“How can I save for retirement” ranks among the most searched personal finance queries in India this year. For most people, the answer stops at one word, EPF. Provident fund contributions feel like retirement planning taken care of, deducted automatically from every payslip without a single decision required.

Built around that one scheme alone, retirement planning stops short of everything else the government offers. Corpus-building tools, guaranteed pensions, and post-retirement income schemes sit unexplored for most working Indians.

Picture a retiree who planned to retire at 60 and live until 85. His expenses grow at 6 to 7% a year, in line with recent inflation. Run his current corpus against that math and it runs dry at 71, fourteen years before he actually needs it to last.

1 Finance’s Retirement Readiness Survey uses this exact projection to show why the question needs more than a one-word answer. The shortfall itself comes first, followed by six government schemes built to close it, each solving a different piece of the problem.

1 Finance measured the retirement shortfall among Indians

The median respondent in the survey saves 15% of their annual income toward retirement and starts at age 39, leaving roughly two decades to build a corpus before a typical retirement at 60. Currently, the corpus stands at ₹28 lakh against a target of ₹1 crore, a shortfall the survey calls the corpus gap, running at 3.6x of what’s already saved.

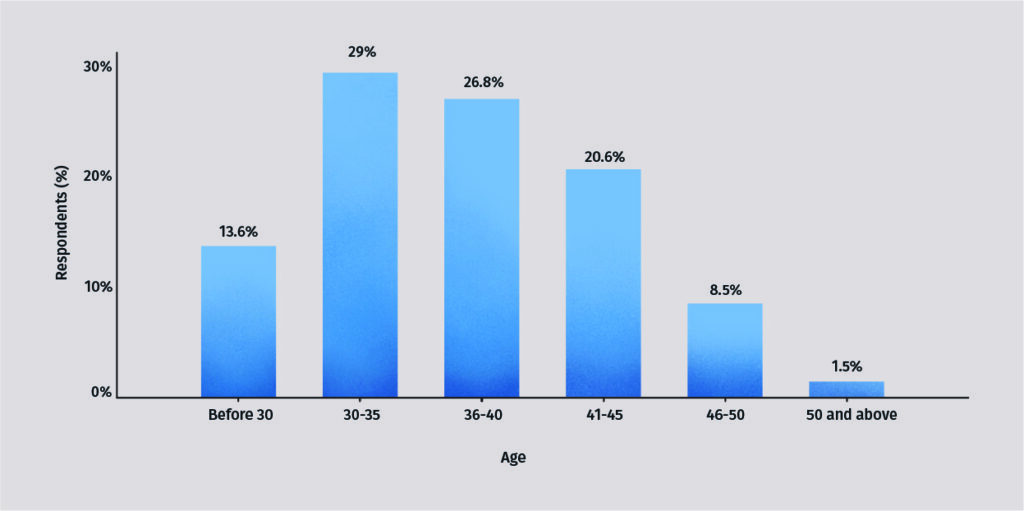

Only 13.6% of respondents started saving before 30, while 29% waited until their early thirties and a combined 30.6% didn’t begin until after 40.

Chart I: When respondents started saving for retirement

This delay has a real cost, since compounding rewards time far more than it rewards a larger contribution. Someone starting at 39 has 21 years left to reach ₹1 crore. Someone starting at 28 has 32 years for the same goal, and needs a noticeably smaller monthly contribution to get there. Nearly half the respondents, 46.5%, save between just 10 and 19% of their income, comfortably inside the range that feels responsible without actually closing a shortfall of this size.

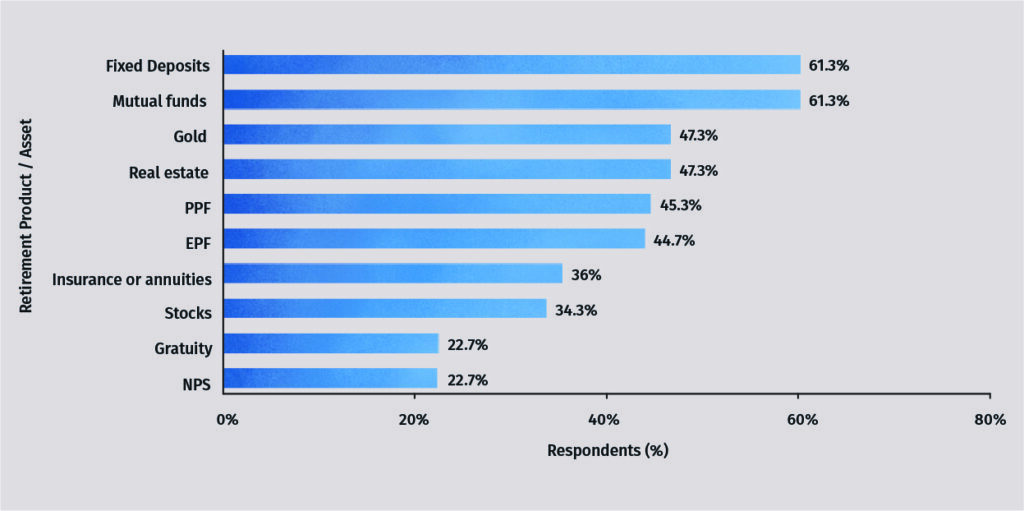

Indians are building retirement corpuses from assets built for other goals

Fixed deposits and mutual funds top the survey’s asset allocation chart, each held by 61.3% of respondents building a retirement corpus. Gold and real estate follow closely at 47.3% each, ahead of the Public Provident Fund at 45.3% and the Employees’ Provident Fund at 44.7%. National Pension Scheme, the one product built specifically for the retirement planning goal, sits near the bottom at 22.7%, level with gratuity, and behind stocks at 34.3% and insurance or annuities at 36%.

Chart II: What retirement portfolios look like

An FD opened for any goal or a mutual fund SIP started without a retirement label outranks NPS and PPF, the two products the government designed around this exact outcome. NPS and PPF solve retirement’s particular tax and payout problems, yet they sit behind assets that solve no problem specific to retirement at all.

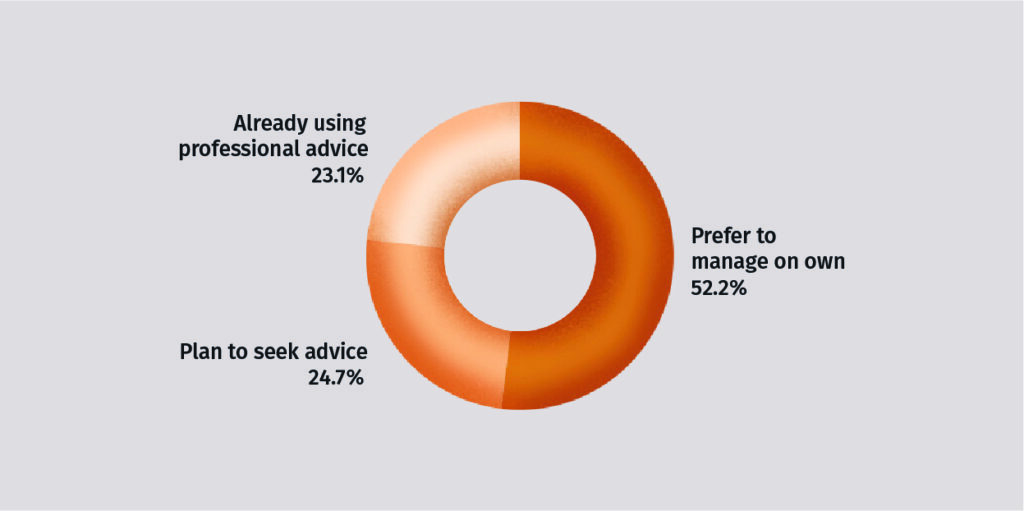

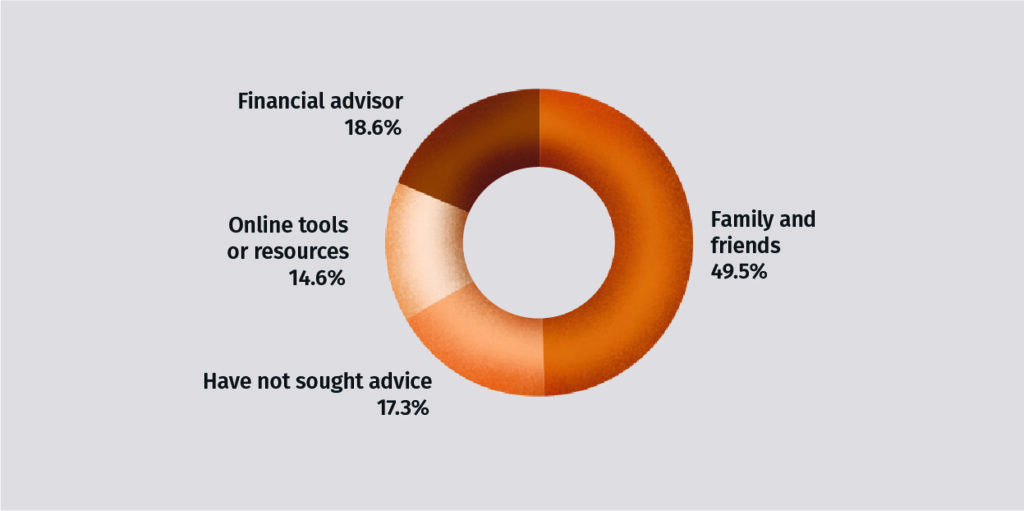

Most Indians are planning retirement without professional help

More than half the respondents, 52.2%, plan to manage their own retirement planning without outside help. Only 23.1% currently use professional financial advice, and 24.7% intend to seek it eventually.

Chart III: Respondents approach retirement planning

Among those who do ask someone, family and friends remain the dominant source at 49.5%, ahead of financial advisors at 18.6% and online tools at 14.6%.

Where respondents go for retirement planning

A shortfall of 3.6x is unlikely to close through general advice from family or online tools alone. It needs scheme-by-scheme decisions on tax treatment, lock-in periods, and payout structure, the kind the sections below walk through in detail, and worth reading with your own numbers in hand rather than a friend’s.

Employee Provident Fund (EPF)

Every salaried employee already contributes to Employee Provident Fund (EPF) without filling an extra form. The EPF Scheme 2026 draws 12% from your basic pay and dearness allowance, matched by an equal 12% from your employer, currently earning 8.25% for FY 2025-26.

Of your employer’s share, about ₹1,250 is diverted into EPS under the EPS 2026 rules, which continue to guarantee a minimum pension of ₹1,000 a month for life after at least ten years of eligible service, while the new EPF Scheme 2026 caps the mandatory EPF contribution at ₹1,800 a month based on the statutory wage ceiling of ₹15,000.

The deduction happens before the salary reaches you, with no decision required on your part. That default mechanism explains why EPF already sits in 44.7% (Chart II) of retirement portfolios in the survey, ahead of PPF and NPS, without most contributors ever choosing it deliberately.

The new EPF Scheme 2026 kept this contribution structure and the 8.25% rate unchanged when it replaced the 1952 scheme on June 29th, 2026. Hence, the corpus already built in your account continues exactly as before. A separate breakdown covers the full monthly interest calculation and what changed under the new scheme, but EPF forms the base layer under whatever else you build, a layer the survey suggests most contributors never add to.

National Pension Scheme (NPS)

National Pension Scheme (NPS) opens a retirement account to any Indian citizen between 18 and 70, with market-linked returns and a tax deduction ceiling of ₹2 lakh, ₹1.5 lakh under Section 80C plus an exclusive ₹50,000 under Section 80CCD(1B). Only 22.7% of the survey’s respondents hold NPS, despite it being the one financial product engineered for this exact outcome.

NPS withdrawal rules changed materially in December 2025. Non-government subscribers can now withdraw up to 80% of the corpus as a lump sum, with a minimum of 20% going into an annuity, down from the earlier 60-40 split. Tax law hasn’t caught up with the new withdrawal limit. Section 10(12A) still exempts only 60% of the corpus from tax. Any lump sum taken above that threshold gets taxed at your regular income slab rate unless a future budget extends the exemption.

Most people compare NPS against equity mutual funds using pre-tax returns, where equity wins easily. Retirement is fundamentally an income goal, not a pure accumulation one. NPS’s post-tax, annuitised corpus routinely ends up ahead of an equity portfolio’s after-tax withdrawal, since a self-managed withdrawal plan delivers less consistency than a structured annuity.

At exit, NPS also offers the Retirement Income Scheme (RIS), which pairs the mandatory annuity with a scheduled withdrawal of the remaining corpus. A separate breakdown covers the full mechanics of this drawdown structure, including the mandatory annuity calculation and the SPR and SUR options.

Also read: What’s new in NPS: How retirement income scheme (RIS) changes NPS withdrawal rules

Public Provident Fund (PPF)

Public Provident Fund (PPF) pays 7.1% for the July-September 2026 quarter, with every rupee of interest and the full maturity amount sitting outside your tax return under the EEE structure. The account locks in for 15 years, extendable in blocks of five, with contributions up to ₹1.5 lakh a year eligible for tax deductions under Section 80C.

PPF’s 7.1% rate trails EPF, yet its EEE structure means that entire return reaches you without a single rupee lost to tax; a protection neither EPF’s taxable-above-threshold interest nor an equity fund’s capital gains tax can match.

The survey shows PPF sitting marginally ahead of EPF, 45.3% against 44.7% (Chart II), despite EPF being automatic for salaried employees while PPF needs a deliberate account opened and funded every year. A meaningful share of Indians are choosing a tax-free structure on purpose, even when an automatic option already sits inside their salary.

Unified Pension Scheme (UPS)

Unified Pension Scheme (UPS) launched on April 1st, 2025 as an alternative to NPS for central government employees, guaranteeing 50% of average basic pay over the last 12 months as pension after 25 years of service, with a minimum guaranteed pension of ₹10,000 a month after just 10 years of service.

For the narrow group it covers, a pension fixed at 50% of average basic pay encourages guaranteeing the number instead of leaving it to be projected.

Government retirement schemes: A quick snapshot

| Scheme | Best suited for | Current rate or benefit | Lock-in |

|---|---|---|---|

| EPF | Salaried employees | 8.25% plus guaranteed pension | Till retirement |

| NPS | Anyone wanting a higher tax deduction | Market-linked, up to ₹2 lakh deduction | Till age 60 |

| PPF | Self-employed, freelancers | 7.1%, entirely tax-free | 15 years, extendable |

| UPS | Central government employees | 50% of average basic pay | Till retirement |

Conclusion

Six schemes, each solving a different piece of the retirement problem, don’t automatically add up to a plan. EPF’s automatic deduction convinces most salaried employees the job is already done, yet the survey’s median respondent is still ₹72 lakh short of their own stated target. Which of these six schemes carries the most weight depends on facts specific to the saver, whether income comes through a formal payslip or not, how many working years remain before 60, and whether the existing corpus already sits in tax-free assets or taxable ones.

A SEBI-registered, commission-free Qualified Financial Adviser can map these six schemes against that exact combination of income, employment status, and time horizon, giving you a personalised financial plan for your retirement.