Most Indians believe they are on track for retirement. The data suggests otherwise. Our survey of 1,218 individuals across 20+ Indian cities surfaced a quietly dangerous finding: 61.4% of respondents with no formal retirement plan still feel confident they will retire comfortably. For most households, the bigger risk is misjudged readiness: many feel prepared before testing their savings against inflation, healthcare costs and longevity.

Ask most Indians in their 40s and 50s how their retirement is shaping up and the answer is usually a calm “I think I’m okay.” It is one of the most consistent findings of the readiness study. The trouble is that confidence isn’t tracking preparation.

That gap shows up clearly in the numbers. A primary survey conducted by 1 Finance, covering 1,218 individuals across 20+ Indian cities, found that, among respondents with no formal plan, 61.4% still describe themselves as somewhat or very confident about retiring on time. This is the confidence gap that runs through the Indian middle class today.

Complete survey findings: For full methodology and findings, kindly access the report here.

The confidence-preparedness gap

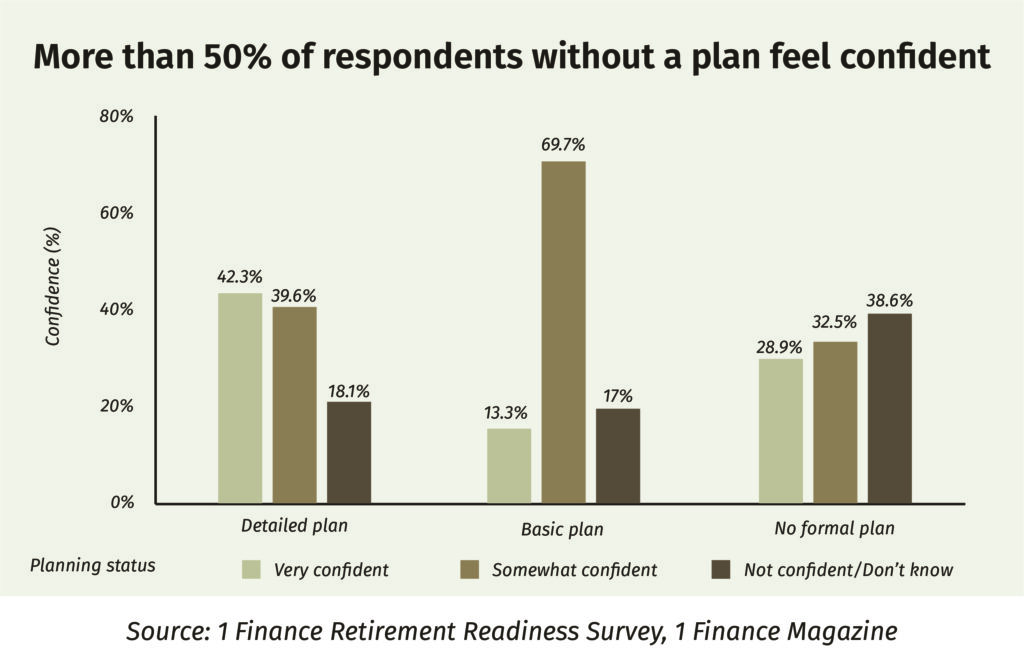

The numbers pull in two directions. 75.5% of respondents have no detailed retirement plan, yet most still feel prepared. Split by planning status, the gap is wider than it first appears.

Here’s what the graph reveals:

- 42.3% of respondents with a detailed plan say they are very confident

- 13.3% of those with only a basic plan say the same

- 28.9% of those with no formal plan still call themselves very confident

- Another 32.5% of the no-plan group say they are somewhat confident

Someone with no plan at all is more than twice as likely to call themselves very confident as someone who has built even a basic one. People with a basic plan have done just enough work to see what they still don’t know. People with no plan haven’t reached that point yet.

The most common retirement planning mistakes in India

A few recurring mistakes show up across cities and income brackets:

- Starting late: Respondents began planning at a median age of 39. That leaves about 21 years before a target retirement age of 60. Someone who starts at 30 gets nine more years of compounding and at 10 to 12% a year, those nine years can roughly double the final corpus.

- Saving without a target: 46.5% of respondents put only 10 to 19% of their annual income towards retirement. Whether that is enough depends entirely on the corpus they are aiming for and very few know what that number is.

- Treating retirement as a single number: The median current corpus stands at ₹28 lakh against a median target of ₹1 crore, a 3.6x gap. Yet few respondents have a year-by-year plan to close it.

- Going it alone: 76.9% of respondents take no professional help when planning for retirement. Among those who do seek advice, nearly half (49.5%) lean on family and friends as their main source of advice, well ahead of financial advisors at 18.6%.

- Quietly counting on working later: 64.3% expect to keep working after they retire. As a deliberate choice, that is perfectly reasonable. As a silent fallback for a corpus that falls short, it carries far more risk.

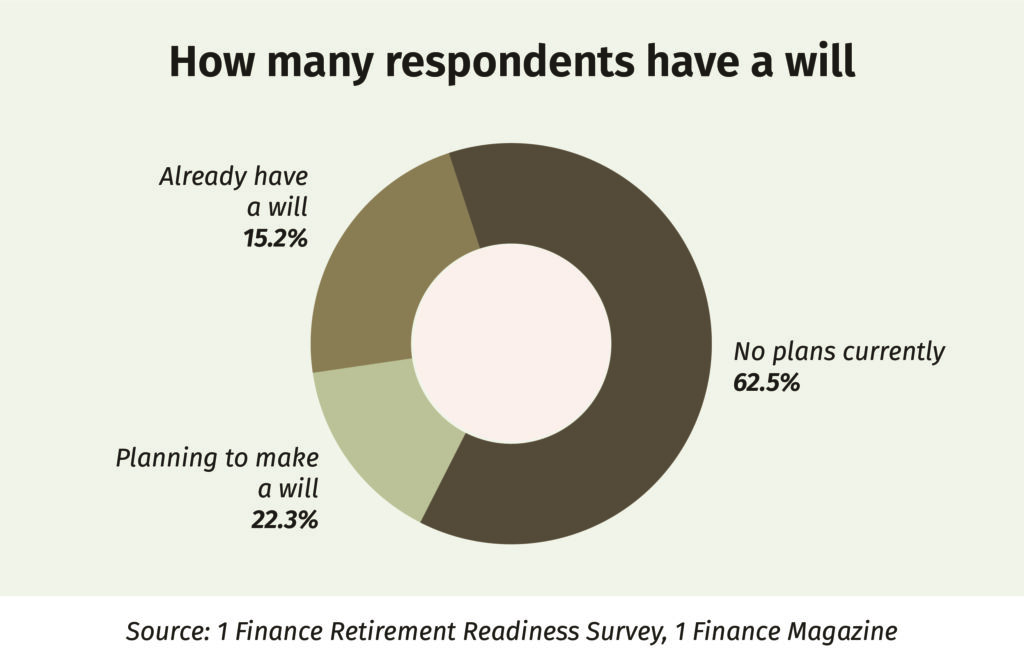

The estate planning blind spot

The confidence gap doesn’t stop at retirement. It carries straight into legacy planning. 84.8% of respondents have no will. 78.2% have never had a detailed inheritance conversation. And among those expecting an inheritance, 79.8% still have no will of their own.

That last figure is the most telling. Plenty of Indian households expect to inherit, while quietly assuming the previous generation has sorted out paperwork that, very often, was never created. The same confidence that pushes back retirement planning also pushes back the conversations and documents that protect family wealth across generations.

What happens when the money runs out

When asked what they would do if their retirement savings ran out, respondents split in a revealing way. 21.2% pointed to family and friends. 19.1% mentioned property or rental income. 18.9% expected to fall back on remaining pension, savings or investments. 16.5% planned to keep working in some form. The single largest group, 24.3%, had no clear answer at all.

Nearly a quarter of pre-retirees have never worked out what happens if the corpus runs short. A backup plan that exists only as a vague intention rarely holds up when it is actually needed.

Turning confidence into a real plan

What separates a confident guess from a real plan is behavioural discipline. A handful of habits consistently move people from one to the other.

- Calculation beats estimation: A sound plan starts by projecting monthly post-retirement expenses in today’s terms, then inflating them forward. Multiplying the inflated annual figure by 25 gives a reasonable minimum corpus. Setting that against current savings is usually where the real gap becomes visible.

- Assumptions need stress-testing: Advisors routinely ask what happens if income stops at 55, if returns come in 2% a year lower than expected, or if expenses climb faster than planned. A plan that survives those questions is far closer to a working plan than one that has never been tested.

- A will matters, however simple: A basic will costs little and takes a weekend and it spares families years of avoidable friction later.

- Inheritance works best as an annual conversation: It needn’t be formal, but it does need to happen at least once a year.

- An independent review is worth it: A single sitting with a SEBI-registered investment advisor, even a one-time plan review, is among the highest-return financial decisions a household can make.

The myth here isn’t really about saving too little. Plenty of Indians save diligently. What trips them up is saving without a target, without a withdrawal plan and without a realistic view of future costs. Confidence is a fine place to start. It has never, on its own, funded anyone’s retirement.

Disclaimer: This article is for informational purposes only and must not be considered investment advice. Investors should consult with experts before making any investment decisions.