Indian households budget for weddings, school fees and EMIs with real discipline. The one thing they rarely budget for carries a far bigger financial cost: 84.8% have no will. The single document that decides what happens to a lifetime of savings is the one most families quietly skip. By 2026, estate planning in India has slipped below even retirement planning to become the country’s most ignored money habit.

Ask a salaried Indian in their forties what their financial plan looks like and you’ll hear about SIPs, term insurance, EPF and maybe a home loan. Ask about a will and the answer usually trails off. That silence sits at the heart of the problem.

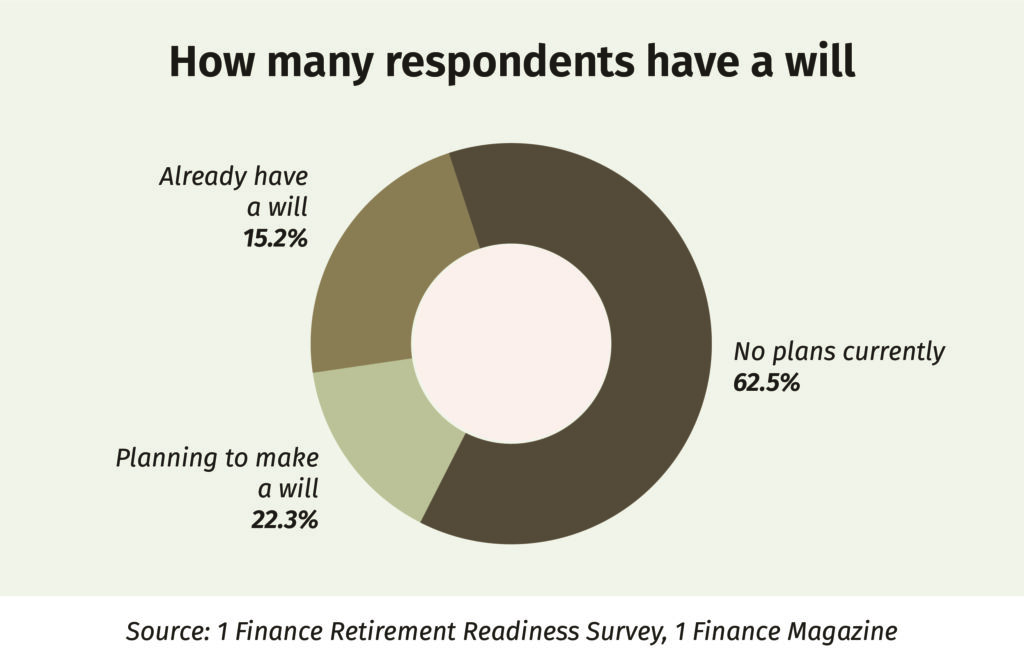

A primary survey conducted by 1 Finance, covering 1,218 individuals across 20+ Indian cities, found that only 15.2% of respondents have a will in place. 62.5% have no plans to make one at all.

Complete survey findings: For full methodology and findings, kindly access the report here.

Will planning in India lags even behind retirement planning

Put the numbers side by side and the gap is hard to miss. 75.5% of respondents have no detailed retirement plan and 84.8% have no will. Writing a will sits even lower on the priority list than retirement, and retirement planning in this country is already shaky.

The breakdown is sharper still:

- 15.2% already have a will

- 22.3% are planning to make one

- 62.5% have no plans to create a will at all

For most people, a will simply doesn’t feel urgent. It reads as a chore for the elderly or the unusually wealthy, with a quiet assumption underneath it that assets will pass down through the family on their own. They mostly don’t.

The inheritance paradox: expecting wealth, leaving none

The most uncomfortable finding in the survey is also the most telling. 79.8% of respondents who expect to receive an inheritance still don’t have a will of their own.

This is the paradox at the centre of many Indian households. The same person banking on wealth from the previous generation has done nothing to pass wealth to the next. Inheritance gets treated as a right that arrives on its own, while writing a will gets filed away as an inconvenience that can always wait.

That gap carries real risk. Undocumented wealth rarely passes cleanly. It gets contested, frozen or split over years of legal friction, however clear things seemed within the family.

Reduce overlap, minimise risk. Build your ideal portfolio

Let our Qualified Financial Advisors guide you

Book a free consultation

Book a free consultationWhy don’t Indian families talk about it?

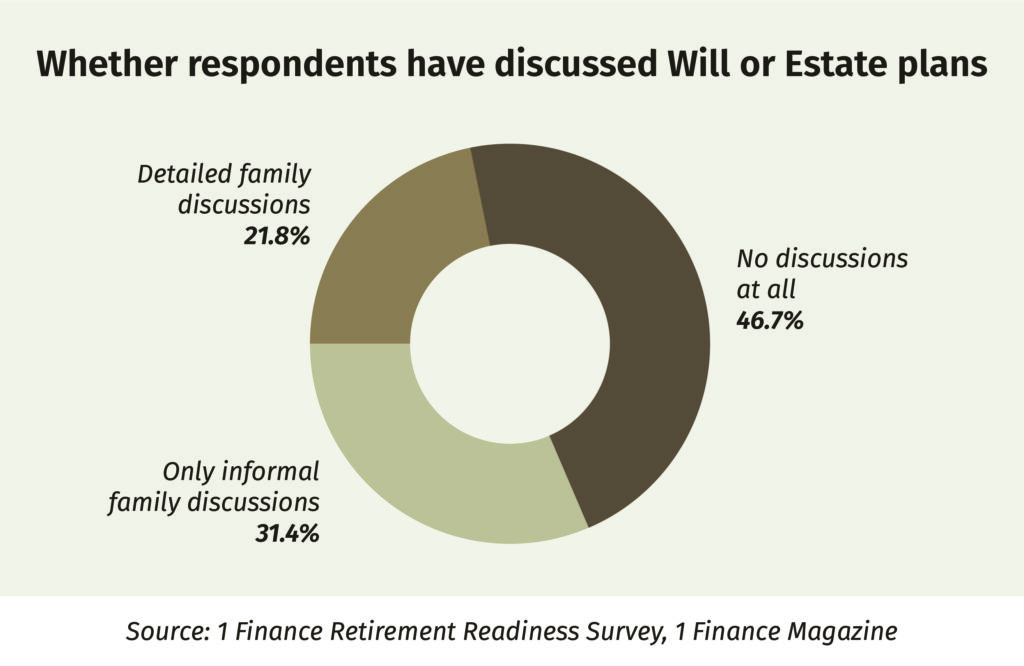

The conversation gap is as wide as the documentation gap.

- 46.7% of respondents have had no discussions at all on wills or inheritance

- 31.4% have had only informal family discussions

- 21.8% have had detailed family discussions

Barely one in five families has sat down to discuss it properly. Inheritance still feels culturally loaded, a topic that hints at mistrust or, worse, mortality. Short-term family harmony tends to win out over the long-term clarity that planning would bring.

The result is predictable. Families that don’t talk about it don’t document it. Families that don’t document it leave the courts to decide.

One thing does move families to act: having been burned before. Households that have lived through an inheritance dispute are almost twice as likely to have made or be planning a will as those that haven’t.

- No disputes: just 29.7% have a will or are planning one

- Minor disagreements: 54.1% have a will or are planning one

- Major disputes: 52.6% have a will or are planning one

The pattern is hard to miss. For most families, the push to document comes only after a painful experience, usually a relative’s estate that turned messy. The lesson tends to arrive a generation too late.

What skipping it actually costs?

The cost of weak planning tends to surface at the worst possible moment. The bank won’t release the locker because no nominee is on file. A flat is held jointly with no clarity on who inherits it. A mutual fund portfolio carries the wrong nominee on three folios and none on the other four. Each gap becomes months of paperwork, court dates and family conversations that should have happened a decade earlier. Nearly 66% of all civil cases pending in Indian courts are land and property disputes, most of them rooted in unclear inheritance, missing nominees, and undocumented succession. Two out of every three civil suits clogging the system are, at heart, estate-planning failures that ended up in a courtroom instead of a will.

The survey also found that 21.2% of respondents would lean on family and friends if their retirement money ran out. That safety net only holds if the family’s wealth can actually be transferred. Without a will, even modest assets can take years to release.

How to make a will in India without overthinking it?

Estate planning can sound intimidating, but the steps that matter most are small and easily done over a weekend.

- Start with a simple will: A handwritten will is legally valid in India, so a registered one is not a prerequisite to getting started. Elaborate legal language is not required. A clear list of assets, beneficiaries, and a named executor is enough.

- Update nominations across every account: bank accounts, EPF, NPS, mutual funds, demat, and insurance all need checking. A nominee receives the asset quickly; a will decides who finally owns it. Both are necessary.

- Keep one inheritance list: A single page covering every account, policy, property, and login, stored where a trusted family member can reach it. Most disputes begin because nobody knew what existed.

- Hold one structured family conversation a year: A casual chat works fine, as long as it happens.

- Register the will once assets are sizeable: Registration costs a few hundred rupees and meaningfully lowers the risk of a later challenge.

- Review it every three years: As lives change, the will should change with them.

Also Read: Estate planning services in India: A complete guide

Over the last two decades, the Indian middle class has taken to SIPs, term insurance, health cover and tax-saving instruments. A will is the obvious next habit and arguably the cheapest financial decision a household can make, since it protects every other one.

This blind spot has little to do with wealth and everything to do with willingness. Writing a will doesn’t bring death any closer; it just brings clarity sooner.

Disclaimer: This article is based on 1 Finance Magazine’s Retirement Readiness survey of 1,218 individuals across 20+ Indian cities. This article is for informational purposes only and must not be considered investment advice. Investors should consult with experts before making any investment decisions.