Here’s How You Can Create Your Wedding Budget Without Compromisi...

A wedding is one of life’s most cherished moments, but it also comes with significa...

Book a free consulation

Book a free consulation

Get advice on investing, insurance, tax planning, loan management, etc, for free with a Qualifed Financial Advisor

Education is one of the few expenses most Indian families never question. It sits in a protected category, alongside food and healthcare, where the instinct is to spend first and figure out the finances later.

But the numbers behind that instinct deserve a closer look.

Research published as part of the 1 Finance Global Economic Outlook 2026 maps the total cost of schooling a child in India against what families actually earn. The gap between the two is wider than most parents expect, and it is growing every year.

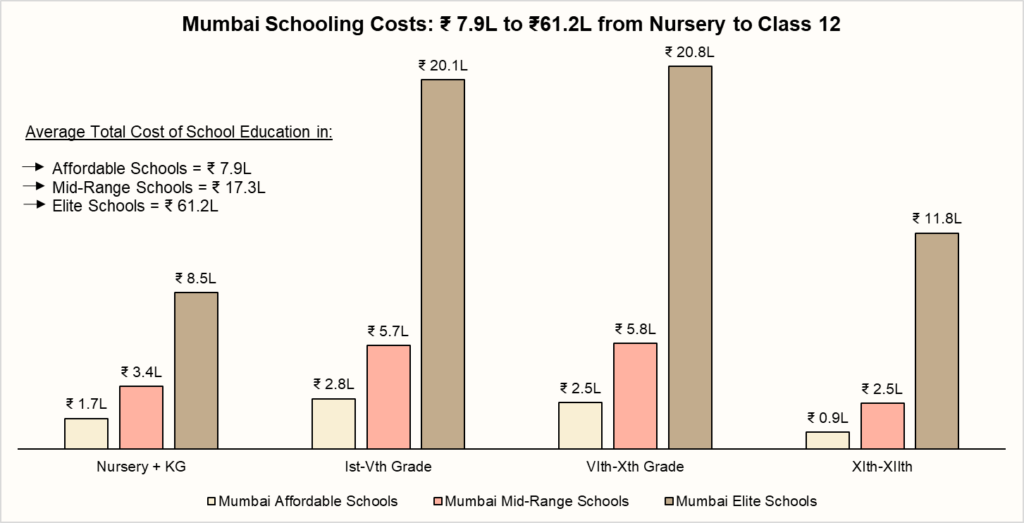

Let’s start with a straightforward question. How much does it cost to send one child through school, from nursery to class XII, in Mumbai?

The answer depends on the type of school. At an affordable school, the total comes to approximately ₹7.9 lakh. At a mid-range school, it rises to ₹17.3 lakh. And at an elite school, the number reaches ₹61.2 lakh.

Source: School Websites, 1 Finance Research

These figures cover tuition fees alone. They do not include transport, uniforms, books, admission fees, or extracurricular activities. The actual out-of-pocket cost for most families will be higher.

For a city where a large share of households earn between ₹4–6 lakh a year, even the mid-range figure of ₹17.3 lakh represents more than three years of a couple’s combined income spent on one child’s schooling.

Education loan boom: Rising cost of education in India and why you need a financial plan

One of the more striking findings in the research is the gap between what schools actually charge and what official inflation data suggests.

According to MoSPI’s Consumer Price Index data, education inflation in India runs at 3–6% annually. But the 1 Finance research found that schools across Mumbai, Delhi, Pune, Hyderabad, and Bangalore routinely raise fees by 10–12% per year. In several documented cases, the hikes were far steeper.

Schools typically raise fees across multiple grades all at once. They do not just target one specific class or cohort. As a result, education inflation compounds over several years. This increases the long-term financial burden on families significantly.

The table below shows this trend very clearly. It tracks the inflation rate of total tuition costs for 13 years (from Nursery to Grade XII).

| School | City | Previous Fee (Year) | Current Fee (Year) | Fee Hike (% per year) |

Nalanda Public School | Mumbai | ₹9,51,600 (2021-22) | ₹11,26,440 (2022-23) | 18% |

Pawar Public School | Mumbai | ₹10,23,750 (2024-25) | ₹12,03,020 (2025-26) | 18% |

Tagore International School | Delhi | ₹14,40,480 (2023-24) | ₹16,94,620 (2024-25) | 18% |

The British School | Delhi | ₹31,02,000 (2022-23) | ₹34,11,000 (2023-24) | 10% |

D.A.V. Public School | Pune | ₹5,49,000 (2023-24) | ₹7,78,200 (2024-25) | 42% |

Dhruv Global School | Pune | ₹11,13,196 (2022-23) | ₹15,16,668 (2023-24) | 36% |

The Gaudium School | Hyderabad | ₹52,00,000 (2023-24) | ₹69,80,000 (2024-25) | 34% |

Santinos Global School | Hyderabad | ₹9,63,500 (2024-25) | ₹11,32,700 (2025-26) | 18% |

| Vydehi School of Excellence | Bangalore | ₹14,49,420 (2023-24) | ₹15,94,500 (2024-25) | 10% |

| Dayananda Sagar Public School | Bangalore | ₹10,60,000 (2021-22) | ₹12,35,000 (2022-23) | 17% |

Source: School Websites, 1 Finance Research

The practical impact is significant. A family that budgets for a 5% annual increase, in line with official inflation data, will find itself underestimating the real cost of education by a wide margin within just a few years. Over a 15-year schooling period, that compounding gap can add up to lakhs of unplanned spending.

This is where the financial strain becomes clear.

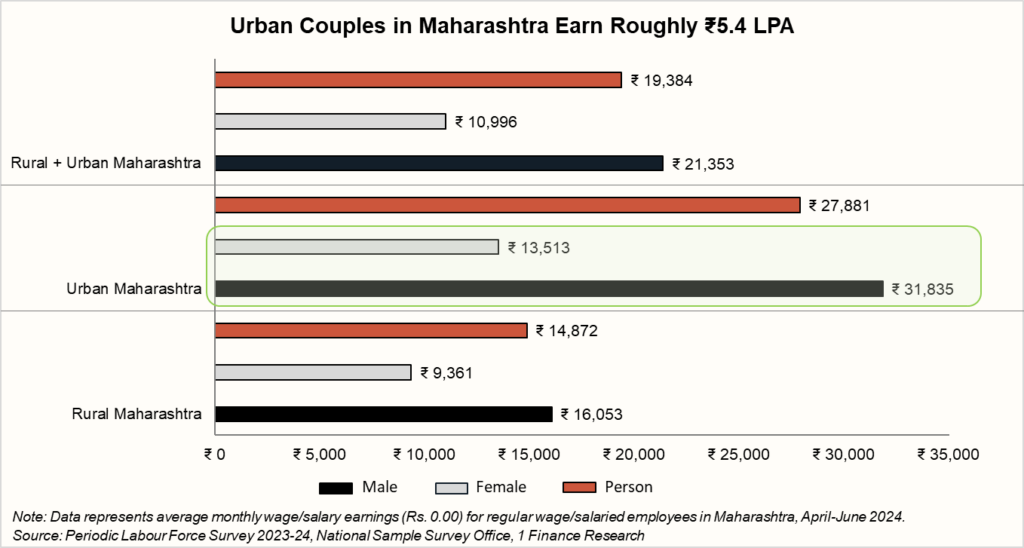

According to the Periodic Labour Force Survey 2023–24 published by the National Sample Survey Office, an urban couple in Maharashtra earns approximately ₹5.4 lakh per year, or about ₹45,348 per month combined.

Nursery fees alone at a mid-range school in Mumbai can cost around ₹1.13 lakh per year. That is over 20% of the couple’s total annual income, before any other expenses.

As the child moves to higher classes, fees rise further. And if a family has more than one child, the maths becomes even more difficult.

The core problem is straightforward. Fees rise 10–12% every year. Salaries, for most families, do not grow at the same pace. Each passing year widens the gap between what parents expected to pay and what they are actually paying. That shortfall has to come from somewhere, and it usually comes from retirement savings, emergency funds, or debt.

This is not just a Mumbai problem. The same dynamic plays out across Delhi, Pune, Hyderabad, and Bangalore, where school fee inflation consistently outpaces household income growth. The specific numbers vary by city, but the underlying pattern is the same.

This gap between official inflation data and actual education costs is not a minor statistical discrepancy. It has real consequences for how families plan their finances.

Most financial planning tools, SIP calculators, and education corpus estimators use CPI-based inflation assumptions of 5–6% for education. If the real rate is 10–12%, then a family saving for their child’s education at the “recommended” rate is likely to fall significantly short of the amount they will actually need.

Consider this. A degree that costs ₹80 lakh today could cost ₹1.6–2 crore in 10 years at these rates. Families relying on standard inflation assumptions to build their education fund may find themselves underprepared by 30–40% or more. That is not a rounding error. It is the difference between a fully funded education and a loan.

The problem is compounded by the fact that education spending is not discretionary in the way other expenses are. You cannot defer it, pause it, or reduce it mid-way without disrupting your child’s life. Once committed, the spending path is largely locked in, which makes accurate planning at the outset even more important.

This is not an argument against investing in your child’s education. Good schooling has real value. But it is an argument for treating education spending with the same financial rigour you would apply to any other major long-term commitment.

Here are a few things worth considering.

India’s education cost problem is not a one-time spike. It is a structural, compounding pressure that affects families across income levels and across cities.

Schools raise fees by 10–12% a year because they know parents won’t pull their children out mid-way. Official inflation data gives the impression that the situation is under control at 3–6%. And families, guided by that data, end up underestimating what they will actually need.

The fix is not to spend less on education. It is to plan for what education actually costs, with real numbers, realistic escalation assumptions, and a clear picture of how that spending fits into your overall financial life. Every school admission is a 15-year financial commitment. It deserves the same scrutiny you would give to buying a home or planning for retirement, because in many cases, it costs just as much.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Get advice on investing, insurance, tax planning, loan management, etc, for free with a Qualifed Financial Advisor

Explore

A wedding is one of life’s most cherished moments, but it also comes with significa...

Financial Well-Being focuses on long-term financial stability, while Financial Wellne...

“Hold fast to dreams, for if dreams die, life is a broken-winged bird that cann...