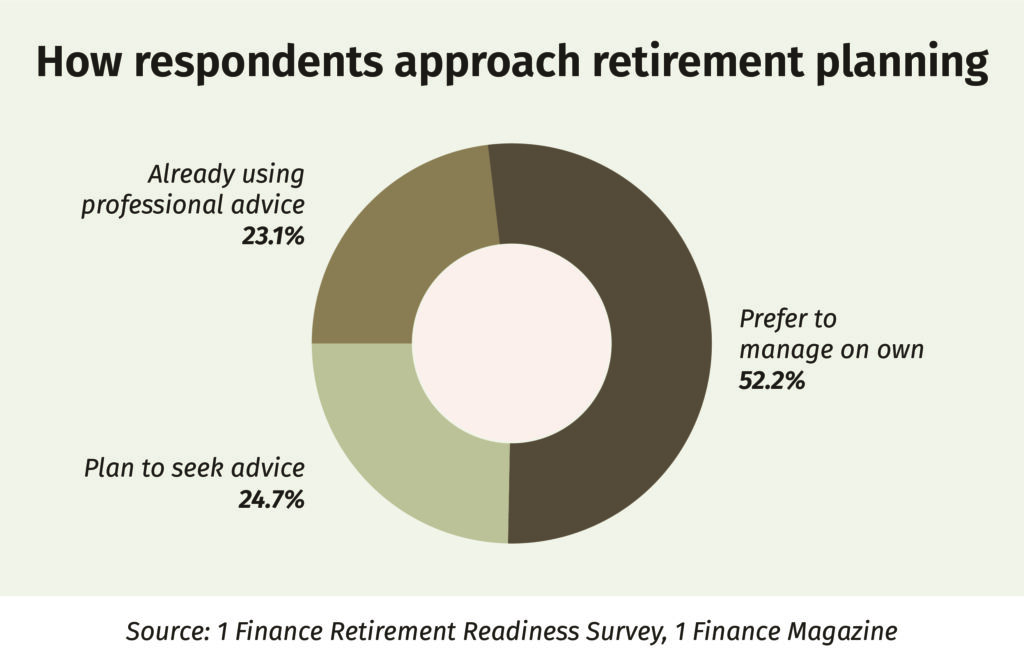

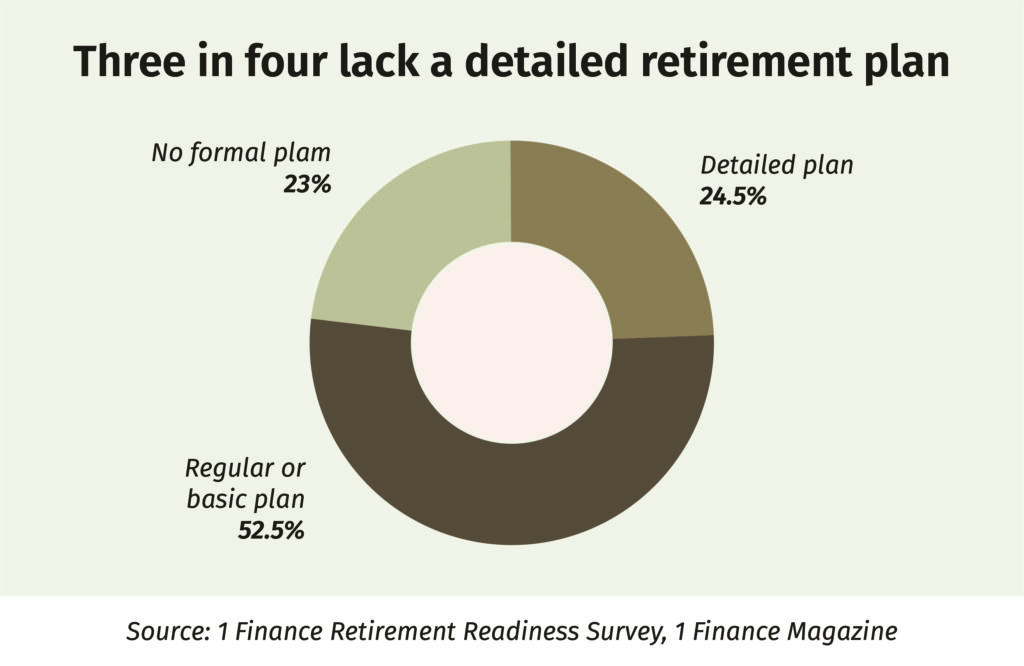

Among Indians planning for retirement, 76.9% don’t take professional advice, and 75.5% have no detailed plan. The overlap between those two figures is the real story here: skipping advice and skipping a plan tend to go hand in hand.

Whether to hire a financial advisor in India for retirement is usually framed as a cost-benefit sum: advisory fees on one side, the comfort of going it alone on the other. The latest retirement readiness survey points to a different cost altogether, the kind that builds up quietly when no one is around to ask the hard questions.

Complete survey findings: For full methodology and findings, kindly access the report here.

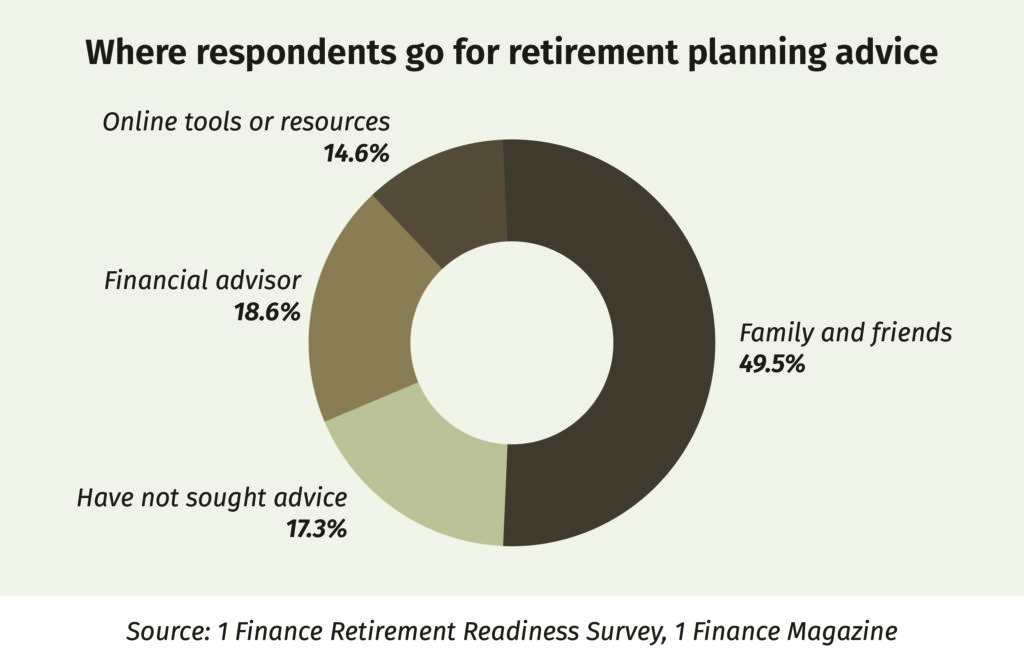

Where Indians actually go for retirement advice?

The picture is uneven. 52.2% of respondents prefer to manage their retirement planning on their own and 49.5% rely on family and friends as their primary source. Only 18.6% turn to a financial advisor, 17.3% haven’t sought advice from anyone at all and 14.6% use online tools or resources.

Put another way, family and friends are more than 2.6 times more likely than a qualified professional to be the primary retirement advisor in an Indian household.

Most family advice is given in good faith. The problem is the assumptions behind it. Parents and uncles who retired in the 2000s did so on a different inflation curve, a different healthcare cost base and a shorter life expectancy. Carrying that same playbook into 2026 quietly understates how much corpus a retiree today actually needs.

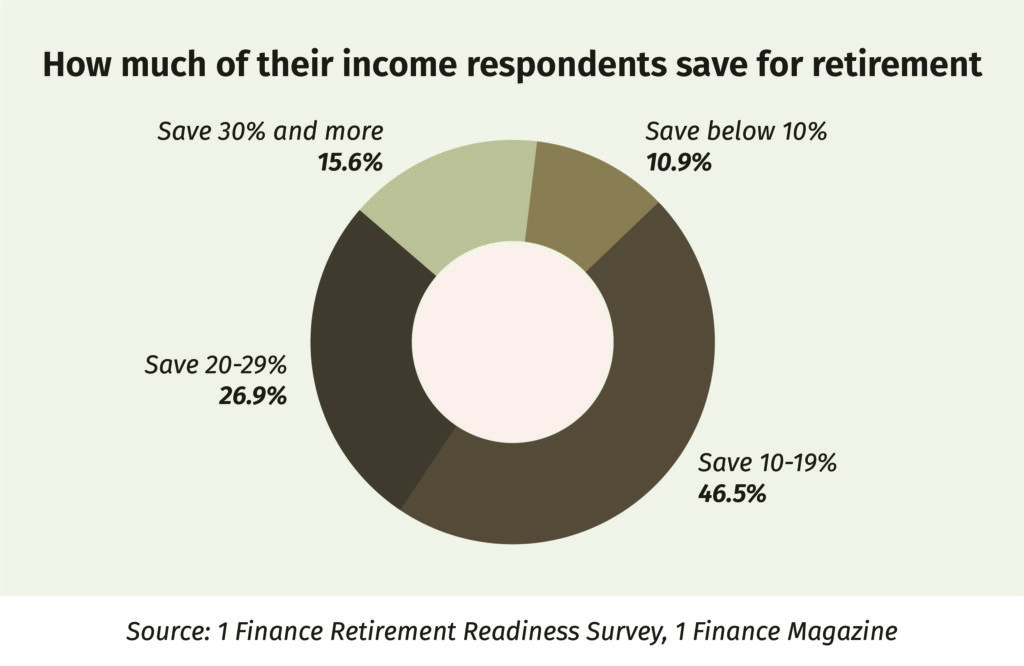

Where Do-It-Yourself plans fall short?

The numbers tell the story plainly. The median respondent has built a corpus of ₹28 lakh against an expected retirement target of ₹1 crore, a 3.6 times gap, with most giving themselves approximately two decades to close it.

46.5% of respondents save between 10% and 19% of their annual income for retirement, often with no clear corpus target behind the figure. Saving at a steady rate builds a good habit, but without a target number it doesn’t add up to a plan.

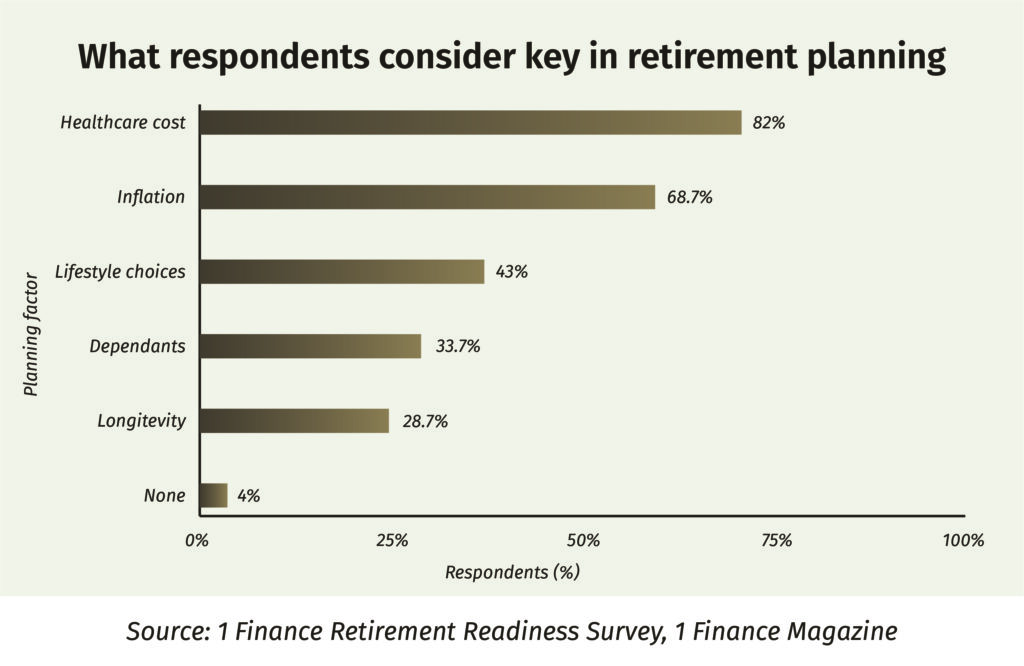

Meanwhile, 82.0% name healthcare costs as their biggest retirement worry and 68.7% flag inflation, the two variables that do-it-yourself plans tend to underestimate most.

When confidence outruns preparation?

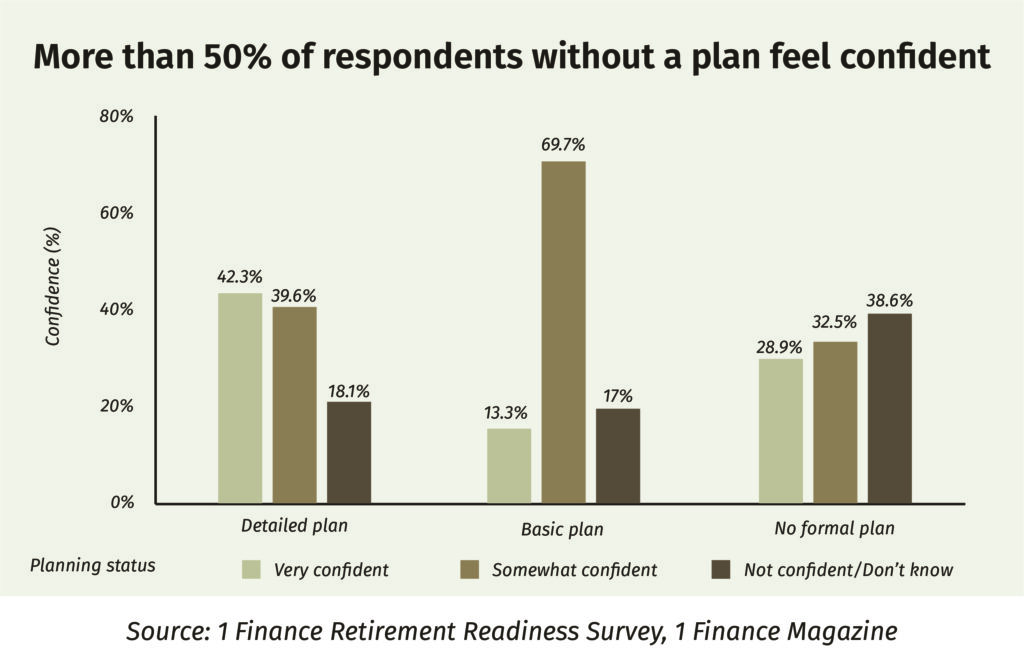

One finding in the survey is worth pausing on. Among respondents with no retirement plan at all, 61.4% still describe themselves as somewhat or very confident about retiring on time.

The breakdown is telling. 28.9% of those with no formal plan call themselves very confident, against just 13.3% of those who have a basic plan. The basic-plan group has done enough work to spot what’s still missing, which is exactly why their confidence is lower. Here, confidence runs in the opposite direction to preparation.

A good advisor’s first job is to turn that confidence into a number. Once an investor sees the gap between their assumed retirement expense, inflated forward, and their current savings trajectory, the question of whether to bring in help tends to answer itself.

Accumulation is only half the problem

Most self-managed retirement plans focus on building the corpus. Far fewer think about how to draw it down. The withdrawal phase comes with its own rules, including sequence-of-returns risk, equity allocation in retirement, tax-efficient drawdowns and healthcare buffers, and most online calculators leave them out entirely.

A SEBI-registered investment advisor typically covers five things a self-managed plan rarely does:

- Project a realistic post-retirement expense from the client’s actual lifestyle, rather than a generic 70%-of-current-income rule.

- Set a corpus target with inflation and healthcare assumptions that have been stress-tested.

- Design a withdrawal plan that is built to outlast the retiree, not just look funded on paper.

- Open up the family conversation around inheritance and a will, given that 84.8% of respondents have no will and 79.8% of those expecting an inheritance don’t either.

- Run an annual review so the plan keeps pace with actual returns, changing expenses and life events.

When is self-managing enough?

Hiring an advisor isn’t a universal requirement. An investor who has built a detailed plan, stress-tested it for inflation and longevity, diversified beyond fixed deposits, and reviews the portfolio with annual discipline may sit comfortably in the 24.5% who can self-manage well. For them, an occasional review from a qualified advisor is often enough, without the need for a full plan rebuild.

The test is straightforward. An investor who can write down their target corpus, expected monthly retirement expense in today’s money, assumed inflation rate and withdrawal strategy on a single page is probably fine on their own. For everyone else, the gap an advisor closes is wider than the fee they charge.

Reduce overlap, minimise risk. Build your ideal portfolio

Let our Qualified Financial Advisors guide you

Book a free consultation

Book a free consultation

How to hire well?

- A SEBI-registered investment advisor is the right starting point. Fee-only advisors carry a cleaner incentive structure than commission-linked distributors.

- A one-time plan review is the lowest-commitment way for an investor to see what their current approach is missing.

- The conversation should cover decumulation, not just accumulation. An advisor who talks only about SIPs and skips withdrawal strategy is solving half the problem.

- A written plan matters: target corpus, monthly savings, asset allocation, withdrawal plan, and estate plan. A single page is enough to begin with.

- Reviews should happen annually. A plan left untouched tends to drift within two to three years.

The real gap in retirement planning is the unchecked assumption: the question no one asks, the inflation number no one tests and the withdrawal plan that drifts off course every year. When used well, an advisor does more than just managing money. Their real job is to make sure good intentions do not get mistaken for a finished plan.

Disclaimer: This article is based on 1 Finance Magazine’s Retirement Readiness survey of 1,218 individuals across 20+ Indian cities. This article is for informational purposes only and must not be considered investment advice. Investors should consult with experts before making any investment decisions.