Popular searches

Get to know your policy better

Product scoring may vary based on gender, age, policy tenure and sum assured.

Gender

Age Group

The lowest age in the selected range is considered for price evaluation (e.g., 25 - 29)

The lowest age in the selected range is considered for price evaluation (e.g., 25 - 29)

Sum Assured

What New vs Old Home Prices Reveal About Maharashtra’s Housing Market

When new homes start selling at a clear, rising premium to resales of older ones, the real estate market is telling you something. It is about what buyers now value in layout, lifestyle and location. In Maharashtra’s three big housing markets—Greater Mumbai, Pune and Thane—that premium has quietly widened over the past decade. Buyers are paying up for newer layouts, managed townships and infra‑linked locations, while older stock loses pricing power even in prime pin codes.

When the gap turns negative, the message is different. A negative spread—where resales are more expensive than new launches in the same micro‑market—usually signals that older stock sits in more established neighbourhoods, closer to job hubs or social infrastructure, while new supply is still coming up in fringe locations or in projects where liveability has not yet caught up. Over time, if infrastructure and amenities improve around these new corridors, that negative gap often narrows and can flip positive, as seen in several Pune and Thane sub‑markets between 2016 and 2025.

Why The New‑Vs‑Old Gap Is A Powerful Signal

In housing analysis, the spread between primary (new launch) prices and secondary (resale) prices tells you three things:

- How fast old stock is becoming obsolete,

- How much buyers value amenities over address, and

- Where infrastructure is quietly redrawing the map.

When primary and secondary prices sit close together, location is doing most of the work. When the primary premium widens and stays wide, product and connectivity are taking over.

Maharashtra’s residential sales data between 2016 and 2025 shows this shift clearly. In all three major markets, new homes that are better designed and better connected have pulled ahead of resale stock, often by double‑digit percentages, even when both sets of homes sit in the same micro‑market.

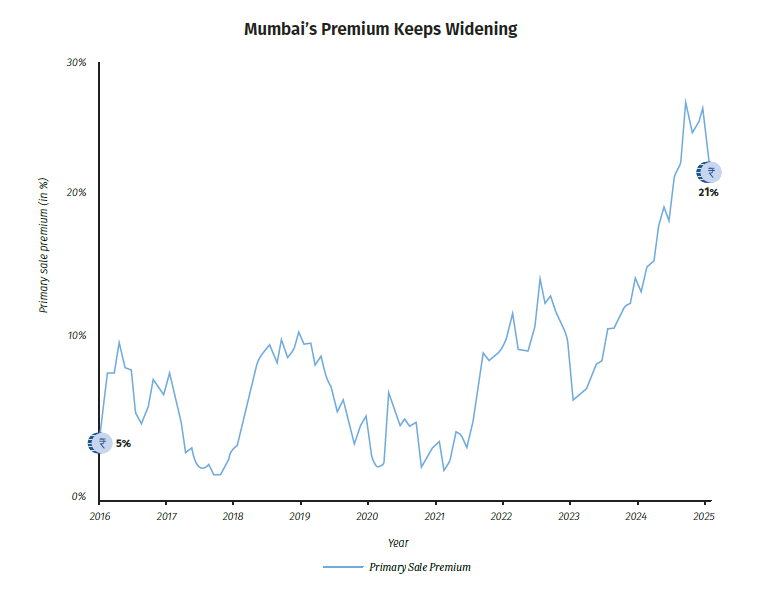

Mumbai Shows Consistent Positive New Home Premium

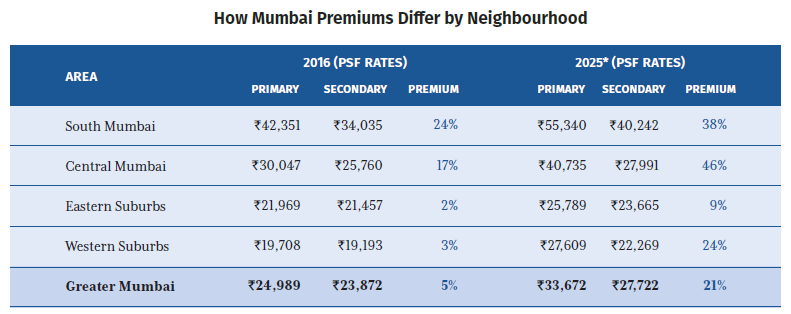

Greater Mumbai remains India’s most expensive housing market, with an average primary price of roughly ₹33,700 per sq. ft (PSF) as of September 2025. Behind that headline sits a decisive internal shift: the citywide premium for primary over secondary stock has widened from about 5% in 2016 to over 21% in 2025.

Drill down by area, and the pattern is sharper. In almost every sub‑market, new launches have broken away from older buildings that share the same basic location but lack contemporary layouts, parking and amenities.

- In South Mumbai, the primary premium has risen from 24% to 38% as buyers shift from ageing standalone buildings to high‑rise towers that finally bundle parking, security, amenities and better services into a single address.

- In Central Mumbai, the spread has exploded—from 17% to 46%—driven by large integrated projects and redevelopment along key corridors where older buildings cannot match new‑build specifications.

- Even the Eastern and Western suburbs, which once traded almost at par across new and old stock, now show clear positive premiums as modern townships and infra‑linked clusters reset benchmarks.

With the average inventory age now above four years, buyers are effectively using the primary market as the new anchor for what each micro‑market is “really” worth. Resale homes still clear, but at visibly lower PSF levels unless they are part of recently built projects.

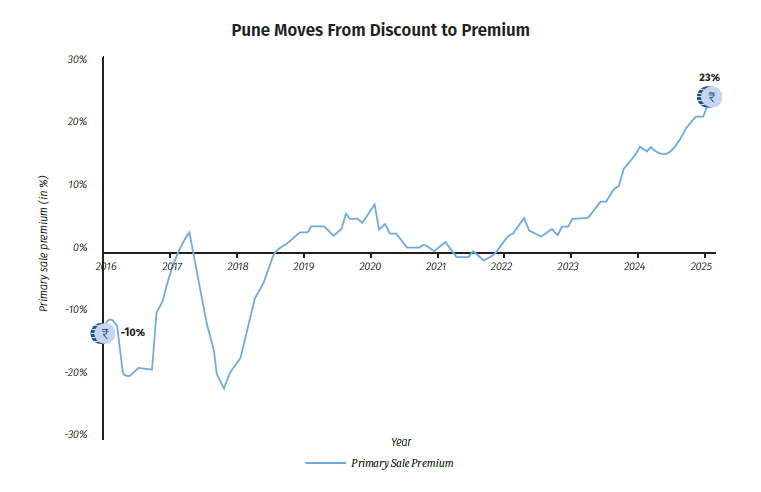

Pune New Home Premium Is At Its Highest

Pune’s transformation is even more striking because it starts from the opposite base. In 2016, several key sub‑markets actually priced resales above new launches; older projects with established neighbourhoods commanded a comfort premium. By 2025, that equation had flipped almost everywhere.

Across the city, 48% of inventory is less than five years old, unsold stock is around 2.69 lakh units, and 62,677 newly launched units were sold in 2025 alone—Pune’s strongest post‑COVID year. This new stock is not just more plentiful; it is also where buyers are willing to pay a clear PSF premium.

The message is consistent:

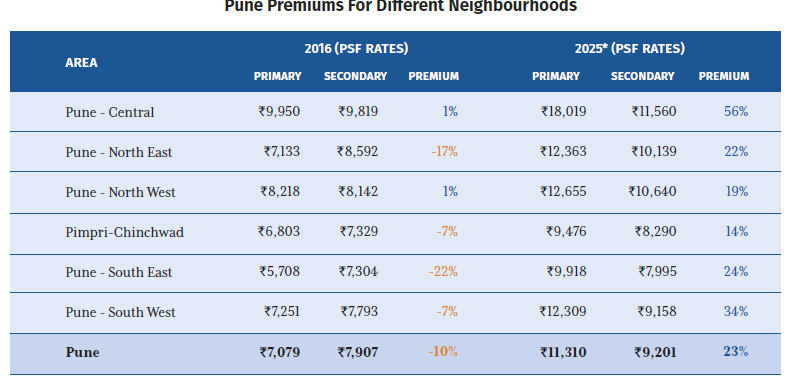

- Sub‑markets such as South‑East and South‑West, where older inventory once enjoyed a 20%+ advantage, now show a 24–34% premium for new launches.

- North‑East and Pimpri‑Chinchwad, tied closely to IT/industrial job hubs, have migrated from resale‑friendly pricing to clear primary premiums as integrated townships and better social infra come up.

- Citywide, the average primary premium has moved from a -10% discount to a +23% premium, underlining how quickly buyer preferences have moved towards planned communities and managed developments.

In practice, this means that for many working households, “Pune property” increasingly implies a unit in Hinjewadi, Wakad, Wagholi or similar growth corridors rather than a legacy building in the inner city.

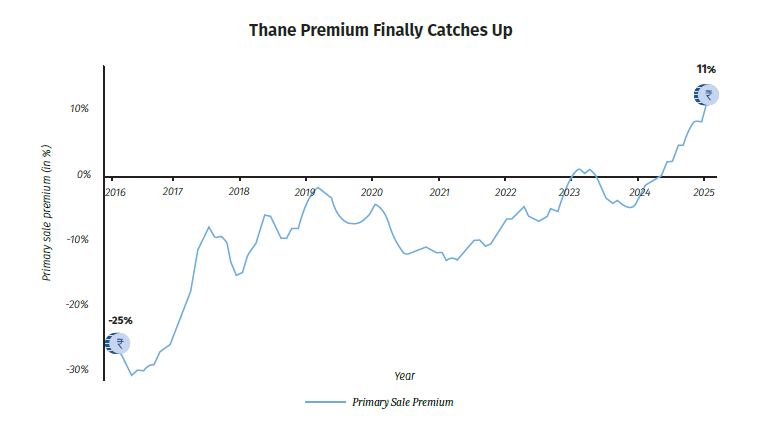

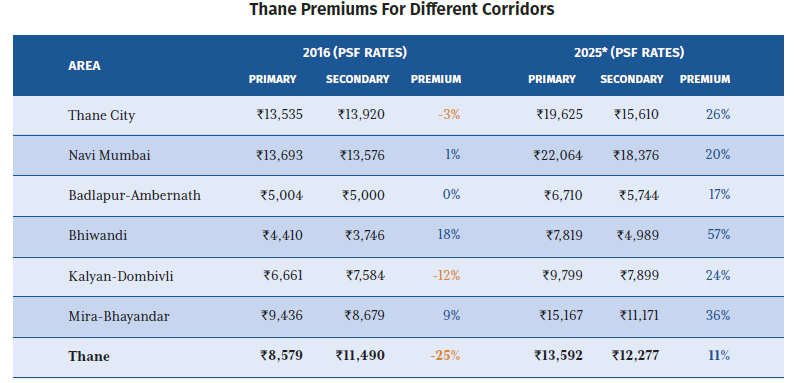

Thane New Launches Are Finally Ahead of Resales

Thane illustrates how infrastructure can steadily flip a market from resale‑dominated to new‑launch‑led. Historically, the strongest pricing power sat with older, centrally located buildings. As ring roads, the forthcoming Metro Line 4 corridor and larger integrated townships have expanded the city’s footprint, that balance has shifted.

By 2025, prices in infra‑adjacent townships along Ghodbunder Road and other corridors have caught up with, and often overtaken, resale stock—even in markets that once gave older buildings a clear edge. Nearly 82% of sales in Q3 2025 came from 1/1.5 and 2/2.5 BHK units, reflecting end‑users upgrading from rented accommodation in Greater Mumbai to ownership in Thane.

Key inferences:

- Thane City has transitioned from a small resale premium to a 26% new‑launch premium as township living and better connectivity pull buyers outward from the historic core.

- In Bhiwandi, the primary premium has surged from 18% to 57%, reflecting how logistics‑linked growth and new project launches have re‑rated a once-peripheral market.

- Region‑wide, Thane has moved from a -25% discount for new launches in 2016 to an 11% premium in 2025, a dramatic re‑pricing in less than a decade.

How Maharashtra’s Housing Cycle Is Changing

Taken together, the Maharashtra data points to a clear conclusion: housing cycles are no longer moving in broad, city‑wide waves. They are fragmenting by micro‑market and by quality of stock.

- In Greater Mumbai, the primary premium shows that buyers now treat modern towers and redeveloped projects as the reference price, even inside long‑established pin codes.

- In Pune, the flip from a –10% discount to a +23% average premium for new launches tells you that growth‑corridor townships and younger stock are where both demand and pricing power now reside.

- In Thane, infra‑adjacent pockets along key corridors have pulled the whole region from resale‑led to primary‑led pricing in less than a decade.

For investors and professionals reading these markets, the implication is straightforward: returns will increasingly depend on picking the right pocket within the city and the right side of the primary‑secondary divide, not simply owning exposure to the “right” metro.

Table of Contents

Share:

Share: