Book a free consultation

Book a free consultation

How to Create a Balanced Investment Portfolio in India

Are you looking to create a balanced investment portfolio that gives you the best of ...

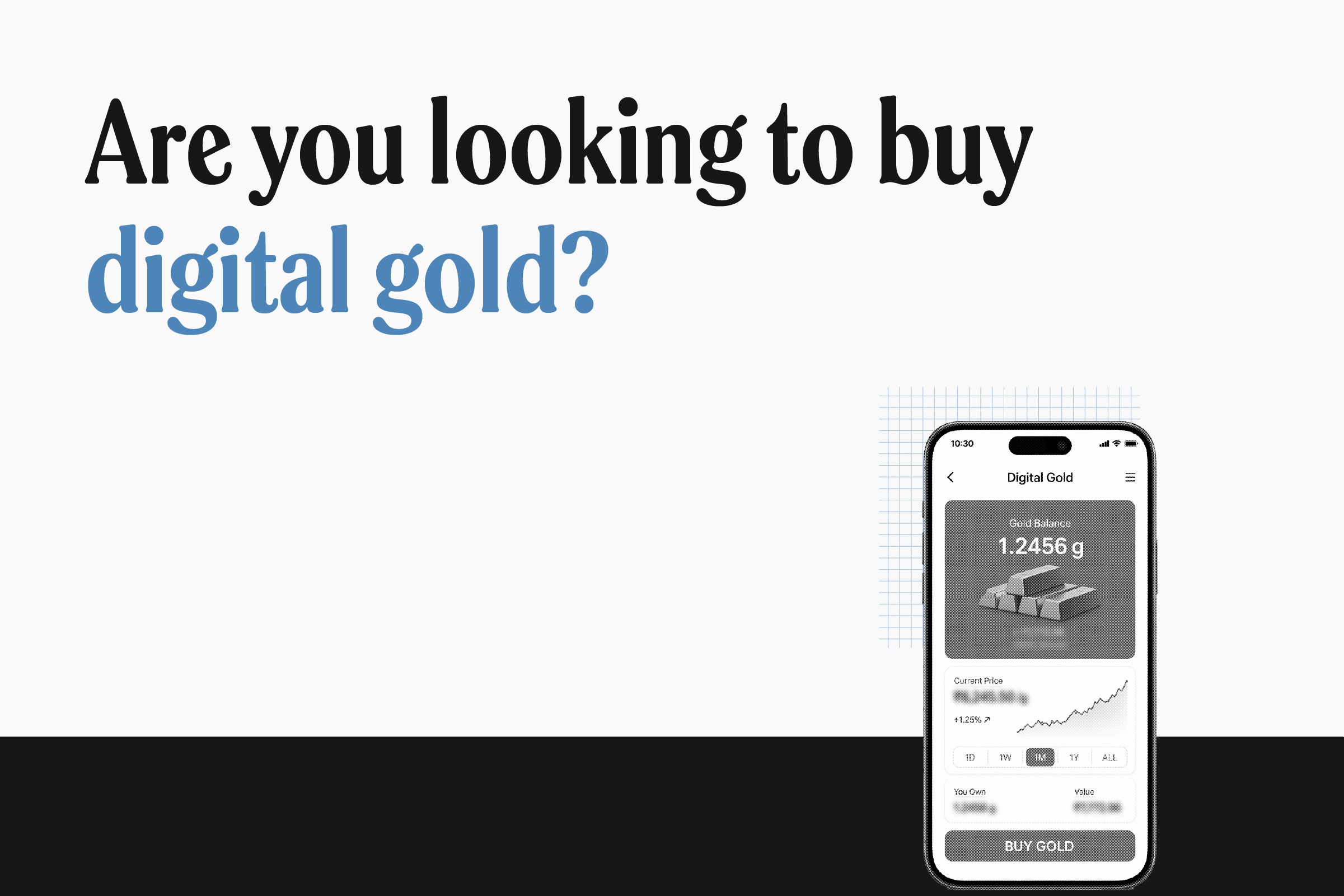

Digital gold has become one of the fastest-growing investment trends in India. You can buy it for as little as ₹1, store it without a locker, and sell it with a single tap. Many apps have made investing in digital gold look effortless, and millions of Indians are jumping in. In March 2026 alone, digital gold transactions on UPI crossed ₹3,171.96 crore.

So, if everyone is buying digital gold, it must be a good investment, right? Well, the straightforward answer is no.

In this article, we explain what digital gold is, how it is bought, and why you may be better off without it.

Digital gold is an online investment product that lets you buy small quantities of gold, starting from as little as ₹1, without physically owning it. When you purchase digital gold through an app, the platform’s custodian (typically MMTC-PAMP, SafeGold, or Augmont) buys an equivalent amount of physical gold and stores it in an insured vault in your name.

You receive a digital certificate of ownership. You can sell it back at live market prices or, once you’ve accumulated enough, redeem it as physical gold coins, bars, or jewellery.

If you want to know, here’s how the process works on most platforms.

Step 1: Choose a platform. In India there are many digital gold platforms from where you can buy digital gold. For example – PhonePe, Google Pay, Paytm, Tanishq Digital Gold, MMTC-PAMP, and Tickertape.

Step 2: Complete KYC. Register with your mobile number and verify your PAN card.

Step 3: Check the live gold price. Prices are updated in real time. The displayed price includes 3% GST. Platforms may lock the price for a couple of minutes, so you need to pay within that window.

Step 4: Enter your amount. You can invest by rupee value (say, ₹500) or by gram quantity (say, 0.05 grams). The minimum is usually ₹1.

Step 5: Pay via UPI, debit card, or net banking. The gold is credited to your account instantly, and you get a digital invoice.

Step 6: Hold, sell, or redeem. You can sell back anytime at the live buyback price. To redeem as physical gold, you typically pay making charges and delivery fees, with a minimum weight threshold of 0.5–1 gram.

So far, so convenient. But there are many problems (grave ones) which tells us why you shouldn’t invest in digital gold.

1. It is completely unregulated

On 8 November 2025, the Securities and Exchange Board of India (SEBI) issued a warning about digital gold. SEBI said it does not regulate digital gold. The same goes for RBI. This means digital gold falls completely outside the control of any major financial regulator in India.

2. No investor protection if the platform fails

Because digital gold is unregulated, the usual investor protections are simply not in place. In simple terms, if something goes wrong, like the company fails, there is fraud, or you cannot access your money, there is no official regulator responsible for protecting you or resolving your issue.

There are no standard rules for how your gold must be stored, no compulsory third-party audits to check if the gold actually exists, no requirement for companies to maintain strong financial backing, and no proper system for handling complaints.

Your only option would be slow, expensive civil litigation.

3. You lose 6% to 10% the moment you buy

When you buy digital gold, you don’t start from zero, you begin with a loss. Suppose you invest ₹1,000 through an app. First, 3% GST (₹30) is deducted immediately, leaving ₹970 effectively invested. Then, the platform includes a hidden markup of around 2–3% (say ₹30), which reduces the real value of your gold to about ₹940. On top of that, there is a buy-sell spread, meaning if you try to sell instantly, the platform will offer a lower price, say another 3% cut, bringing your value down to roughly ₹910.

So, even though you invested ₹1,000, you can only get back about ₹910 on day one, which is a loss of around 9%. Over time, if you hold the gold with providers like SafeGold, you may also have to pay storage fees after the free period ends, which further eats into your returns. This means gold prices must rise significantly just for you to break even. In simple terms, with digital gold, you don’t start at zero profit, you start in the negative.

4. Conversion to physical gold Is expensive and restrictive

If you want actual gold in your hand, you’ll pay making charges (for coins or jewellery), delivery fees, and you usually need a minimum of 0.5–1 gram before redemption is even allowed.

5. Storage has a time limit

Most platforms offer free storage for only 5 to 7 years. After that, you either pay annual storage fees, take physical delivery (with associated costs), or sell back at whatever spread exists at the time.

SEBI itself has pointed investors toward regulated alternatives. Both options give you exposure to gold prices without the regulatory vacuum of digital gold.

Gold ETFs (Exchange-Traded Funds)

Gold ETFs are generally a more reliable way to invest in gold because they are regulated by SEBI, which means there are strict rules around custody, audits, disclosures, and investor protection. Unlike digital gold, you don’t pay 3% GST when you invest, which immediately saves you a significant cost. The annual expense ratio is also much lower—typically around 0.5% to 1%, compared to the 6% or more hidden costs in digital gold. They are highly liquid, so you can buy and sell them on exchanges at real-time market prices during trading hours, and pricing is transparent since it’s determined by the market rather than set by a platform. Another advantage is that there is no storage limit—you can hold gold ETFs indefinitely without worrying about storage fees. Popular options in India include Nippon India ETF Gold BeES, HDFC Gold ETF, SBI Gold ETF, and ICICI Prudential Gold ETF, though you will need a demat and trading account to invest in them.

Gold mutual funds (Gold Fund of Funds)

A gold mutual fund invests primarily in gold ETFs, which means you still get exposure to gold prices but in a more convenient format. The biggest advantage is that you don’t need a demat account, you can invest directly through mutual fund platforms or apps. These funds are also regulated by SEBI, so you get the same level of investor protection as any other mutual fund. They are SIP-friendly, allowing you to start investing with as little as ₹500 per month and automate your contributions. Additionally, they are professionally managed, so the fund handles allocation and rebalancing for you. Well-known options include HDFC Gold Fund, SBI Gold Fund, Kotak Gold Fund, Axis Gold Fund, and ICICI Prudential Gold Fund.

The trade-off, however, is slightly higher costs, typically around 1.0% to 1.2% annually—since you are paying both the mutual fund’s fee and the underlying ETF cost. Some funds may also charge an exit load of 1–2% if you redeem your investment within the first year.

The bottom line

Digital gold is marketed as the simplest way to invest in gold, and it is convenient. But convenience comes at a steep price: high hidden costs, zero regulatory oversight, no investor protection, and full dependence on a private platform that could discontinue the product at any time.

Gold ETFs and Gold Mutual Funds deliver almost everything digital gold promises, fractional ownership, no physical storage, easy buying and selling, but with the one thing digital gold fundamentally lacks: SEBI regulation and the legal safeguards that come with it.

If you want gold in your portfolio, start a SIP in a Gold Mutual Fund or buy a Gold ETF. Skip the shiny app. Your future self will thank you.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Are you looking to create a balanced investment portfolio that gives you the best of ...

Index funds are investment vehicles designed to track the performance of a specific m...

From fixed income to stocks, mutual funds, real estate, and gold, there are several i...