Indians living in metros earn 2.3 times more than their non-metro peers, but they are targeting retirement corpuses that are 3.8 times bigger. That single line, drawn from our survey of 1,218 individuals across 20+ Indian cities, captures one of the most under-discussed fault lines in retirement savings in India. The income gap is wide. The corpus ambition gap is much wider.

Retirement behaviour in India is often discussed as one national story. Look at the geography, though and two very different retirements appear: one engineered for ₹2 crore inside a metro, the other for ₹52.5 lakh outside it. Same country, same inflation, very different numbers.

A primary survey conducted by 1 Finance, covering 1,218 individuals across 20+ Indian cities, found a 3.8x gap in median target retirement corpus between metros and non-metros, against only a 2.3x gap in median annual income.

Complete survey findings: For full methodology and findings, kindly access the report here.

The 2.3x income gap, the 3.8x corpus gap

The numbers leave little room for interpretation. Metro respondents report a median annual income of ₹20.5 lakh against ₹8.8 lakh for non-metros, a 2.3x gap. The current corpus shows a smaller divide, at ₹35 lakh in metros versus ₹20.5 lakh in non-metros, a 1.8x gap.

Target corpus is where the two groups part ways. Metros are aiming for ₹2 crore and non-metros for ₹52.5 lakh, a 3.8x gap sitting on a 2.3x income difference. This is the part the national conversation tends to miss.

There are two ways to read it. Metros may be over-targeting because they have priced in lifestyle inflation, longer life expectancy and weaker family support. Or non-metros may be under-targeting because they are leaning on assumptions that might not hold for 25 years. In practice, both are probably true to some degree.

Reduce overlap, minimise risk. Build your ideal portfolio

Let our Qualified Financial Advisors guide you

Book a free consultation

Book a free consultation

Why ₹52.5 lakh only works on paper?

A ₹52.5 lakh corpus holds up only under a fairly narrow set of conditions: owned housing with no rent or rebuild costs, inflation behaving better than its long-run trend; and single-city living with no medical evacuation to a metro hospital, even where health insurance might otherwise step in.

The difficulty is that 82.0% of respondents flagged healthcare costs as their single biggest retirement concern, ahead of inflation at 68.7%. Healthcare also happens to be the category least bound by geography. A bypass surgery, a cancer protocol, or a year of structured diabetes care can cost almost the same in Ahmedabad as in Mumbai, and a ₹52.5 lakh corpus built for baseline living can be wiped out by one multi-year medical episode.

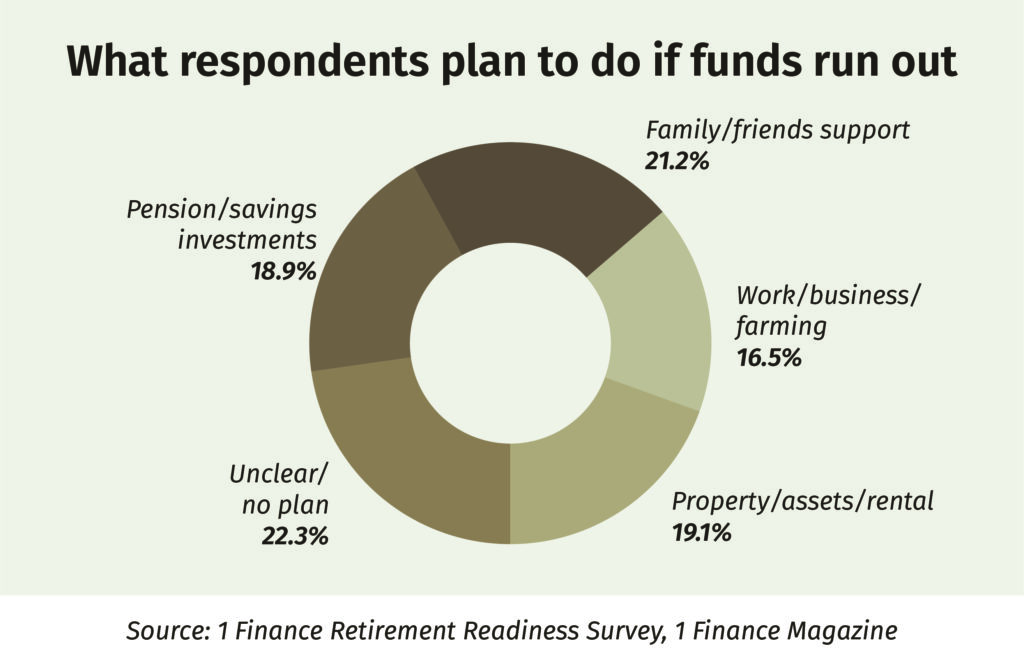

Family support is the other quiet assumption. Across the sample, 21.2% listed family or friends as their primary fallback if savings ran out. That dependency runs higher in non-metro households, even as the next generation increasingly migrates for work and may not be in a position to deliver on it.

What ₹2 crore actually pays for?

The metro target of ₹2 crore looks aspirational, but it is carrying more weight than it first appears. It absorbs 25 to 30 years of urban inflation in cities where rentals and groceries already move faster than CPI; private healthcare for two people through their 70s and 80s; a likely absence of co-residing children; and the cost of lifestyle continuity, from travel to hobbies to simply staying put.

Seen that way, the metro corpus is closer to a running cost than a luxury. It is what it takes to keep a metro household going through 20 to 25 retired years without forcing a change in how the family lives. The non-metro target of ₹52.5 lakh, drawn that way, looks less like a different lifestyle and more like a different set of assumptions about who picks up the slack.

Smaller incomes, steeper savings rates

The hard arithmetic of building a retirement corpus is that smaller incomes have to set aside a larger share of themselves to reach a comparable figure. A non-metro respondent earning ₹8.8 lakh and aiming for even ₹1 crore needs a meaningfully higher savings rate than a metro respondent on ₹20.5 lakh aiming for ₹2 crore, simply because the compounding base is smaller.

Yet 46.5% of all respondents save only 10 to 19% of annual income towards retirement, and non-metro behaviour tends to cluster at the lower end of that band. Factor in a later planning start, with a median age of 39 across the sample, and the runway compresses quickly.

Practical pointers for non-metro retirement planning

For households planning a retirement outside the metros, a handful of decisions move the needle out of proportion to the effort:

- Recalibrate the target: A non-metro number is worth stress-testing against a real shock. If a child’s wedding, a metro hospital admission, or an unplanned home rebuild in year five would break the corpus, then the target was set too low to begin with.

- Treat healthcare as a separate corpus: A dedicated sleeve of ₹15 to 25 lakh for medical emergencies, held on top of base savings, keeps a health event from collapsing the main plan.

- Buy comprehensive health insurance early: Premiums for comprehensive cover are far lower at 35 than at 55 and the alternative is facing uninsured medical exposure at 75.

- Diversify beyond FDs and gold: A blend of equity mutual funds, NPS, and PPF tends to prove more durable across two decades than fixed deposits alone, particularly on a smaller base where compounding has more work to do.

- Leave inheritance out of the plan: Any future inheritance is better treated as a bonus than as a line item. The corpus should be built as though it is never coming.

The metro versus non-metro retirement gap finally comes down to the quality of assumptions. Smaller cities may have lower living costs today, but healthcare inflation, migration, and weaker family support can quickly change the calculation.

Retirement in India will keep being told as a single story while it quietly splits into two, unless smaller cities start planning with the rigour the bigger ones already apply.

Disclaimer: This article is based on 1 Finance Magazine’s Retirement Readiness survey of 1,218 individuals across 20+ Indian cities. This article is for informational purposes only and must not be considered investment advice. Investors should consult with experts before making any investment decisions.