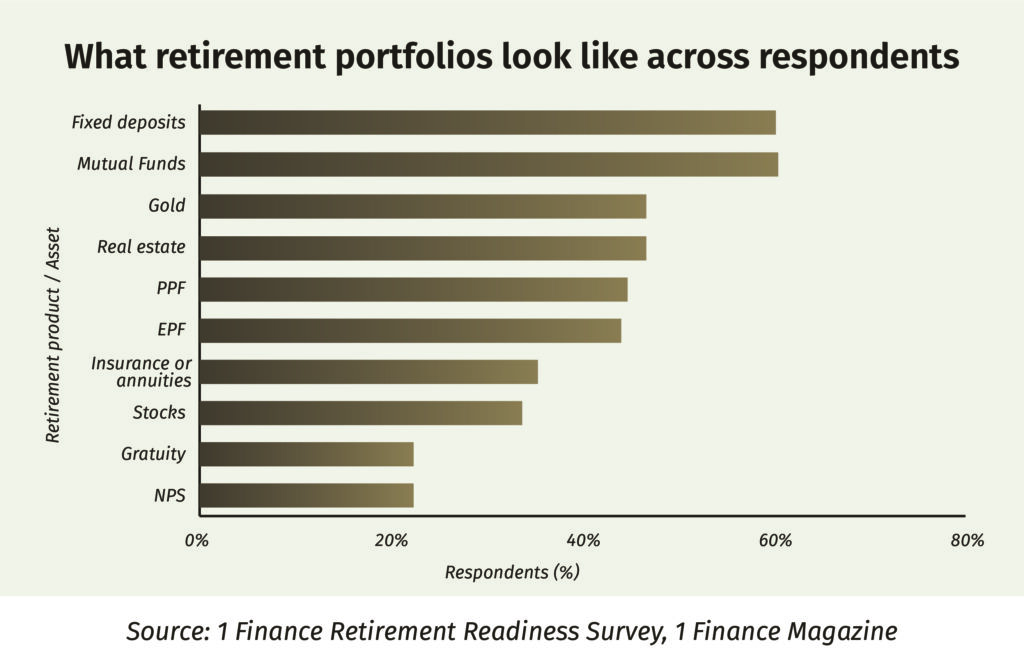

The asset mix is conservative too. FDs and mutual funds lead at 61.3% each, followed by gold and real estate at 47.3%. NPS and stocks, both built to outpace inflation over a 20-year horizon, sit near the bottom of the list at 22.7% and 34.3% respectively.

None of this is a criticism of family advice. The catch is that family members tend to anchor to their own retirement, which played out under a different inflation regime, a different cost-of-living curve and a different life expectancy. Any advice is only as reliable as the assumptions sitting behind it.

What a stronger plan looks like in practice

A handful of decisions over the next quarter tend to carry the most weight for any saver:

- Anchor the plan to a number. A target of 25 to 30 times expected annual post-retirement expenses gives savers a working figure to refine, rather than a vague sense of “enough”.

- Raise the savings rate in steps. Someone putting away 12% of income can move to 15% the next year and 18% the year after. Steady increases tend to hold better than dramatic one-off resolutions.

- Look beyond fixed deposits. A blend of equity mutual funds, NPS, PPF and EPF usually proves more durable over a 20-year horizon than FDs alone.

- Plan the withdrawal, not just the build-up. How a corpus is drawn down matters as much as how it is accumulated, yet most plans stop at the building stage.

- Get it onto a single page. Target corpus, monthly savings, asset allocation, expected retirement age and a five-year review date are enough to begin with.

For most Indians, the next gain in retirement readiness will come from clearer targets, disciplined savings increases and a written plan that can be reviewed regularly.

Disclaimer: This article is based on 1 Finance Magazine’s Retirement Readiness survey of 1,218 individuals across 20+ Indian cities. This article is for informational purposes only and must not be considered investment advice. Investors should consult with experts before making any investment decisions.