Book a free consultation

Book a free consultation

Difference Between Belated ITR and Revised ITR

Introduction While most people around you might have successfully filed their Income ...

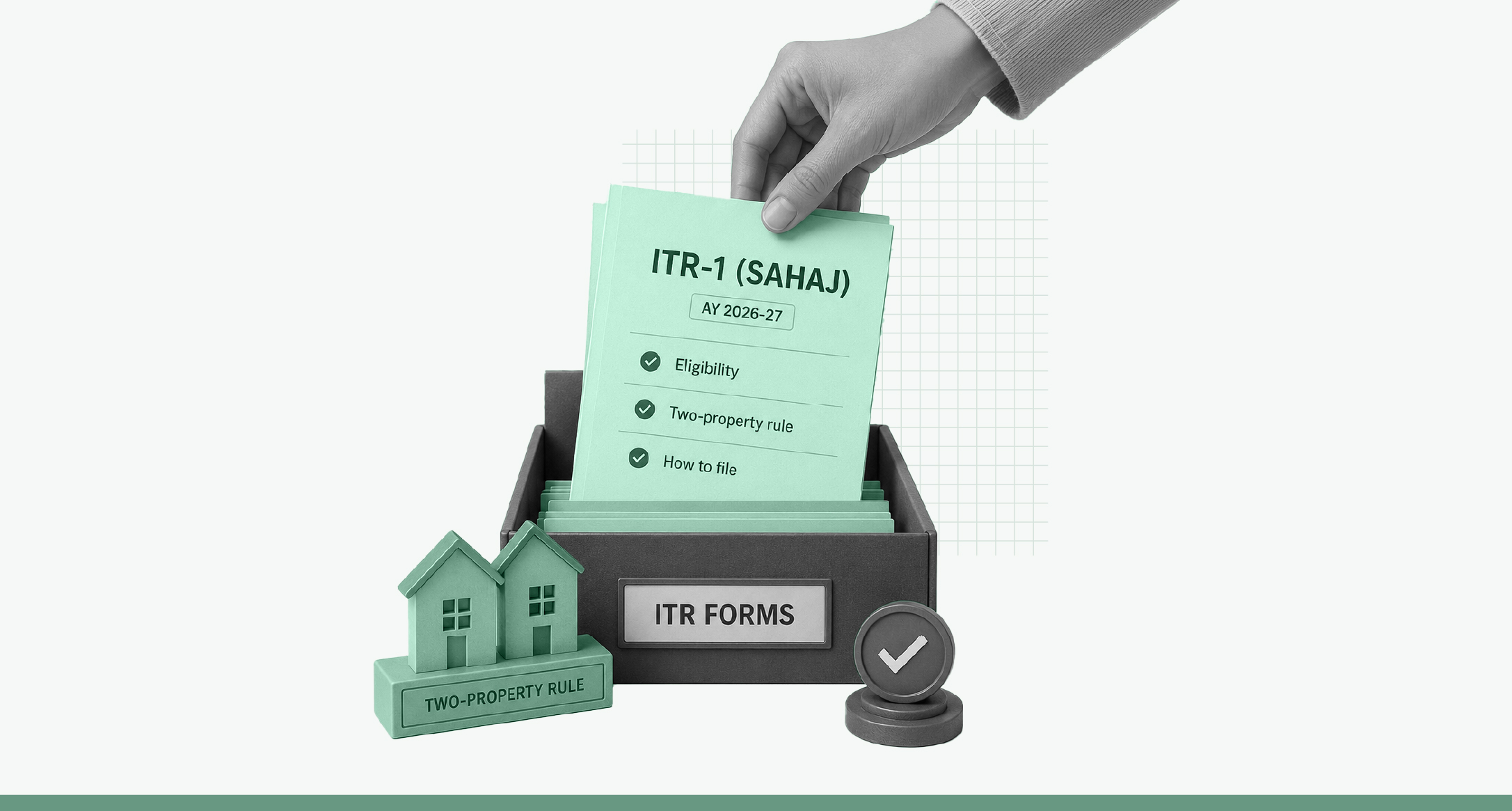

ITR-1, better known as Sahaj, is the most commonly used income tax return form in India. It is designed for salaried individuals and pensioners with relatively simple finances, it remains the default choice for crores of taxpayers.

The important update is, for Assessment Year (AY) 2026-27, ITR-1 has become significantly more useful. Two important changes now allow many taxpayers to continue using this simplified form instead of moving to the more complex ITR-2.

This guide explains what’s new, who can and cannot file ITR-1, the documents you’ll need, and how to file your return online.

Key takeaways

As per CBDT notification on 30 March 2026, taxpayers can use ITR-1 even for AY 2026-27, even if they have income from up to two house properties.

For example, you can file ITR-1 if you:

→ Live in one house and rent out another.

→ Own two rented properties.

Earlier, owning more than one house property generally meant filing ITR-2. However, the relaxation applies only up to two properties. If you own three or more house properties, you must file ITR-2 instead.

Any income or loss from the two eligible properties can be reported directly in ITR-1, provided you meet the other eligibility conditions for the form.

ITR filing 2026: The complete guide for FY 2025-26 (AY 2026-27)

Two genuine expansions make ITR-1 more flexible this year, both flowing from the ITR forms the CBDT notified on 30 March 2026:

Alongside these, the form has a few tightened compliance details for AY 2026-27, covered in the “What else has changed” section below.

You can file ITR-1 only if all of the following conditions are satisfied.

You must be a Resident and Ordinarily Resident (ROR) individual.

ITR-1 cannot be used by Non-Resident Indians (NRIs) and Resident but Not Ordinarily Resident (RNOR) taxpayers

Also your total income during the financial year must not exceed ₹50 lakh.

Your income should arise only from the following sources:

➜ Salary or pension income.

➜ Income from up to two house properties.

➜ Income from other sources, such as savings-account and fixed-deposit interest (excluding lottery winnings and income from racehorses).

➜ Long-term capital gains (LTCG) under Section 112A up to ₹1.25 lakh, with no capital losses to carry forward.

➜ Agricultural income up to ₹5,000.

If your finances fit within these conditions, ITR-1 is likely the correct return form.

You must use a different form (usually ITR-2, or ITR-3/ITR-4 if you have business income) if any of these apply to you:

➜ You have business or professional income.

➜ Your total income exceeds ₹50 lakh.

➜ You have any short-term capital gains, long-term capital gains above ₹1.25 lakh, or gains from property, gold, or other assets. (The ₹1.25 lakh exemption applies only to listed-equity LTCG.)

➜ You have capital losses that you want to carry forward or set off.

➜ You own more than two house properties.

➜ You have foreign income or foreign assets, or are claiming relief under a tax treaty.

➜ You are a director in a company or hold unlisted equity shares.

➜ You are an NRI (Non-Resident Indian) or RNOR (Resident but Not Ordinarily Resident).

➜ Your agricultural income exceeds ₹5,000.

If even one of these is true, filing ITR-1 would make your return defective under Section 139(9) — so move to the correct form instead.

ITR-1 vs ITR-2 vs ITR-3 vs ITR-4: Which ITR form should you file?

Keep these ready before you start:

➜ PAN and Aadhaar: Make sure they are linked, as an inoperative PAN can hold up your return and refund.

➜ Form 16 from your employer, showing your salary and the tax deducted at source (TDS).

➜ Form 26AS and the Annual Information Statement (AIS) / Taxpayer Information Summary (TIS).

➜ Bank account details and interest certificates for savings-account and fixed-deposit interest.

➜ Capital gains statement from your broker or mutual fund platform, if you have any listed-equity long-term capital gains (LTCG) to report.

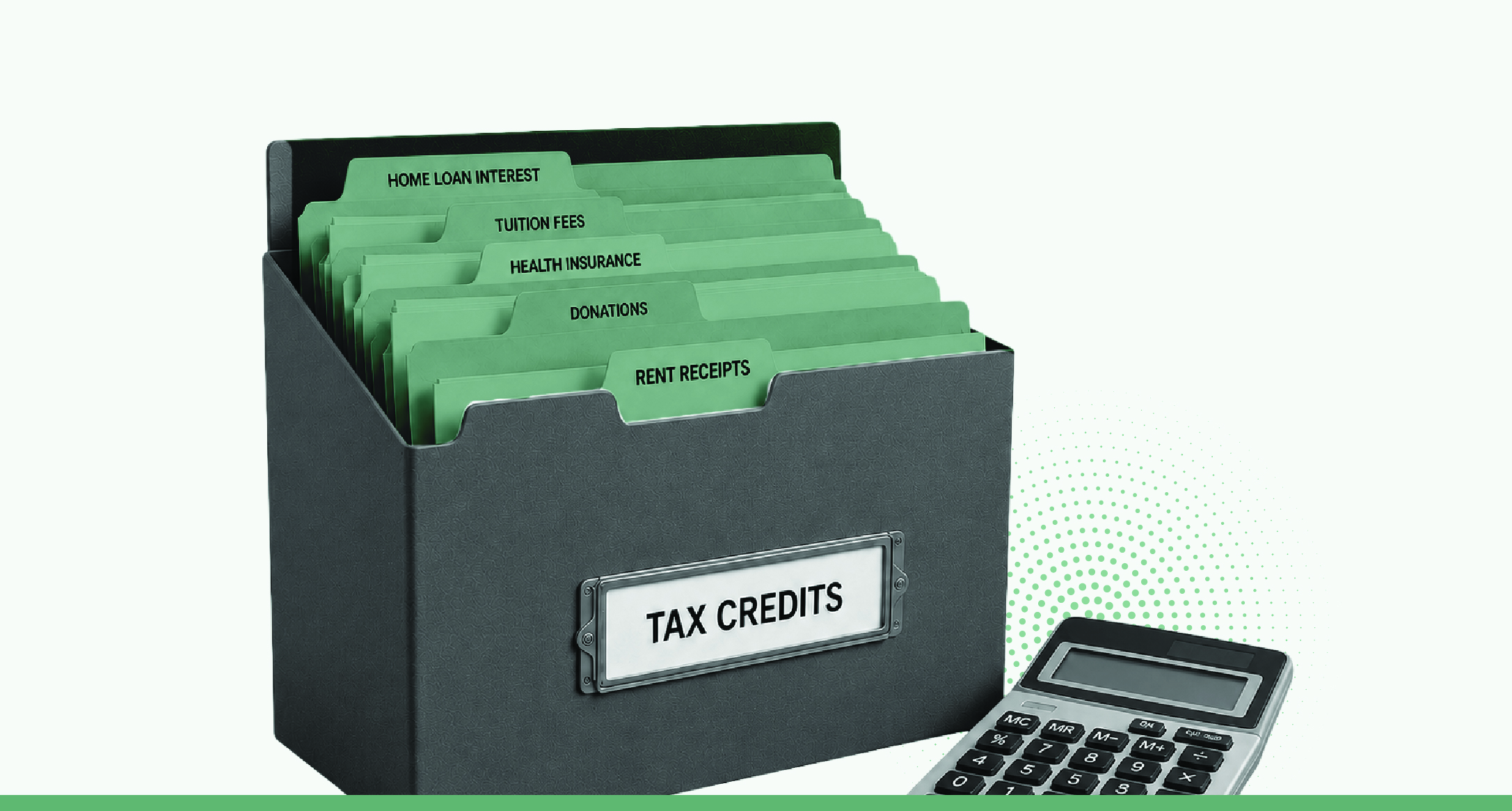

➜ Proof of deductions you plan to claim under the old tax regime, such as insurance premiums, Section 80C investments, rent receipts, and other eligible documents.

The Income Tax Department has enabled both online filing and the offline (Excel) utility for ITR-1 for AY 2026-27. Here’s the online route:

You can e-verify instantly using an Aadhaar OTP, net banking, or a bank or demat-based EVC. If you can’t verify online, post a signed ITR-V to the CPC in Bengaluru — but e-verification is faster and recommended.

Let our experts guide you

The due date for filing ITR-1 for AY 2026-27 is 31 July 2026. Miss it and you can file a belated return until 31 December 2026, but with a late fee under Section 234F (₹1,000 if income is up to ₹5 lakh, ₹5,000 above that), 1% monthly interest under Section 234A on any unpaid tax, and the risk of being locked into the new regime. Filing on time is the simplest way to avoid all of that.

What is ITR-1 (Sahaj)?

ITR-1, or Sahaj, is the simplest income tax return form for resident individuals with income from salary or pension, up to two house properties, interest income, agricultural income up to ₹5,000, and limited long-term capital gains under Section 112A.

Who can file ITR-1?

Resident individuals with total income up to ₹50 lakh can file ITR-1 if their income comes only from permitted sources such as salary, pension, up to two house properties, interest income, agricultural income up to ₹5,000, and eligible long-term capital gains under Section 112A.

Can I file ITR-1 if I own two houses?

Yes. From AY 2026-27, taxpayers can report income from up to two house properties in ITR-1. If you own more than two house properties, you will generally need to file ITR-2.

Can I report capital gains in ITR-1?

Yes, but only long-term capital gains under Section 112A from listed equity shares and equity mutual funds up to ₹1.25 lakh. Short-term capital gains, higher long-term gains, or gains from assets such as property or gold require ITR-2.

Is ITR-1 only for salaried people?

No. While ITR-1 is mainly used by salaried employees and pensioners, any resident individual who meets the eligibility conditions can file it.

What is the last date to file ITR-1 for AY 2026-27?

The due date for filing ITR-1 for AY 2026-27 is 31 July 2026 for taxpayers not subject to audit. Belated returns can generally be filed up to 31 December 2026 with applicable late fees and interest.

How do I file ITR-1 online?

Log in to the income-tax e-filing portal, select AY 2026-27 and ITR-1, verify the pre-filled information, choose your tax regime, pay any tax due, submit the return, and complete e-verification within 30 days.

Is ITR-1 or ITR-2 for salaried people?

Most salaried taxpayers can file ITR-1. However, you may need ITR-2 if you have income above ₹50 lakh, more than two house properties, foreign assets or income, certain capital gains, unlisted shares, or are a company director.

Who files ITR-1, ITR-2, ITR-3 and ITR-4?

What is the difference between ITR-1 and ITR-2?

ITR-1 is meant for resident individuals with relatively simple income and total income up to ₹50 lakh. ITR-2 is required for taxpayers with more complex income situations, such as larger capital gains, more than two house properties, foreign assets or income, or total income exceeding ₹50 lakh, but who do not have business income.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Introduction While most people around you might have successfully filed their Income ...

After ITR filing, an intimation notice arrives citing a tax credit mismatch, and the ...

When discussing personal finance, one topic we can’t overlook is income tax fil...