Book a free consultation

Book a free consultation

Understanding Tax Credits: How to Use Form 26AS and Annual Information...

Form 26AS and Annual information statement (AIS) display a comprehensive view of the ...

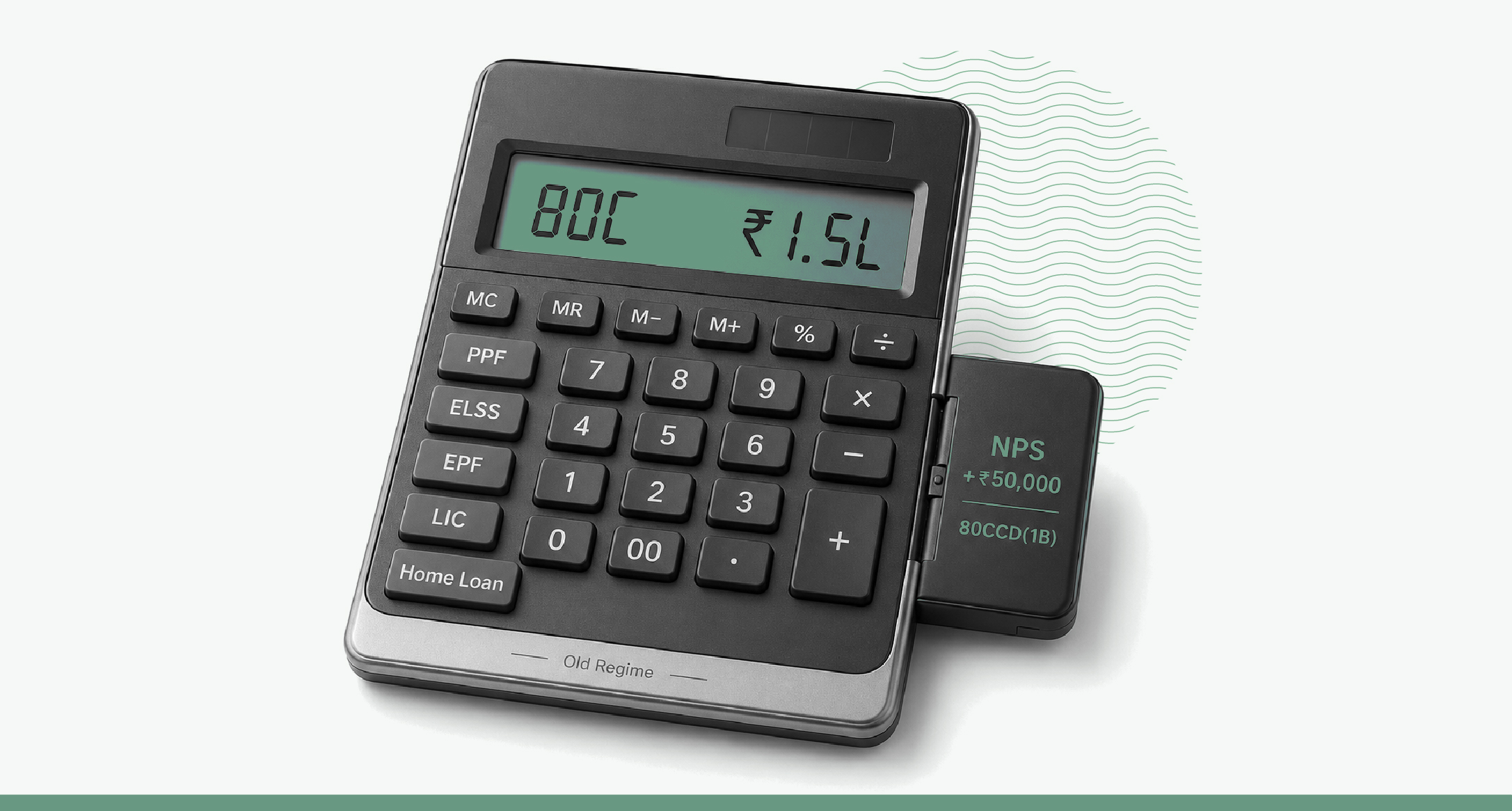

Section 80C is the most used tax-saving deduction in India. It lets individuals and Hindu Undivided Families (HUFs) reduce taxable income by up to ₹1.5 lakh a year by investing in or spending on specified items — PPF, ELSS, life insurance, EPF, home loan principal, and more. This guide explains the ₹1.5 lakh limit, gives the full list of what qualifies, and shows how to claim it. One thing to know up front: Section 80C is available only under the old tax regime.

For how this fits the regime choice, see our old vs new tax regime guide.

Key takeaways

Section 80C of the Income Tax Act, 1961 allows you to deduct certain investments and expenses from your gross total income, lowering the income on which you pay tax. The maximum deduction is ₹1.5 lakh in a financial year, and this limit has stayed the same since FY 2014-15 — Budget 2025 did not raise it.

Two basic conditions apply. The deduction is only for individuals and HUFs — companies and firms cannot claim it. And it is available only under the old regime. If you opt for the new tax regime, you cannot claim Section 80C at all.

This is the point people most often get wrong. The ₹1.5 lakh is not available separately for each investment. It is a single combined limit across everything you claim under Sections 80C, 80CCC, and 80CCD(1), together governed by Section 80CCE.

So if you put ₹1.5 lakh into PPF alone, you have used the full limit, and adding ELSS or insurance on top gives no extra deduction. If you spread money across several items — say ₹60,000 in PPF, ₹50,000 in ELSS, and ₹60,000 in insurance premiums — the total deduction is still capped at ₹1.5 lakh, not the ₹1.7 lakh you actually invested.

You can invest more than ₹1.5 lakh if you want to, but the deduction will not exceed ₹1.5 lakh.

Here are the main items that qualify, with their lock-in and how returns are taxed.

| Item | Type | Lock-in | Returns |

| Employee Provident Fund (EPF) | Retirement (own contribution) | Till retirement or job change | Interest tax-free within limits |

| Public Provident Fund (PPF) | Government savings | 15 years | Fully tax-free |

| Equity Linked Savings Scheme (ELSS) | Equity mutual fund | 3 years | LTCG taxed above ₹1.25 lakh |

| Life insurance premium | Insurance (self, spouse, children) | Policy term | Maturity usually exempt under 10(10D) |

| Sukanya Samriddhi Yojana | Girl child savings | Long-term | Fully tax-free |

| National Savings Certificate (NSC) | Government savings | 5 years | Interest taxable |

| 5-year tax-saving fixed deposit | Bank deposit | 5 years | Interest taxable |

| Senior Citizens Savings Scheme (SCSS) | Senior citizens | 5 years | Interest taxable |

| Unit Linked Insurance Plan (ULIP) | Insurance plus investment | 5 years | Maturity exempt if conditions met |

| Home loan principal repayment | Expense | Hold property 5 years | Not applicable |

| Stamp duty and registration charges | Expense (year of purchase) | One-time | Not applicable |

| Tuition fees (up to two children) | Expense | Not applicable | Not applicable |

| Self-contribution to NPS (Tier-I) | Retirement, under 80CCD(1) | Till age 60 | Partly taxable at maturity |

A recurring deposit does not qualify — only the 5-year tax-saving fixed deposit does. Tuition fees qualify only for full-time education in India, for up to two children.

Pay ₹2,499 upfront and get 100% cashback.

Filing will be done by Planmytax.ai, powered by 1 Finance

On top of the ₹1.5 lakh, you can claim an additional ₹50,000 for your own contribution to the National Pension System under Section 80CCD(1B). This is over and above the 80C limit, so a taxpayer can claim up to ₹2 lakh in total between 80C and this extra NPS deduction.

Separately, your employer’s contribution to NPS under Section 80CCD(2) is its own deduction, does not count against the ₹1.5 lakh, and is the one NPS deduction that remains available even in the new regime.

Not all 80C investments are taxed the same way when you withdraw. This matters as much as the deduction itself.

Some follow the EEE model — exempt at investment, on growth, and at withdrawal. PPF, EPF, Sukanya Samriddhi, and ELSS broadly fall here, so the maturity amount is tax-free (ELSS gains above ₹1.25 lakh are taxed as LTCG). Others follow the EET model — exempt going in but taxable at the end. Tax-saving FDs, NSC, and SCSS fall here, because the interest is taxable. So two investments that both give the same ₹1.5 lakh deduction can leave you with very different amounts after tax.

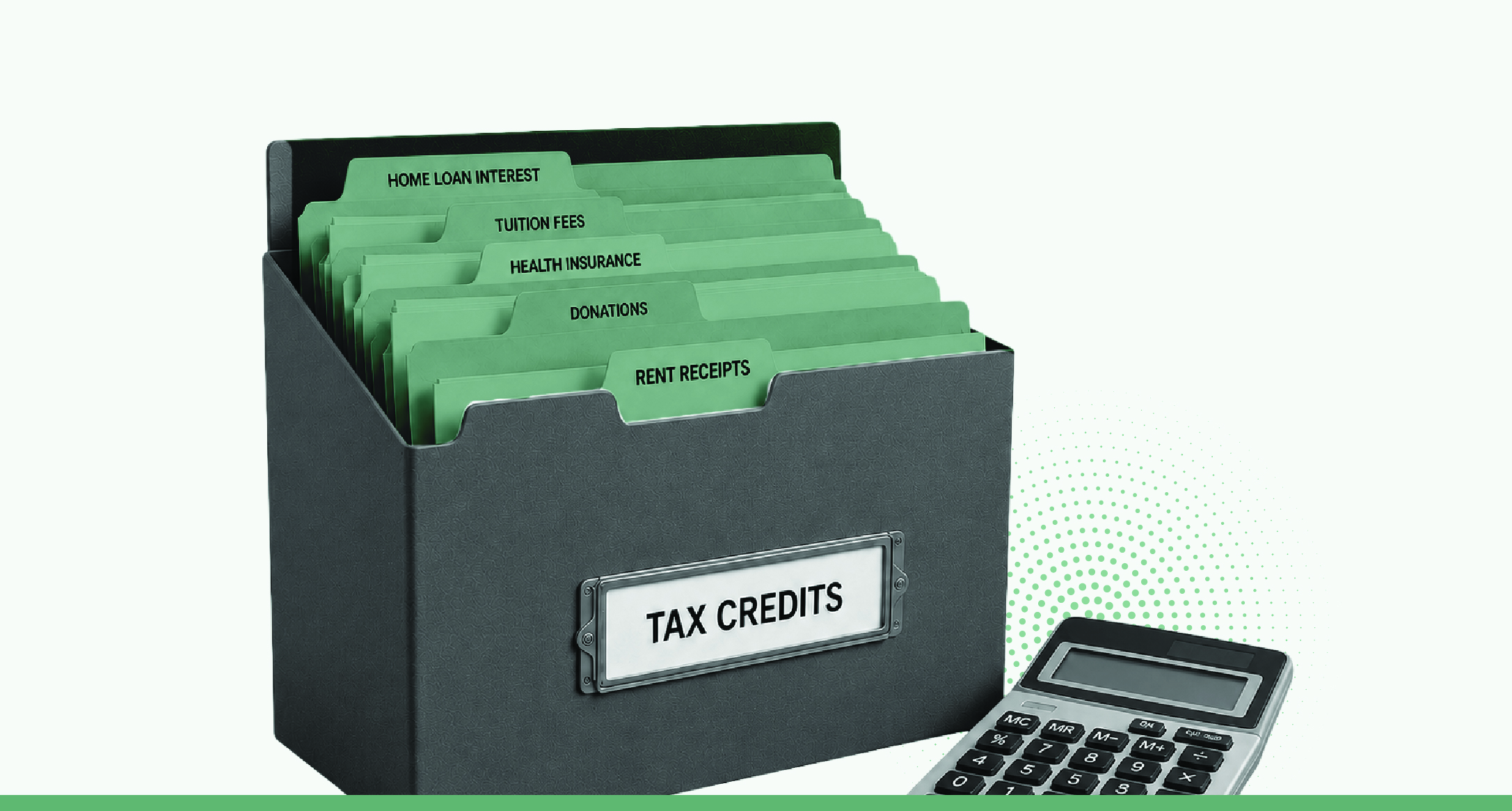

You claim 80C when you file your return, under Schedule VI-A, by entering the amounts you invested or spent. You do not attach proofs to the return, but you must keep them — premium receipts, PPF passbook, ELSS statement, the bank’s home loan certificate, NSC certificates, and fee receipts — in case of scrutiny.

The investment or expense must be made during the financial year, between 1 April 2025 and 31 March 2026 for FY 2025-26. If you did not declare your investments to your employer in time, you can still claim them while filing your return, as long as they were made before 31 March 2026.

Section 80C works best when the investment behind it suits your goals, not when you buy something only to fill the limit. A few practical points help.

First, check what you already use. For many salaried people, the EPF deducted from salary, a life insurance premium, and home loan principal repayment together fill much of the ₹1.5 lakh without any new investment. Adding more on top of a full limit gives no extra tax benefit.

Second, match the instrument to the goal. ELSS suits long-term growth, PPF and Sukanya Samriddhi suit safe long-term saving, and a tax-saving FD suits someone who wants certainty. Choosing by lock-in and risk, not just by the deduction, leaves you with money you actually want at the end.

Third, do not buy insurance you do not need just to save tax. A term policy you need for protection earns its 80C benefit honestly; a costly traditional policy bought only for the deduction often returns less than the tax it saves. Let the deduction follow a sound decision, not drive a poor one.

Pay ₹2,499 upfront and get 100% cashback.

Filing will be done by Planmytax.ai, powered by 1 Finance

What is Section 80C?

Section 80C is a deduction that lets individuals and HUFs reduce taxable income by up to ₹1.5 lakh a year through specified investments and expenses, such as PPF, ELSS, life insurance, EPF, and home loan principal. It is available only under the old tax regime.

What is the 80C deduction limit for FY 2025-26?

₹1.5 lakh per financial year. It is a combined limit across all eligible items under Sections 80C, 80CCC, and 80CCD(1), and it has not changed since FY 2014-15.

What comes under Section 80C?

PPF, EPF, ELSS, life insurance premiums, NSC, 5-year tax-saving FDs, Sukanya Samriddhi Yojana, Senior Citizens Savings Scheme, ULIPs, home loan principal repayment, stamp duty in the year of purchase, and tuition fees for up to two children.

Is Section 80C available in the new tax regime?

No. Section 80C is available only under the old regime. If you choose the new regime, you cannot claim it. The one related deduction that survives in the new regime is the employer’s NPS contribution under Section 80CCD(2).

Can I claim more than ₹1.5 lakh under 80C?

The 80C deduction is capped at ₹1.5 lakh even if you invest more. However, you can claim an extra ₹50,000 for NPS under Section 80CCD(1B), taking the combined deduction up to ₹2 lakh.

Can I claim 80C if I didn’t submit proof to my employer?

Yes. You can claim eligible 80C investments while filing your return even if you did not declare them to your employer, as long as they were made before 31 March 2026.

This guide is for general informational purposes and is accurate to the best of our knowledge as of June 2026. Tax laws, limits, and the tax treatment of investments can change, and individual circumstances vary. Please verify current details on incometax.gov.in and consult a qualified Chartered Accountant or financial advisor before acting on any information here.

The views in the article /blog are personal and that of the author. The idea is to create awareness and not intended to provide any product recommendations.

Form 26AS and Annual information statement (AIS) display a comprehensive view of the ...

After ITR filing, an intimation notice arrives citing a tax credit mismatch, and the ...

Whether you’re applying for a bank loan or filing a visa application, income tax re...