Popular searches

Get to know your policy better

Product scoring may vary based on gender, age, policy tenure and sum assured.

Gender

Age Group

The lowest age in the selected range is considered for price evaluation (e.g., 25 - 29)

The lowest age in the selected range is considered for price evaluation (e.g., 25 - 29)

Sum Assured

India’s ₹2.2 Lakh Crore in Forgotten Wealth

As children, we all stashed pocket money in our piggy banks, but in the process of growing up and earning adult money, we forgot about them and the money we carefully saved.

Now imagine this happening to lakhs of Indians with their hard-earned money, except on a much larger scale and with bank deposits, insurance policies and investment portfolios in place of piggy banks. Amidst the routines of daily life, it is easy to lose track of investments, particularly those made before widespread digitalisation.

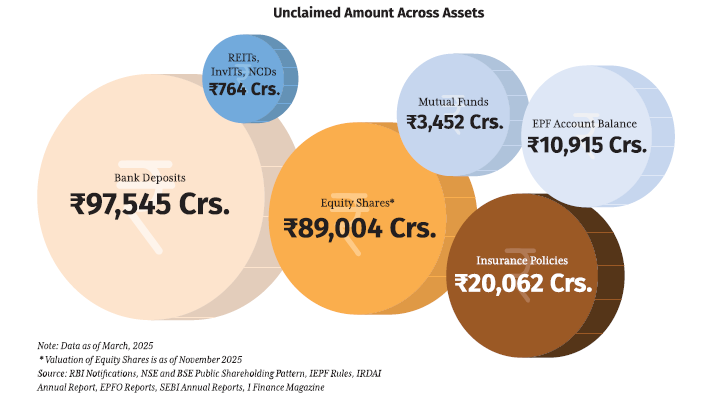

As of December 2025, approximately ₹2.2 lakh crore worth of unclaimed assets lie across government funds, bank accounts, and corporate registers in India. Households are losing decades of compounding as these assets sit idle or earn sub-optimal returns. This figure has grown sharply over the past five years, reflecting gaps in succession planning, asset documentation, and digital and financial literacy.

Here, we cover the extent, composition and accessibility of these unclaimed assets while addressing the structural inefficiencies that perpetuate this problem.

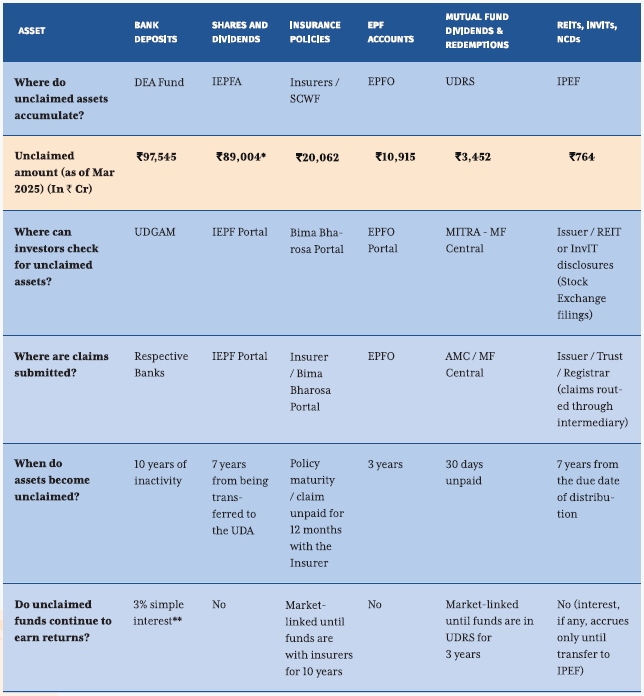

Overview of The Major Unclaimed Financial Assets in India

** 3% is only on interest-bearing deposits

Source: RBI Notifications, NSE and BSE Public Shareholding Pattern, IEPF Rules, IRDAI Annual Report, EPFO Reports, SEBI Annual Reports, 1 Finance Magazine

Glossary

The Scale of The Problem

The scale of unclaimed assets in India is best understood through the frameworks governing different financial products, as each product is subject to its own requirements, rules, and timelines.

Thus, India’s unclaimed wealth cannot be found as a consolidated number but accumulates quietly across institutions and regulators. Based on available disclosures and estimations, unclaimed financial assets run into several lakh crore rupees. In many cases, assets remain unclaimed due to outdated contact details, unreported deaths, missing nominations, or heirs being unaware of legacy investments made decades earlier.

The concentration of unclaimed assets in bank deposits reflects the era of a pre-digital financial system, where physical documentation, manual records, and limited interoperability were the norm.

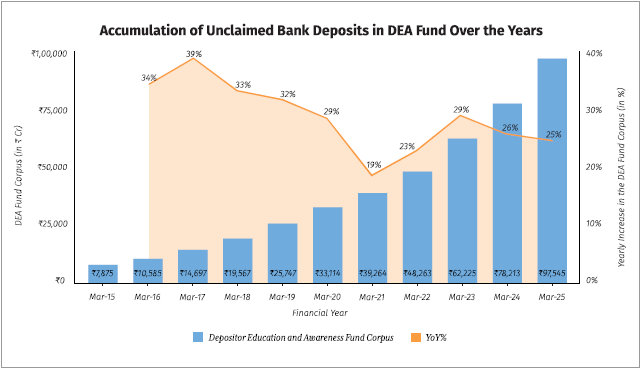

Over ₹97,000 Crore in the RBI’s DEA Fund

Under the Reserve Bank of India’s (RBI) Depositors’ Education and Awareness (DEA) Fund Scheme, banks transfer balances from savings, current, term and other accounts that remain unclaimed for ten years to the DEA Fund.

As of March 2025, the scheme held ₹97,545 crore, and over the last five years, the corpus has increased by an average of 24% annually, reflecting the steady accumulation of inactive and unclaimed balances.

Interest-bearing deposits transferred to the DEA Fund accrue simple interest at a capped rate of 3% per annum for the period they remain unclaimed in the fund. Depositors or their legal heirs can claim these balances at any time from their respective banks. The banks are required to refund the principal amount along with the accumulated interest earned during the period the deposits remained with the DEA Fund.

The applicable interest rate is well below the prevailing market rates and does not keep pace with inflation, highlighting the high opportunity cost borne by depositors. Beyond unclaimed bank deposits, equity investments form the second-largest pool of forgotten assets in India.

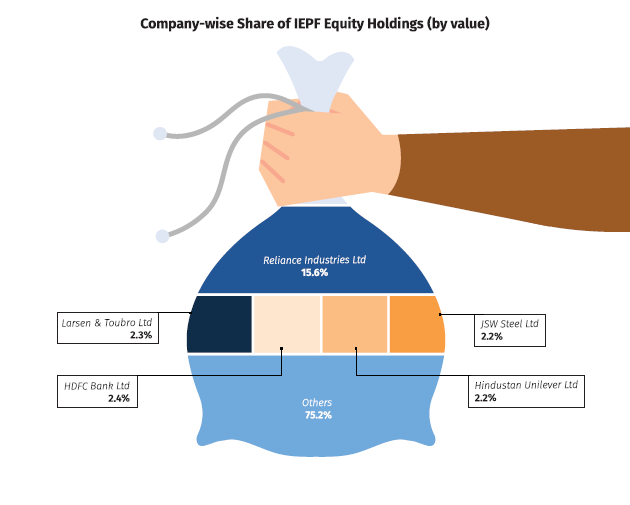

₹89,004 Crore in Unclaimed Shares in the IEPFA

While most unclaimed-asset frameworks deal primarily with cash balances, the Investor Education and Protection Fund Authority (IEPFA) is unique in that it separately houses both unpaid dividends and the underlying equity shares.

Under the Companies Act framework, share dividends that remain unpaid to the investor for 30 days after declaration are transferred to a company’s Unpaid Dividend Account, where investors have up to seven years to claim them. If dividends remain unclaimed for all seven years, the dividend and the underlying shares are mandatorily transferred to the IEPF.

As per the IEPF rules, unpaid dividends are retained as monetary balances in designated bank accounts, while unclaimed shares, whether physical or dematerialised, are transferred to IEPF’s demat accounts maintained with National Securities Depository Limited (NSDL). Unlike dividends, these shares continue to remain market-linked while in the IEPF.

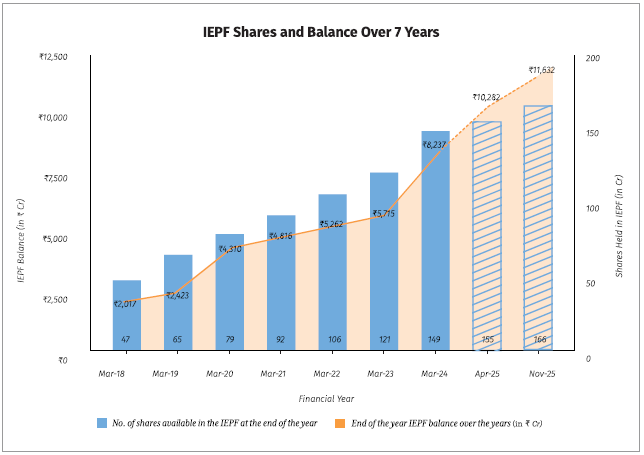

As of November 2025, the IEPFA held 166 crore shares across 1,671 listed companies, with an estimated market value of ₹89,004 crore, based on prevailing share prices.

On the other hand, the cash balance held under the IEPF was ₹8,237 crore as of March 2024, including unpaid dividends, matured deposits, and other amounts transferred under the IEPF rules.

The number of shares held under IEPF has grown by 17% annually since 2018, while the value of assets has increased by 26% annually.

Source: IEPF Annual Reports, 1 Finance Magazine

Nearly 25% of the total equity value in the IEPF is concentrated in just five widely held Indian stocks, with Reliance Industries alone accounting for 16%.

Source: 1 Finance Magazine, Listed Company Shareholding Patterns

IEPF unclaimed asset transfers are more the result of administrative gaps like outdated bank mandates, unreported deaths and heirs/nominees unaware of ancestral investments.

While unclaimed equity shares continue to remain market-linked even while in the IEPF, unclaimed insurance proceeds follow a different path.

Unclaimed Amounts of Policyholders Cross ₹20,000 Crore in 2024

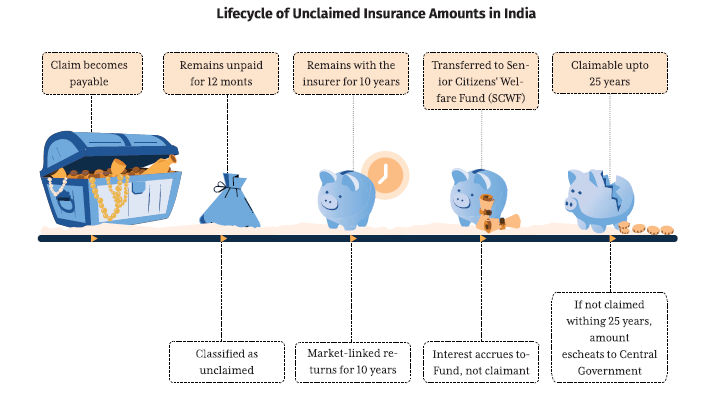

As the third largest pool of unclaimed assets in India, unclaimed insurance proceeds stood at approximately ₹20,062 crore at the end of FY2023-24, comprising policy maturities, death benefits, surrenders, and other claim payments that were not received by policyholders or nominees.

Under IRDAI’s regulatory framework, insurance proceeds are classified as unclaimed if they remain unpaid for twelve months after becoming due. During this period and for up to ten years after, the unpaid amounts remain with insurers in a segregated fund. IRDAI requires insurers to invest the unclaimed insurance proceeds in money market instruments and fixed deposits. The investment income accrued is credited quarterly to the unclaimed amount, with a 20 basis point administrative fee per annum.

But at the end of the ten years, if the amount remains unclaimed, insurers are mandated to transfer the proceeds to the Senior Citizens’ Welfare Fund (SCWF). Even though the SCWF is an interest-bearing account in the public account of the Union of India, the interest accrues to the fund itself and is not passed back to claimants. Further, policyholders can claim their unclaimed amounts for up to 25 years, after which the amounts escheat to the Central Government as per Section 126 of the Finance Act 2015.

Beyond insurance, a large share of forgotten wealth in India also emerges from employment-linked savings.

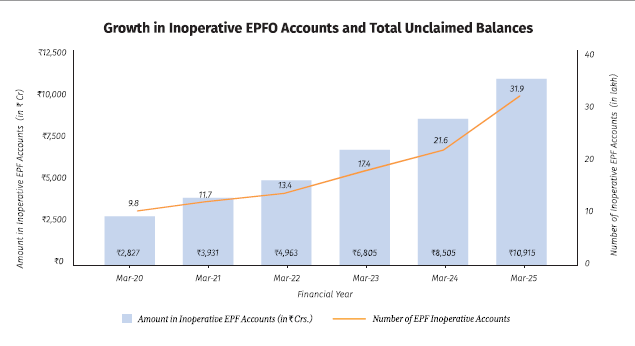

Inoperative EPF Accounts Hold Over ₹10,000 Crore in Balance

The Employee Provident Fund (EPF) functions as a default retirement savings instrument for most salaried employees. Because contributions are automatic and require little active engagement, EPF balances are often left unmanaged, making them forgettable. Before the rollout of the Universal Account Number (UAN) framework, employment-linked savings were spread across multiple employers and accounts and weren’t monitored or recorded.

Under the framework, an account is classified as inoperative if it remains inactive for a period of three years, with no contributions or withdrawals. The accounts continue to exist on the records of the Employees’ Provident Fund Organisation (EPFO) and can be claimed by account holders at any time.

Despite the introduction of the UAN in 2014, both the number of inoperative EPF accounts and the balances held in them have risen over time. Inoperative balances grew from ₹2,827 crore in 2020 to ₹10,915 crore in 2025, reflecting a y-o-y growth of 31%. Inoperative accounts grew to 31.9 lakh in March 2025 from 9.8 lakh in March 2020.

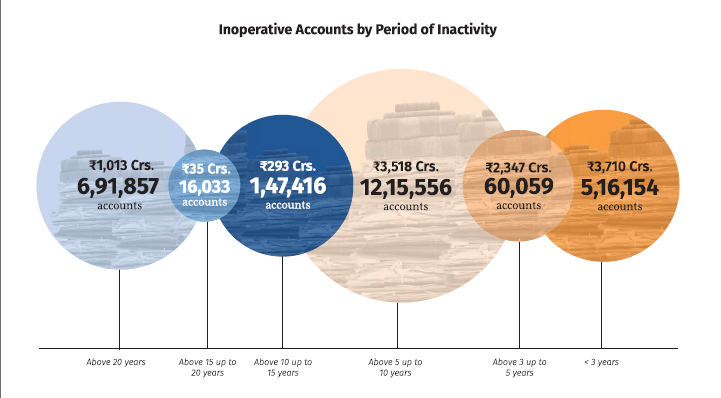

A closer look at the distribution of the accounts tells us that nearly 50% of the total unclaimed corpus lies in only 0.4% of the EPF inoperative accounts, with balances exceeding ₹10 lakh.

Further, over 12 lakh, or 38%, of the total inoperative accounts have been dormant for five to ten years, collectively holding ₹3,518 crore or 32% of the entire EPFO unclaimed corpus. And close to 7 lakh accounts have been inoperative for over twenty years, which is pretty much half of your employment years.

Inoperative Accounts by Period of Inactivity

Inoperative accounts are heavily concentrated in metropolitan cities such as Bangalore, Delhi, Kolkata, and Chennai, reinforcing the role of job mobility and inter-city migration in driving dormancy. However, unclaimed assets are not just limited to passive savings instruments and extend to digitally managed assets as well.

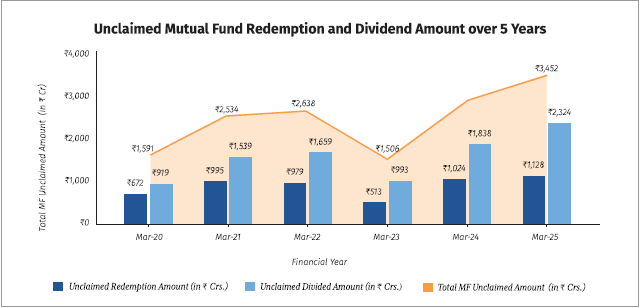

Unclaimed Mutual Fund Amounts Exceed ₹3,000 Crore

Mutual funds are among the most digitally integrated and centrally regulated investment products in India. Yet, a significant pool of investor wealth remains unclaimed. In FY 2024-25, mutual funds collectively held ₹3,452 crore in unclaimed dividends and redemption proceeds, a ~21% year-on-year increase from ₹2,862 crore in FY 2023-24.

Unlike equity shares, mutual fund units themselves aren’t declared inactive, and ownership of the underlying asset remains with the investor. Amounts are declared unclaimed when dividend payouts or redemption proceeds are not received by investors.

Under the regulatory framework of the Securities and Exchange Board of India (SEBI) and the Association of Mutual Funds in India (AMFI), such unpaid amounts after thirty days are parked under the Unclaimed Dividend and Redemption Scheme (UDRS). These amounts are invested in liquid instruments, allowing them to continue appreciating in value for up to three years from the date of creation of the URDS units.

However, if the unitholder does not claim the amount within three years, then the appreciation accrued from the fourth year onwards is transferred to the IEPF. Both the principal and the appreciation accrued during the first three years are fully claimable by legal claimants.

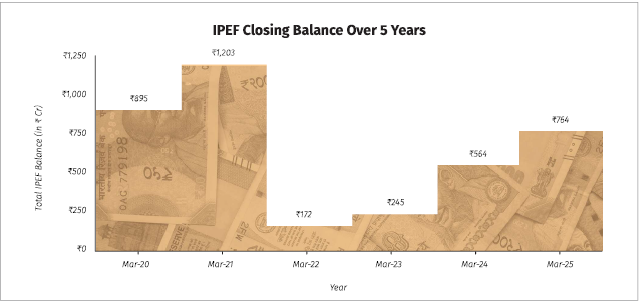

Unclaimed Cash Flows from New-Age Market Products

The Real Estate Investment Trusts (REITs), Infrastructure Investment Trusts (InvITs), and listed Non-Convertible Debentures (NCDs) are among the fastest-growing market-linked instruments that give regular cash distributions to investors. As these payouts have scaled up, so have their unclaimed interest, dividends, and redemption proceeds.

Until recently, these instruments sat in a regulatory grey zone and lacked a framework for handling unpaid distributions. Under the current rules, any distribution that remains unpaid for fifteen days is first transferred to an escrow or Unpaid Distribution Account, and if the amount continues to remain unclaimed for seven years from the due date, it is transferred to the SEBI-administered Investor Protection and Education Fund (IPEF). These amounts do not lapse to the government and remain claimable by investors or their legal heirs without any time limitations.

As of March 2025, the balance of the IPEF, where the unclaimed amounts of REITs, InvITs, and NCDs go into, is ₹764 crore. The absolute value of unclaimed amounts in this segment is still small relative to bank deposits or equity shares, but the pace is rising steadily at 31.4%. This tells us that even digitalised investing instruments are beginning to contribute to India’s forgotten financial wealth.

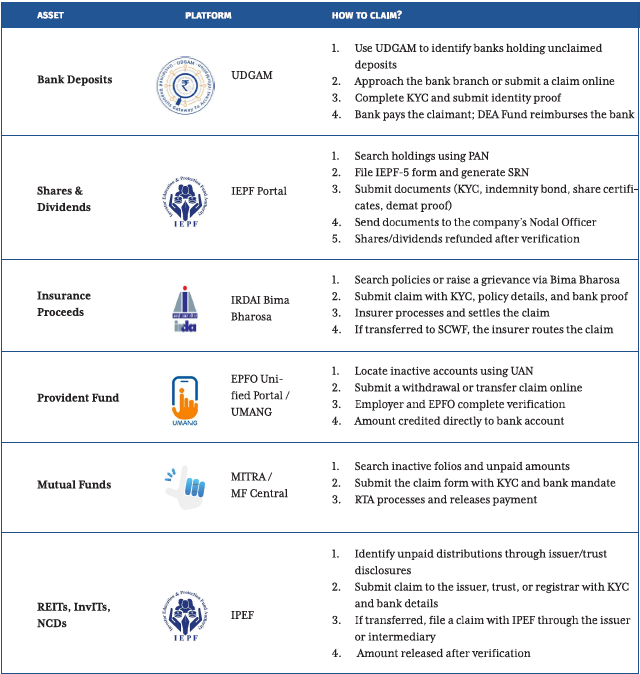

How to Recover These Forgotten Assets?

As the stock of unclaimed financial assets in India has grown, regulators and the government have, over the years, launched multiple centralised digital platforms that allow investors and their heirs to identify, locate, verify, and recover their respective dormant assets across institutions.

A recent initiative undertaken by the Ministry of Finance is the “Your Money, Your Right” campaign, launched in October 2025, which set up facilitation camps to help claimants recover unclaimed financial assets. In the two months of its launch, the initiative helped settle approximately ₹2,000 crore in unclaimed funds.

In all its diversity, the recovery process of unclaimed financial assets follows a common underlying logic. The recovery of money is more about verifying the identity and ownership of the asset.

What the Claim Process Typically Involves

Across asset classes, the claim process usually requires the same core set of documents:

- Identity & KYC

- PAN

- Aadhar / Passport / Voter ID

- Date of birth proof

- Proof of address

- Up-to-date phone and email

- Entitlement & Succession

- Account / folio / policy / UAN / demat documents

- Policy bond / original share certificates / CAS / UAN history

- Death certificate of the original holder

- Nominee details

- Legal heir certificate / succession certificate / probate (if no nominee)

- Bank documentation

- Active bank account details

- Cancelled cheque / bank statement

- Indemnities & Declarations

- Indemnity bond

- No-objection certificates from co-heirs

- Affidavit / notarised declaration / apostilles

Investors can keep a physical and digital kit ready with the above items.

As mentioned earlier, there are a few official digital platforms established for investors to check for and claim their dormant accounts or funds:

Where to Search For and How to Claim (by Asset Class)

Where Do Unclaimed Assets Go and How Are They Utilised?

Unclaimed assets do not sit idle in these institutions. Each asset category, governed by a defined framework, used these funds to help protect and educate the citizens of India. Let’s understand what happens to these unclaimed assets over time.

- Bank Deposits under the DEA Fund

Unclaimed bank deposits transferred to the RBI’s DEA Fund remain claimable indefinitely by depositors or their legal heirs or nominees. These funds are deployed for depositor education, awareness campaigns and financial literacy initiatives; claim settlements take priority. When the depositor makes a claim, banks first refund the claimant and are subsequently reimbursed by the RBI from the DEA Fund corpus.

- IEPF’s Shares & Dividends

Under Section 125 of the Companies Act, unclaimed dividends and the underlying shares transferred to the IEPF are held in perpetuity. The IEPF corpus is utilised for investor education, awareness, refunds to claimants, and research, while ownership of shares remains intact.

When a valid claim is made, shares are returned to the claimant in their demat account, along with the unpaid dividends originally transferred. However, any corporate benefits or income accrued during the period do not pass through to the claimant.

- Insurance Proceeds and the SCWF

Unclaimed insurance policy proceeds, unlike other asset funds, do not appreciate or earn returns on the unclaimed amount while with the insurers.

While claim rights continue even after transfer to the SCWF, returns do not accrue to claimants. Any interest earned during this period is retained by the fund. Policyholders or their heirs generally have up to 25 years to claim these amounts, after which they may escheat to the Central Government under the Finance Act, 2015. The SCWF uses these amounts for the welfare of senior citizens.

- UMANG’s Inoperative EPF Accounts

Inoperative EPF accounts continue to exist indefinitely within the EPFO system and do not migrate to any external fund such as the DEA Fund, IEPF, or SCWF. In the event of the account holder’s death, legal heirs or nominees typically have up to 25 years to initiate a claim, beyond which balances may escheat to the Central Government. In practice, most EPF balances remain reclaimable for extended periods, provided documentation is in order.

- Mutual Funds Under UDRS

Unclaimed dividends and redemptions are parked in the UDRS. During the first three years, both the principal and the appreciation remain fully claimable by claimants. From the fourth year onwards, the appreciation accrued on the principal is transferred to the IEPF. This structure preserves capital but places a time limit on market-linked profits. Also, there is no time limit for claiming the principal amount and the appreciation accrued for the first three years.

- REITs, InvITs and Listed Debt Instruments

After being transferred to the IPEF, the funds are then used for investor education and awareness initiatives, while claim rights continue to remain intact. There is no expiry period for investors or their legal heirs to reclaim these amounts.

Thus, across assets, the claim rights are preserved, but the value of your asset is not guaranteed. Over time, capped interest rates, forgone market returns, or diversion of income streams shift the financial benefit away from the investors.

Is Forgotten Wealth a Planning Failure?

Across assets, a consistent pattern emerges. India’s growing stock of unclaimed wealth is a result of poor financial hygiene.

Frameworks like the DEA Fund, IEPF, EPFO and SCWF are designed to preserve money value. Yet, the capital parked in these funds loses time and years of compounding, liquidity and timely use. In many cases, ownership of assets remains intact, but access goes away due to outdated records, incomplete nominations, and most critically, the absence of clear succession planning.

This pattern extends beyond financial products. Physical assets, particularly real estate, represent an even larger and denser pool of unclaimed wealth. Effective succession planning is not a one-time exercise but an ongoing process of documentation, consolidation, nomination and communication. This is where the role of a fee-based, qualified financial advisor comes into the picture.

Table of Contents

Share:

Share: