Indians overwhelmingly trust what they know. Our retirement readiness survey of 1,218 individuals across 20+ Indian cities found that fixed deposits and mutual funds tie for the top retirement choice at 61.3% each, while NPS, the product designed specifically for retirement, sits at the bottom at 22.7%.

The real takeaway is that FDs, mutual funds, and NPS play different roles in a retirement portfolio, while familiarity continues to drive most choices. Familiarity is doing most of the choosing, and the products built around retirement happen to be the ones people understand least.

Walk into any Indian household conversation about retirement and you will hear the same three letters more than any others: FD. Safe, predictable, trusted across generations. FDs clearly earn their place in a retirement portfolio. The real question is whether everything else in the mix is getting a fair look.

A survey conducted by 1 Finance covering 1,218 individuals across 20+ Indian cities found that FDs and mutual funds lead the retirement toolkit at 61.3% each, while NPS sits near the bottom at 22.7%.

Complete survey findings: For full methodology and findings, kindly access the report here.

Also read: Retirement planning in India 2026

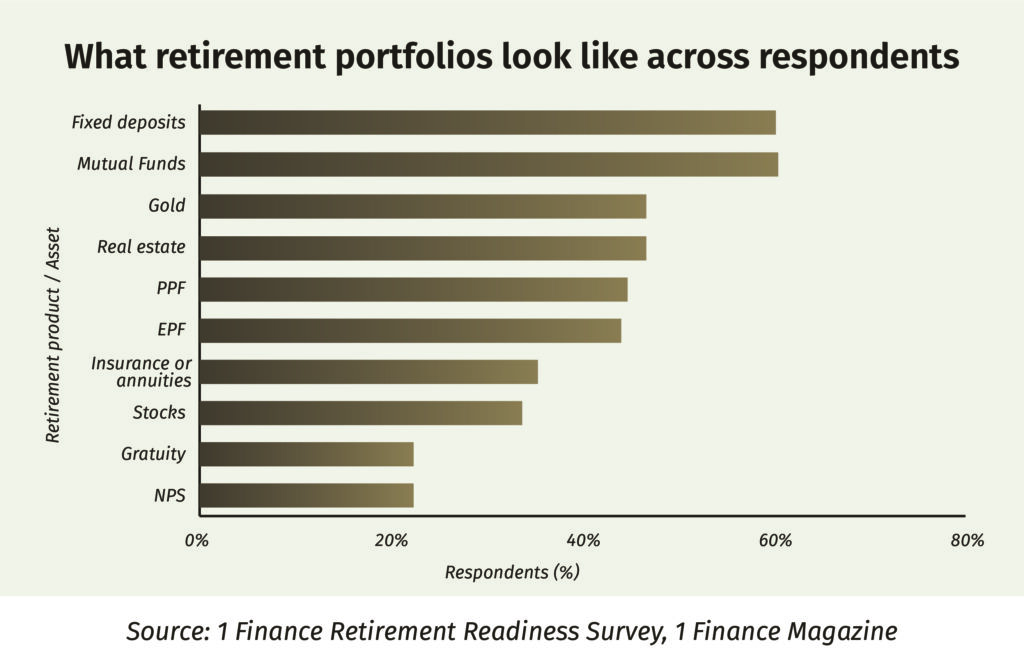

Where Indians are parking their money for retirement?

The survey asked respondents which products and assets they would consider for retirement.

The full picture:

- FDs: 61.3%

- Mutual Funds: 61.3%

- Gold: 47.3%

- Real Estate: 47.3%

- PPF: 45.3%

- EPF: 44.7%

- Insurance/annuities: 36.0%

- Stocks: 34.3%

- NPS: 22.7%

- Gratuity: 22.7%

Two patterns jump out. First, the familiar names dominate. FDs, gold, and real estate, the three pillars of traditional Indian household savings, all sit in the top four. Second, the instruments designed for long horizons, NPS and equity-focused products, sit in the bottom half. Most people, in other words, are building the toolkit from what they already know, with little room for products that might suit a specific goal.

How do the three core instruments actually compare?

The choice between the three comes down to risk appetite, time horizon, and the role each is meant to play in the overall asset allocation:

| Feature | Fixed Deposit | Mutual Funds (Equity) | NPS (Tier I) |

| Typical long-term return | 6 to 8% p.a. | 10 to 12% p.a. | 9 to 12% p.a. (auto-choice) |

| Risk profile | Lowest (DICGC up to ₹5 lakh) | High, market-linked | Moderate to high, market-linked |

| Lock-in | None (penalty on premature withdrawal) | None (3 years for ELSS). Exit-load may be applicable | Until age 60, premature withdrawal possible with certain restrictions |

| Key strength | Capital protection, predictable income | Long-term wealth creation, flexibility | Purpose-built for retirement, strong tax efficiency |

| Best suited for | Conservative investors, near-term needs, income certainty | Long-term investors who can absorb volatility | Disciplined savers comfortable with the lock-in until retirement |

There is no one-size-fits-all answer here. A 55-year-old close to retirement may rightly anchor in FDs for income certainty, while a 35-year-old has the runway to lean harder on equity mutual funds and NPS. What the survey really flags is the habit underneath the numbers: many Indians are choosing by default rather than building a deliberate mix.

Where each product earns its keep?

FDs offer something no other instrument quite manages in the Indian context: emotional certainty. The rate is known, the maturity is known, and the principal is protected. For a generation that has built wealth slowly and lived through several market cycles, that certainty carries real weight. Close to retirement, protecting capital and securing predictable income can matter as much as growth.

The catch is inflation. FD rates at major banks currently sit at 6 to 6.5% for popular tenures, while retail inflation averaged 4.6% in FY25 per MoSPI. That leaves a real return of roughly 1.5 to 2%, which is fine for the conservative slice of a corpus but hard to lean on as the sole engine.

Mutual funds tying with FDs at 61.3% is real progress, driven by SIPs, easier KYC and rising financial literacy. The open question is what sits inside that 61.3%. Which fund someone picks matters far less than the structure around it: how much equity is held, for how long and rebalanced on what rule. That layer of structure is exactly what the 75.5% of respondents without a detailed retirement plan are missing.

NPS at 22.7% is the most telling number in the mix. The product is built around retirement from the ground up, with tax benefits, long-horizon equity exposure, and a built-in annuity at exit. It lags for reasons that have little to do with how good it is. The lock-in until 60 feels long, the annuity at exit is widely misunderstood, and it is harder to explain in passing than an FD or an SIP. These are awareness gaps more than real weaknesses.

Practical pointers for a sharper retirement asset mix

- A sensible mix matches each product to its time horizon – FDs suit the conservative slice and near-term needs; equity mutual funds reward longer horizons that can absorb volatility.

- Equity exposure works best when it is structured – Splitting the retirement allocation between equity and debt on a written ratio, then rebalancing once a year, keeps it disciplined.

- NPS earns its place on tax efficiency – Even a 5 to 10% allocation captures the extra deduction available on the employer’s contribution under the new regime and adds structured equity exposure.

- PPF and EPF deserve to stay in the picture – Both already feature in roughly 45% of portfolios and remain among the most tax-efficient instruments available.

- Asset allocation is a review cycle, not a one-time call – Revisiting the mix every three years and turning more conservative as retirement nears keeps it aligned with the goal.

Better retirement outcomes rarely come down to one perfect product. They come from understanding what each instrument does well and combining them around a clear goal. That, more than any single fund choice, is where the next leap in Indian retirement readiness lies.

Disclaimer: This article is based on 1 Finance Magazine’s Retirement Readiness survey of 1,218 individuals across 20+ Indian cities. This article is for informational purposes only and must not be considered investment advice. Investors should consult with experts before making any investment decisions.

Reduce overlap, minimise risk. Build your ideal portfolio

Let our Qualified Financial Advisors guide you

Book a free consultation

Book a free consultation